Market Data

October 4, 2022

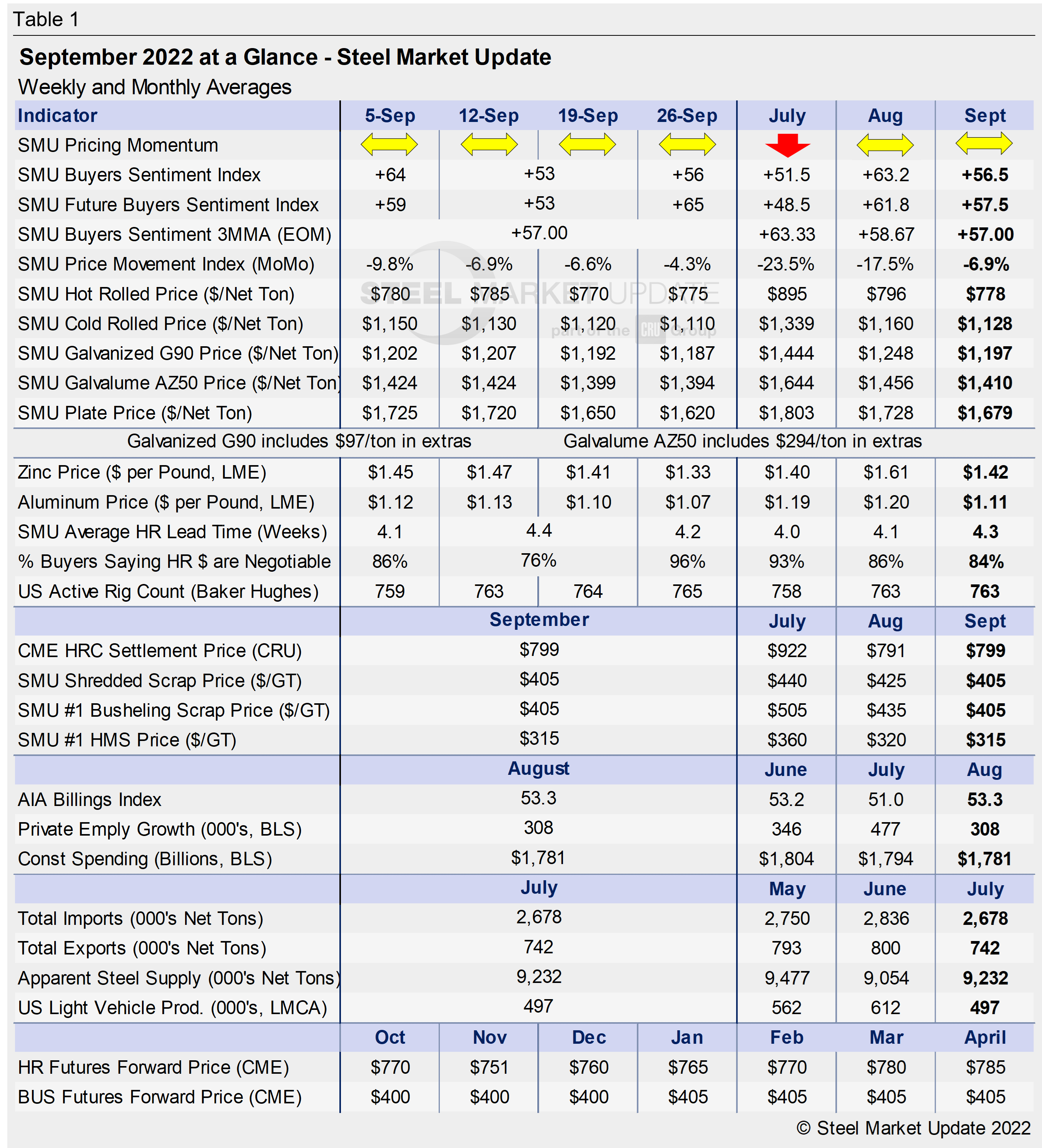

SMU's September at a Glance

Written by Brett Linton

Steel prices were steady to slightly down throughout the month of September, following declines seen in each of the four months prior. Hot-rolled prices averaged $780 per ton ($39.00 per cwt) the first week of September, falling to a low of $770 per ton in the third week of the month, and rising to $775 per ton as of last Tuesday. Recall that hot-rolled prices also reached the same low of $770 per ton in the middle of August. The SMU Price Momentum Indicator for flat-rolled products remained at Neutral since it’s adjustment on August 9th. Price Momentum on plate remained at Lower since our May revision.

Raw material prices eased further last month. Scrap prices fell another $5-30 per gross ton from August, with busheling and shredded prices both averaging $405 per ton. Sources expect scrap prices to decline slightly again in October. Zinc and aluminum spot prices fell throughout September, with both products now nearing lows seldom seen in the last year. You can view and chart more multiple products using our interactive pricing tool here.

The SMU Buyers Sentiment Index remained positive but ticked down throughout September, moving from +64 to +56. Future Sentiment has been fluctuating, falling to +53 mid-month, then jumping back up to +65 by month end. Viewed as a three-month moving average, Buyers Sentiment fell to +57.00 through the end of the month, the lowest level recorded since mid-October 2020.

Hot rolled lead times averaged 4.3 weeks in September, slightly higher than July and August levels, but still relatively short historically. The percentage of buyers reporting that mills are willing to negotiate on prices remains high. Through last week, 96% of hot-rolled buyers reported that mills were willing to talk price to secure an order. A history of HRC lead times can been found within our interactive pricing tool.

Key indicators of steel demand remain positive overall, though not at the bullish levels seen earlier this year. The energy market continues to slowly recover. And while construction has slowed, activity has remains at solid levels. Import and export volumes both declined in July, though apparent steel supply remains healthy at over nine million tons. Total imports are expected to decline further into August, according to recently released data.

See the chart below for other key metrics in the month of September:

By Brett Linton, Brett@SteelMarketUpdate.com