Market Data

October 28, 2022

Consumer Confidence Edges Down in October

Written by David Schollaert

US consumer confidence slipped in October after two straight monthly increases amid rising concerns about inflation and a possible recession next year. Despite the decline, households remain keen to purchase big-ticket items like motor vehicles and appliances, The Conference Board reported.

Though down, October’s results still pointed to decent consumer buying, as more consumers planned to buy a home over the next six months — despite soaring borrowing costs — and correlating well with the recent GDP growth reported for the third quarter.

“Consumer confidence retreated in October, after advancing in August and September,” said Lynn Franco, The Conference Board’s senior director of economic indicators. “The Present Situation Index fell sharply, suggesting economic growth slowed to start Q4. Consumers’ expectations regarding the short-term outlook remained dismal. The Expectations Index is still lingering below a reading of 80 — a level associated with recession — suggesting recession risks appear to be rising.”

The headline Consumer Confidence Index fell by 5.3 points in October to a reading of 102.5. The decline comes after back-to-back monthly increases as American households were impacted by rising inflation concerns, with both gas and food prices serving as main drivers, according to the report.

“Looking ahead, inflationary pressures will continue to pose strong headwinds to consumer confidence and spending, which could result in a challenging holiday season for retailers,” added Franco. “And, given inventories are already in place, if demand falls short, it may result in steep discounting which would reduce retailers’ profit margins.”

The Present Situation Index, which measures consumer sentiment toward current business and labor market conditions, fell to 138.9 from 150.2 last month. The Expectations Index, which assesses the short-term outlook for income, business, and labor market conditions, slipped to 78.1 from 79.5.

