Market Data

July 7, 2022

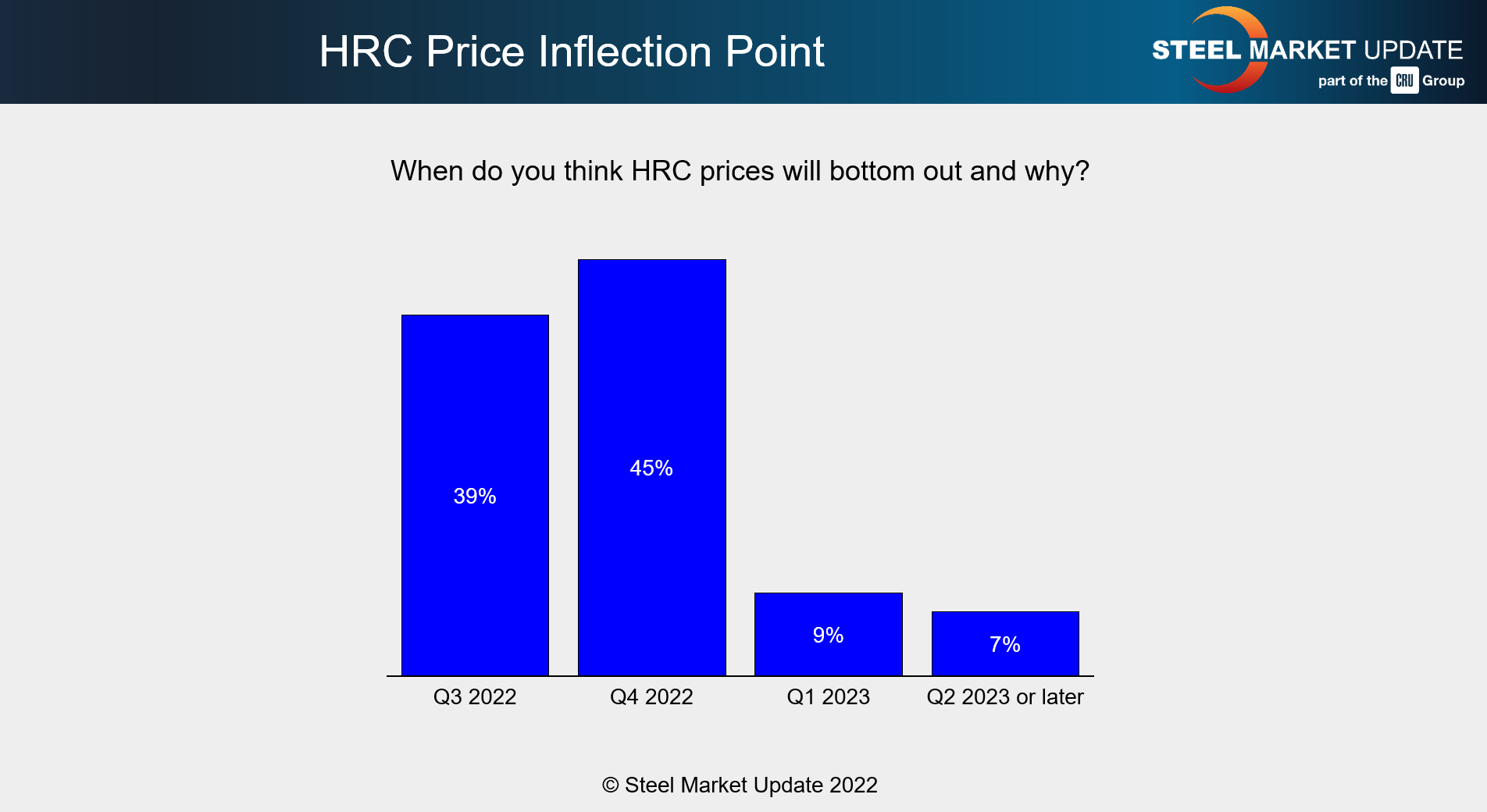

SMU Survey: More Respondents Expect HRC Pricing Bottom in Q4

Written by Laura Miller

More respondents to SMU’s latest survey now think hot-rolled coil prices will bottom in the fourth quarter of this year, with a majority anticipating prices to fall into the range of $800-899 per ton ($40-44.95 per cwt) by early September.

As of last week, SMU’s average HRC price was $995 per ton.

Just a month ago, when HRC prices averaged $1,255 per ton, more than half of survey respondents predicted prices would bottom in the third quarter.

Here is where things stand now:

Just under half of survey respondents (45%) now think HRC prices will find a floor in Q4, while 38.75% predict one will be found in the current quarter.

Here is what survey respondents had to say about their predictions of when and why a bottom might be reached on HRC prices:

“Historical pattern: mills will find a way to stop the bleeding. I don’t subscribe to an apocalyptic future.”

“Buyers are pushing prices so fast, we will get to a bottom quickly and the outages and labor negotiations will help establish a floor.”

