Prices

July 29, 2022

CRU: Handicapping the Odds of Section 232 Being Lifted in Aluminum

Written by Greg Wittbecker

By Greg Wittbecker, Advisor, CRU Group

US International Trade Commission hearings provide little direction

Last week in DC, the US International Trade Commission (ITC) held a series of public meetings and hearings to take comments on current Section 232 tariffs.

Representatives from throughout the value chain were in attendance. The Aluminum Association participated in a panel discussion along with the Aluminum Extrusion Council (AEC), Century Aluminum, The Beer Institute, Constellium, and Tri-Arrows Aluminum.

As one might expect, the positions of the respective participants depended upon their positioning within the value chain and how much of the ultimate price risk they hold in respect to Section 232 and 301.

Century, as a US producer, along with Alcoa and Magnitude 7, continue to benefit from the 10% duty on imports of aluminum. Perhaps now, more than ever, they see Section 232 as an important proponent of keeping the US industry viable. LME prices have tumbled from the mid-$3,000s per tonne to $2,400 per tonne while energy prices have skyrocketed. Preservation of the duty is a key element of their revenue foundation, and they remain a vocal supporter.

Concurrently, Canada, along with Australia and Argentina, enjoy exemption from Section 232 duties entering the US. They also like the 10% revenue enhancement that comes with the US domestic market pricing itself at the value of non-exempt supply coming from offshore. These countries are maintaining a low profile in respect to vocal support for Section 232 but do like to underscore that they are part of a very stable and reliable supply chain to keep the US supplied with primary metal.

Semi-fabrication participants such as the AEC and the major rolling mills such as Arconic, Constellium, Novelis and Tri-Arrows are positioned in the middle of the value chain. Their business model operates with metal cost, including Section 232, as a direct pass-through. Yes, Section 232 raises their costs and increases working capital. But at the end of the day, they pass most of that cost onward to their buyers as their products are indexed to the US Midwest duty PAID aluminum market. Offshore replacement is completely factored into their selling prices. Hence, they are relatively protected on price exposure to the effects of Section 232. The Aluminum Association has consistently targeted their support toward addressing China’s industry subsidies and its disruptive effect on global pricing. Their posture is best captured in the statement from Chuck Johnson, president of the Aluminum Association:

“With respect to Section 232 tariffs, the association and its members did not request relief under this tool, which chiefly aimed to support US-based primary aluminum producers,” said Johnson. “And, while the tariffs have provided some level of stability for aluminum firms up and down the value chain, they have not addressed the fundamental and ever-evolving distortions resulting from China’s rampant use of industrial subsidies in the aluminum sector. Any future actions to alter or remove the tariffs should be undertaken carefully with a stepped approach, and in a way that minimally disrupts the US market.”

Unquestionably, the biggest opponents of Section 232 are the ultimate consumers of aluminum, who stand at the end of the value chain and who really “hold the final price” in the form of an all-in aluminum price. The Beer Institute falls into this camp, as would the automobile manufacturers or any other producer who puts the aluminum “on the shelf” to the American consumer.

The Beer Institute wrote the Biden Administration on July 1 saying Section 232 was a highly regressive tax and a penalty to the consumer. They are actively seeking its removal. During the hearings, they used the platform to again challenge the validity of the Midwest Aluminum Price and APEX Act (Aluminum Pricing Examination Act).

This concern has been previously addressed by Congress, and it has not led to the investigation that this group seeks. In our view, the Beer Institute would be better served by treating Section 232 as a standalone issue than wrapping it around theories about market manipulation.

At the end of the day, no action was taken on Section 232, nor were there any expectations that the ITC would recommend anything imminently. The consensus view is that 232 will remain policy but remains a political decision.

One clear “ask” of the Biden administration, is that any decision to change Section 232 be done in a phased-in manner. This would mitigate the expected disruptive effects on near-term Midwest metal pricing and give the supply chain time to “flush” higher priced, duty-paid metal through the system without treating everyone to a financial “haircut” on the mark-to-market loss resulting from a sudden change in duty structure.

The Midwest market does not seem to believe in the status quo on Section 232

Notwithstanding all the above, the US physical aluminum ingot market is on edge about the status of Section 232. Spot premiums are hovering around $.28 per pound, having corrected down from their highs near $.40 per pound at the outset of the war in Ukraine. There is no doubt in the early stages of the war that the market was operating on imperfect information about how Russian exports would be handled. Initial reactions were for the absolute worst, meaning a major cut-off of supply. That got priced into the market. Now, with the benefit of five months of additional observation, those fears of a wholesale suspension have faded. We are going through a process of self-sanctioning Russian supply, but Russian metal is still around, and shortages are not apparent.

The market now seems much more focused on recession, especially in Europe. Earlier this week, the IMF lowered its 2022 World GDP forecast from 3.6% growth to 3.2% growth. This compares to 6.1% growth in 2021. Germany headlines the downturn with GDP growth expected to slow to just 1.2%

While the US growth rate is still projected to be 2.3%, many players in the market are also beginning to handicap the higher probability of Section 232 coming off on aluminum.

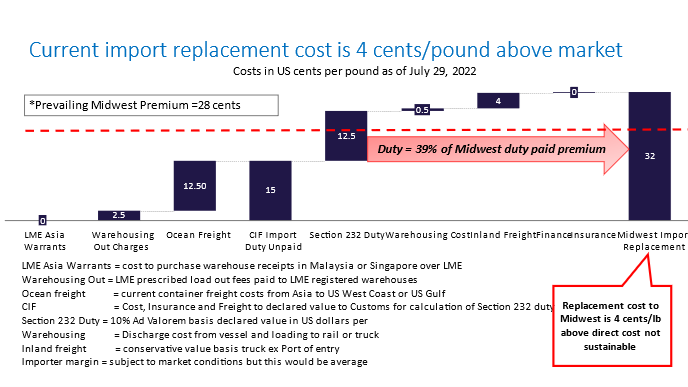

This is best shown in the bridge chart below, showing how much import replacement is being discounted (click to expand).

The physical aluminum market is extremely efficient, and the traders handling imports are no fools. No one would consistently discount replacement this much for any extended period in the belief that they could make money “shorting” the premium. In 2021, we DID see Midwest premiums fall to a low of $26.50 cents/pound over LME. It is possible that some traders have been bearish on the global economy and that shorting the Midwest can be profitable. However, given the uncertainties around Russian supply later in the year and the very low stocks in the US now, we think the risk versus reward of that trade is not favorable.

Instead, we believe we may be seeing some premium “long” liquidation taking place. Traders have had a very good, long-term rise in premiums since the outset of the pandemic. They may want to take money off the table now before getting blindsided by the Biden Administration on Section 232.

The Administration’s talk of lifting Section 301 duties on China to help blunt inflationary trends on consumer prices is a tip-off. Why think that Section 232 could not be included in that approach? If the Beer Institute gets support from automakers and other consumer goods OEMs, there could be pervasive arguments for a change. It might not be a permanent removal of the duty, but something to help take the edge off inflation.

The trade reads the same signals as we do. It is the smart play for them to lower exposures now. If nothing happens, they have opportunity cost if premiums rebound. However, they do not give back all the money they made on the ride up.

Stay tuned. If anything is going to happen, it will come in the next 60 days as the Biden administration will want to time this to get maximum benefit ahead of the mid-term elections in November.

For more information about this topic, contact the author gregory.wittbecker@crugroup.com.

Learn more about CRU’s services at www.crugroup.com.