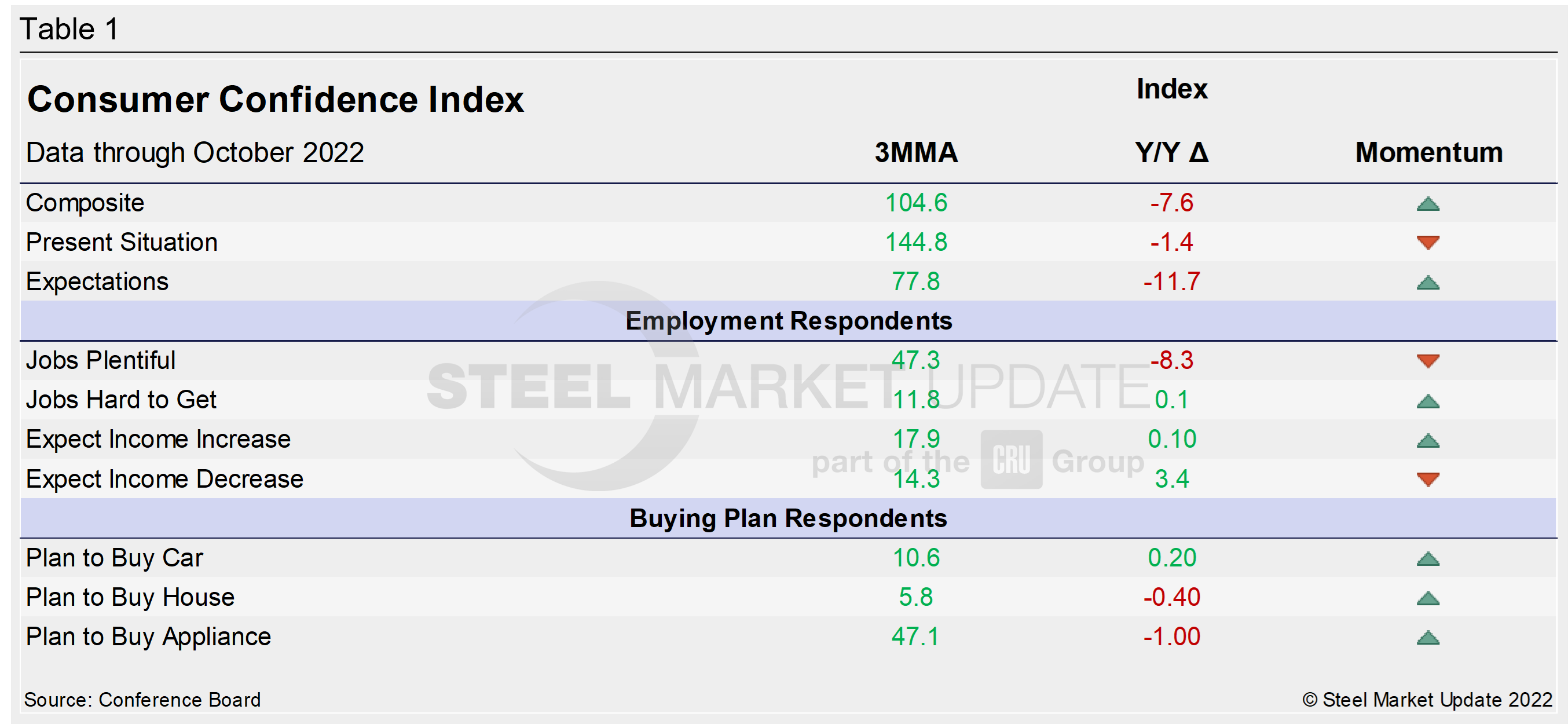

Calculated as a three-month moving average (3MMA) to smooth out volatility, The Conference Board’s Composite Index was 104.6, a 2.4-point increase versus September. The figure has now risen for three straight months but remains well behind a pre-pandemic high of 130.4 in February 2020.

