Plate

July 8, 2022

Hot Rolled vs Plate Steel Prices: Plate Premium Rises to Record High

Written by Brett Linton

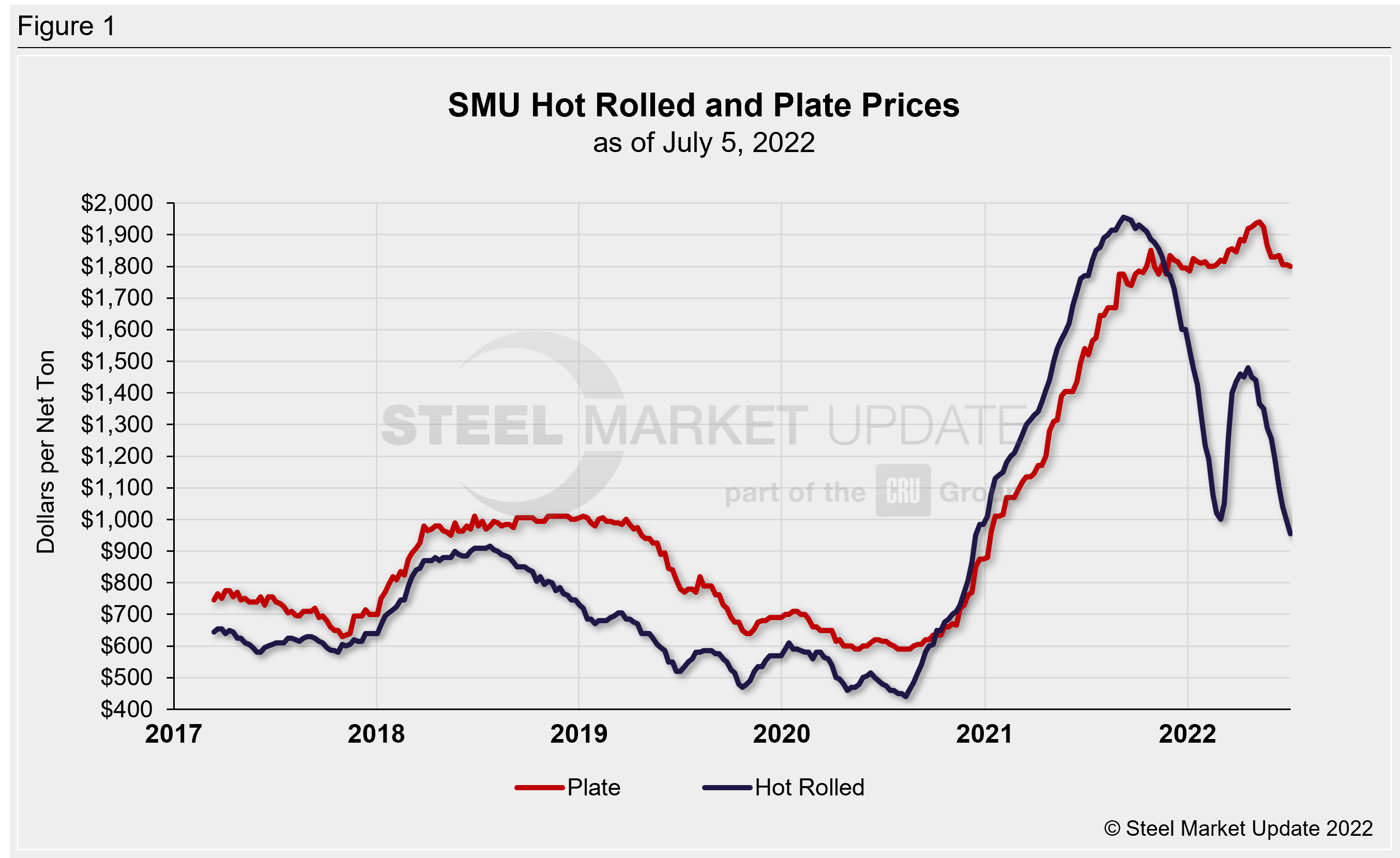

Sheet steel prices declined last week for the eleventh week in a row, while plate prices have remained relatively stable in comparison, according to SMU’s price indices published last Tuesday. Plate prices typically carry a premium over hot rolled prices because plate is a value-added product and requires more time on the mill.

SMU’s hot rolled coil index averaged $955 per ton ($47.75 per cwt) last week, the lowest level since December 2020. Recall that prior to the Russia-Ukraine war, our index had reached a 14-month low of $1,000 per ton in the first week of March, following a record-high $1,955 per ton in September 2021. Our latest plate index averaged $1,800 per ton last week. It has remained in the low- to mid-$1800s for the previous six weeks. Plate prices have declined $140 per ton from the $1,940 per ton high seen on May 10. The plate market has been much more stable compared to sheet, with our plate index remaining within $80 per ton of $1,880 per ton for more than nine months.