“Lack of demand and new capacity at full swing.”

“Buyers are ensuring they will be in business next year and reducing inventories.”

“Falling demand, but mills likely have some discipline to slow the fall in prices.”

“Demand erosion will occur faster than mills idling capacity.”

“Backlogs will ease the decline until Q4.”

“At some point, folks will have to start buying again.”

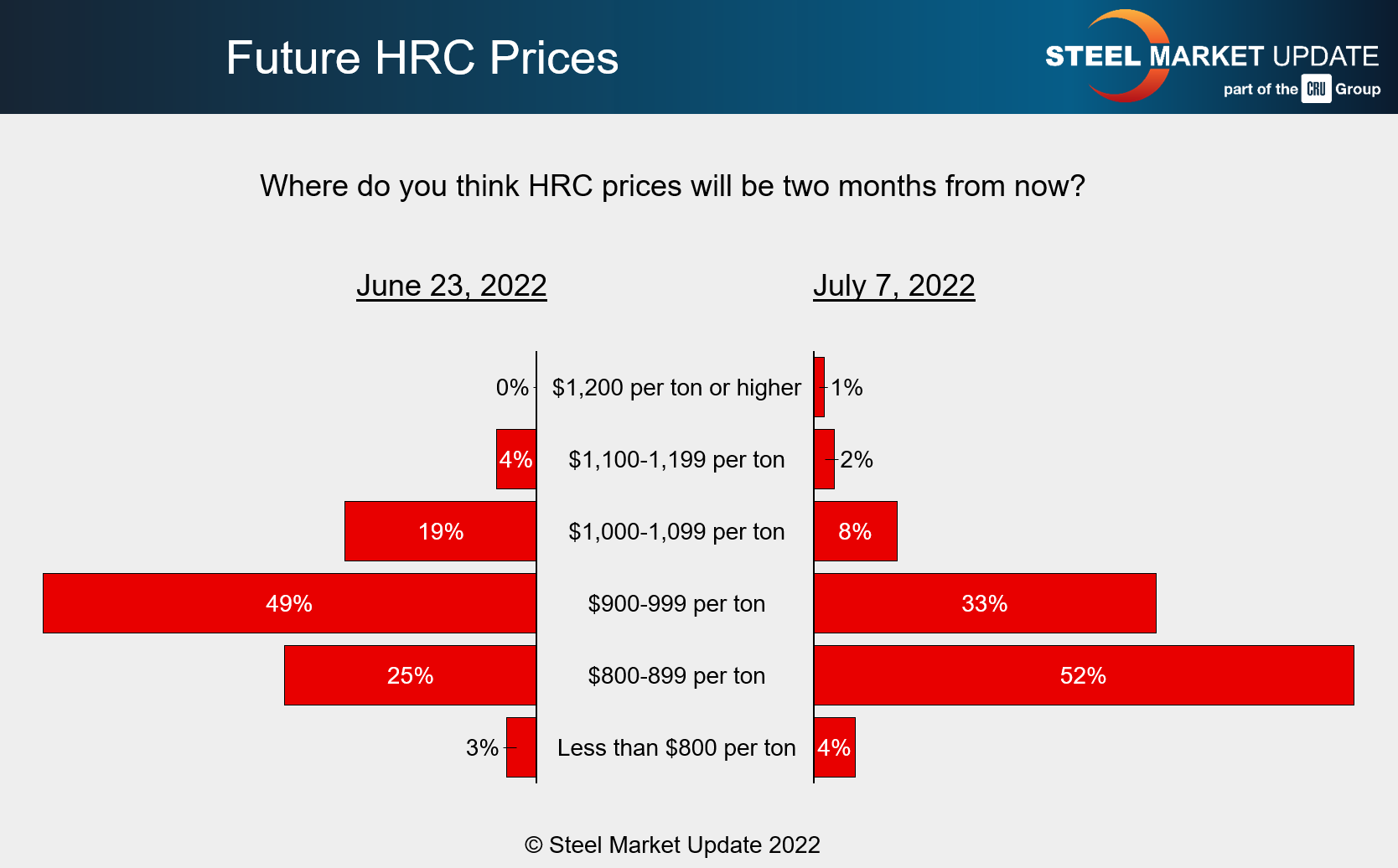

As for pricing expectations, here is where things currently stand:

This week’s SMU’s survey asked, with HRC averaging $995/ton last week, where do you think HRC prices will be two months from now?

More than half of respondents (52%) feel prices will be $800-899/ton – a big increase from the 25% predicting that range two weeks ago. A third of respondents believe prices will be $900-999/ton in September. Only 4% predict prices will be below $800/ton.

“It’s up to the mills to regulate supply,” one respondent noted.

“Chinese HRC is down 11% in the past 30 days, and the same doom and gloom message is over there,” said another.

Another respondent predicted prices will “bottom out in the $800s, but two months from now, we’ll have come back a smidge and be in the early $900s.”

By Laura Miller, Laura@SteelMarketUpdtae.com