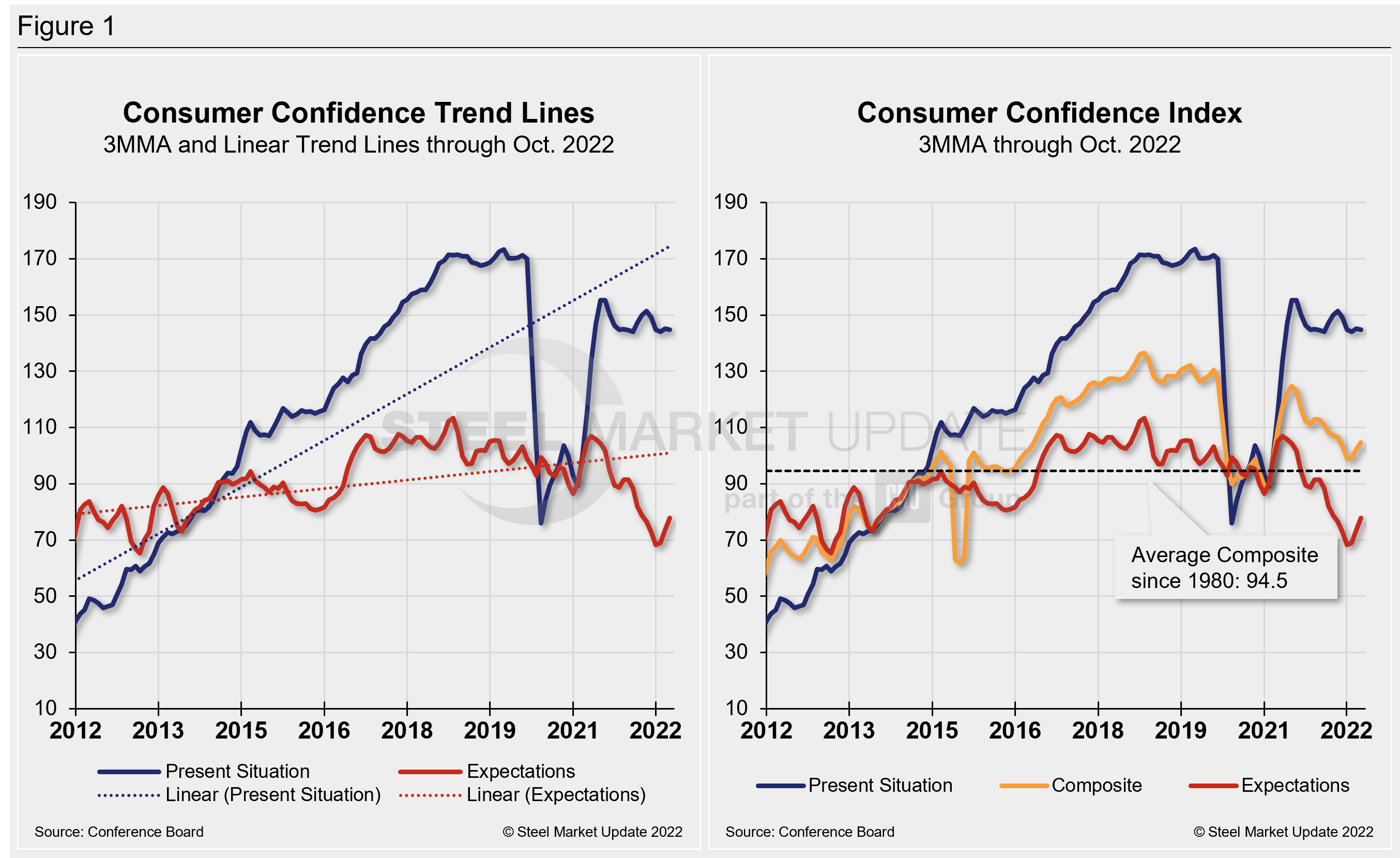

The Composite Index is made up of two sub-indexes: consumers’ view of the present situation and their expectations for the future. Figure 1 below notes the 3MMA linear trend lines from January 2012 through October 2022 versus the trend lines of all three subcomponents of the index: Present Situation, Composite, and Future Expectations. All three were above the average composite line prior to the pandemic before falling consecutively through February 2021. The surge from March through June of 2021 pulled all three indexes above the composite line once again. But economic uncertainty has since really eroded confidence and expectations, despite present recovery.

The table below compares October 2022 with October 2021 on a 3MMA basis. The headline index and its two sub-indexes have all been declining on a year-on-year (YoY) basis. Present Situation has seen a less aggressive fall, but two out of three are down notably, with Expectations showing the most volatility over the same period. Present Situation, however, is showing declining momentum through October.

When compared to the same 2019 pre-pandemic period, the Composite Index is down 21.5 points on a 3MMA basis. The Present Situation is down 28.7 points, while the Expectations reading is down 16.7 points this month when compared to the same period in 2019. The Consumer Confidence report includes employment data and purchase plans. These are summarized in the table below.