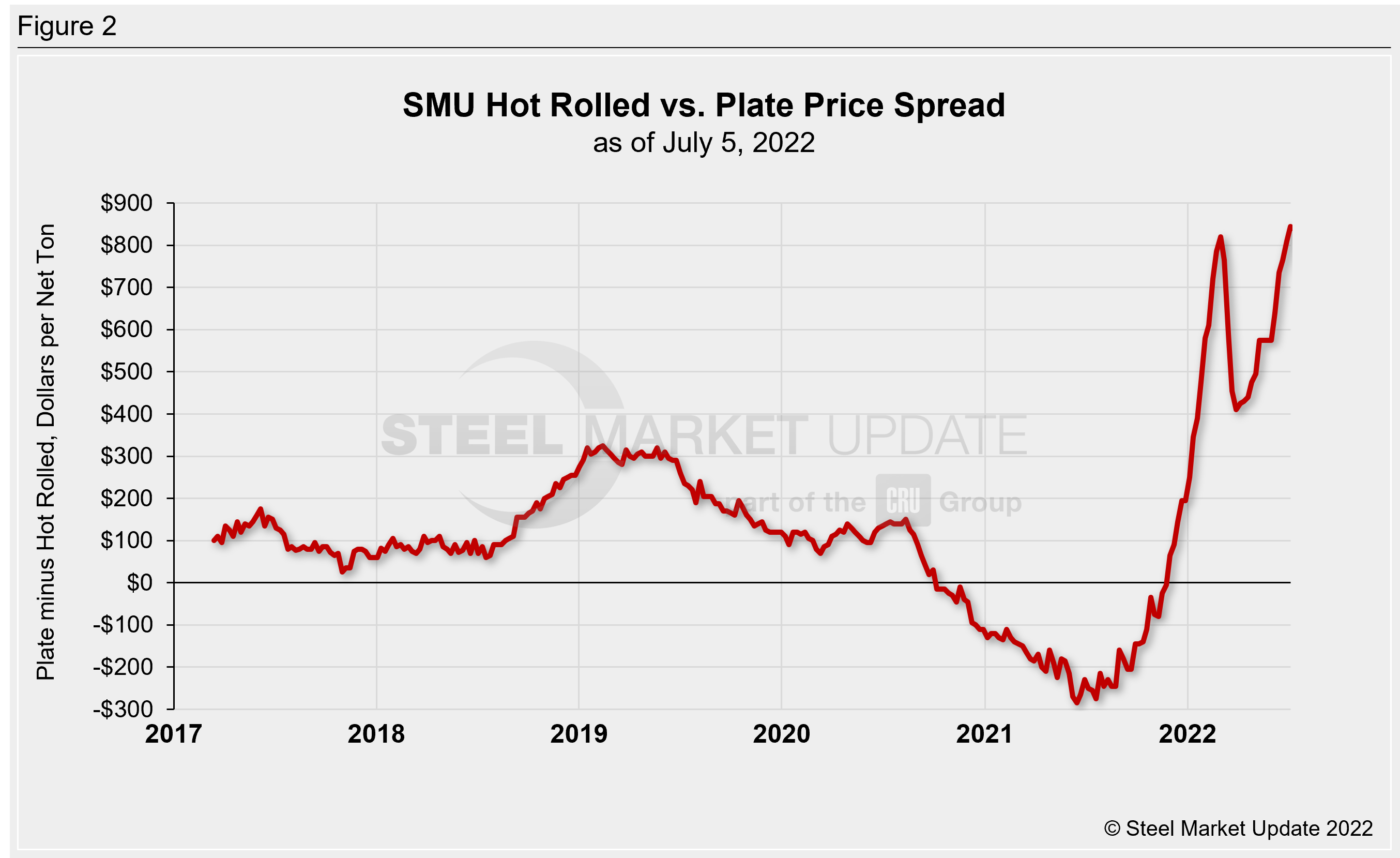

Throughout 2017 and the first half of 2018, plate prices held a roughly $100-per-ton premium over hot rolled. That premium crept up after mid-2018 to reach a high of $325 per ton by February 2019, declining thereafter until it diminished and hot rolled begain to sell at a higher price in October 2020. HRC held onto that premium until November 2021, losing it after sheet prices began declining in October and plate prices stood firm.

This year, the plate premium surged to $820 per ton by the first week of March, quickly receding to $410 by the end of the month, but rising back up each week since. As of last week, the premium has surpassed the March high, with plate now holding a $845-per-ton premium over hot rolled. The average premium held by plate over HRC for 2022 year-to-date is now $576 per ton, having risen from $535 in our early June update.