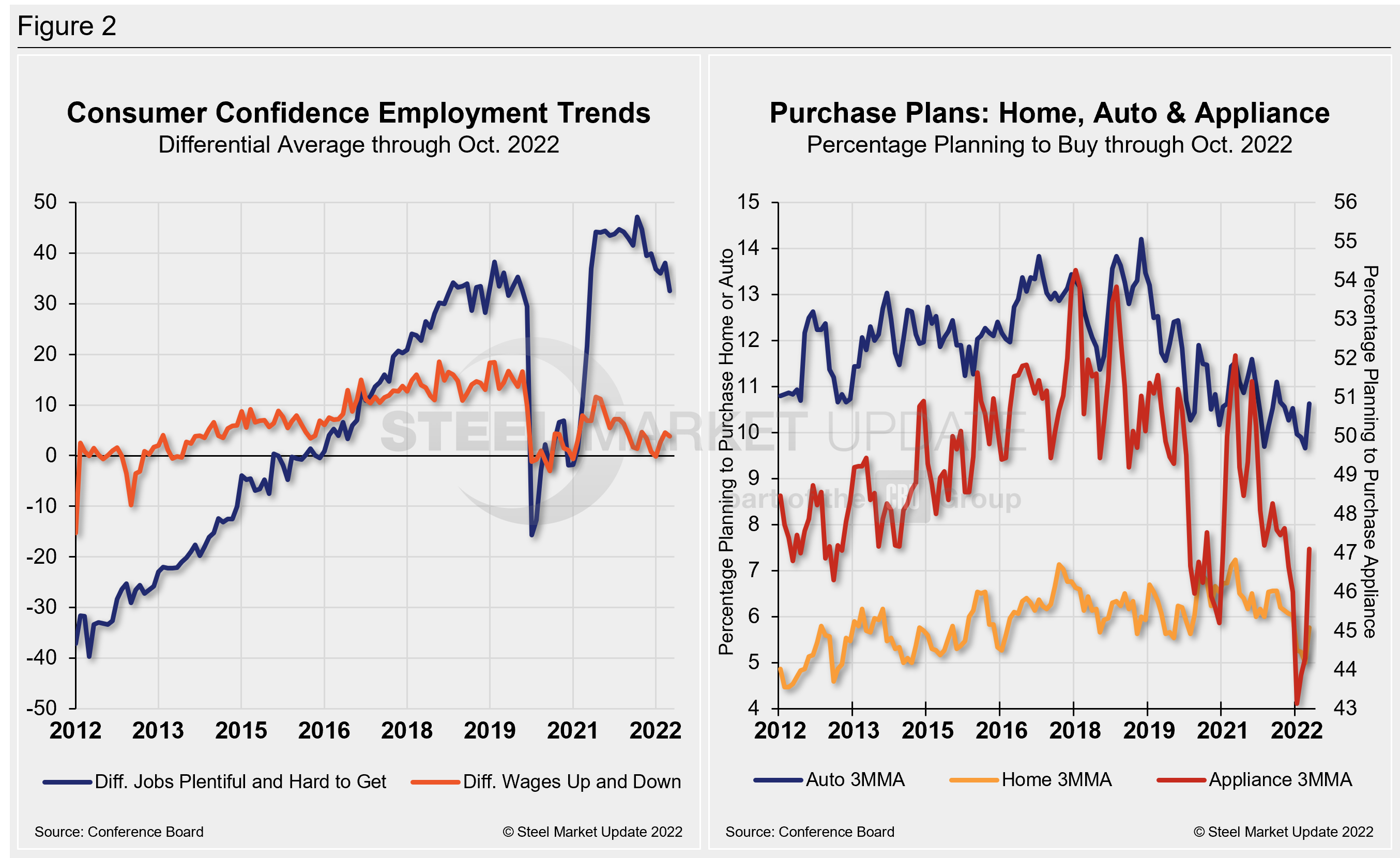

People found jobs less plentiful in October but were more optimistic about wage increases compared to the month prior. The differential between those finding jobs and those having difficulty was 32.5 in October, down from 38.1 in September. The measure is trending further way from the most recent pre-pandemic high of 44.1 seen just a year ago. The difference between those expecting wages to rise versus those expecting wages to fall is 3.8, down 0.7 points MoM, and well removed from the recent high of 11.6 last June.

Buying intentions for big-ticket items — cars, homes, and major appliances — were all surprisingly improved in October. Even as consumers worried about the economy’s outlook, they remained interested in buying big-ticket items over the next six months, though they pulled back on travel plans, the report said.

The share of consumers planning to buy motor vehicles increased to the highest level since July 2020. More consumers planned to buy appliances such as refrigerators and washing machines. Consumers were also more inclined to buy a house, probably encouraged by a sharp slowdown in house price inflation.

Home buying saw the largest percentage increase in October, up 36%, followed by car buying (+25.3%), while major appliance buying was up just 2.7% over the same period. These recent dynamics and historical movements are illustrated below in Figure 2.

Note: The Conference Board is a global, independent business membership and research association working in the public interest. The monthly Consumer Confidence Survey®, based on a probability-design random sample, is conducted for The Conference Board by Nielsen. The index is based on 1985 = 100. The composite value of consumer confidence combines the view of the present situation and of expectations for the next six months.

By David Schollaert, David@SteelMarketUpdate.com