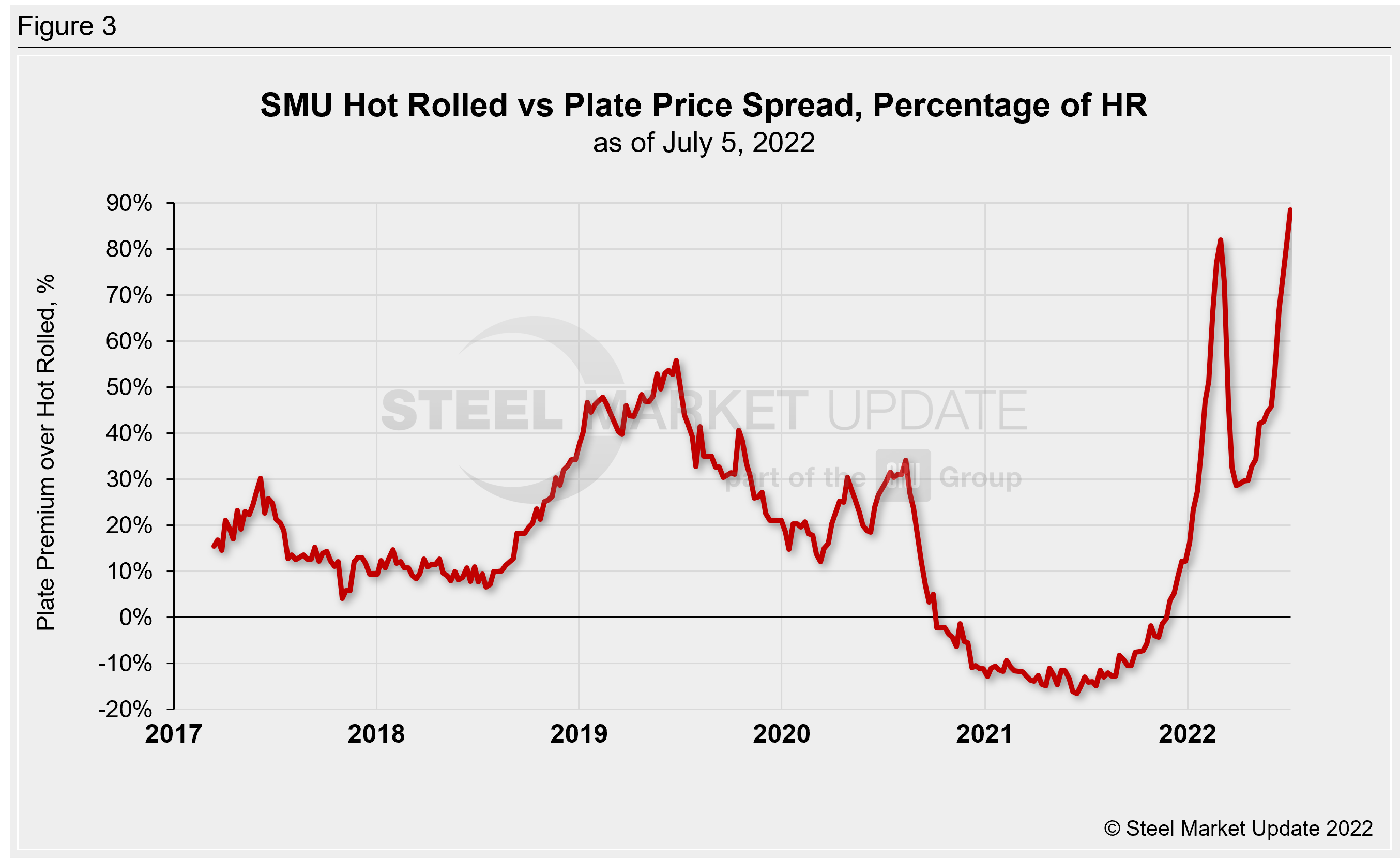

To better compare this price spread, we graphed the plate price premium over hot rolled as a percentage of the hot rolled price. This is an attempt to paint a clearer comparison against historical pricing data. Plate prices held an average premium of 16% over hot rolled in 2017, peaking at a 56% premium in June 2019. The premium declined from there and turned negative in October 2020 (when HR began to sell at a higher price than plate), falling to a low of -17% in June 2021. Plate regained its premium price in November 2021, surging to a (then) record high premium of 82% in the first week of March and falling to 29% by the end of the month. The latest plate premium is now at a new record high of 88%, having risen each of the past 14 weeks. 2022 now averages 48% YTD, up from 43% in our previous analysis.

By Brett Linton, Brett@SteelMarketUpdate.com