Analysis

December 1, 2022

Hot Rolled Futures in the December Doldrums

Written by Michael D'Angelo

Editor’s note: SMU Contributor Michael D’Angelo is a researcher and trader at Marex. In his role, Mike performs fundamental and quantitative analysis, which directly leads to actionable trading/risk management strategies across the base, precious, and ferrous metals derivative spaces. Prior to joining Marex, Mike received a BA in economics with a minor in finance from Princeton University. Mike can be reached at mdangelo@marex.com for comments/questions.

CRU’s weekly Midwest HRC index stabilized this week, coming in at $626 per net ton, down just $1 from the previous week. However, this week marked the sixth straight week the index has fallen, and it has been down nine out of the last ten weeks.

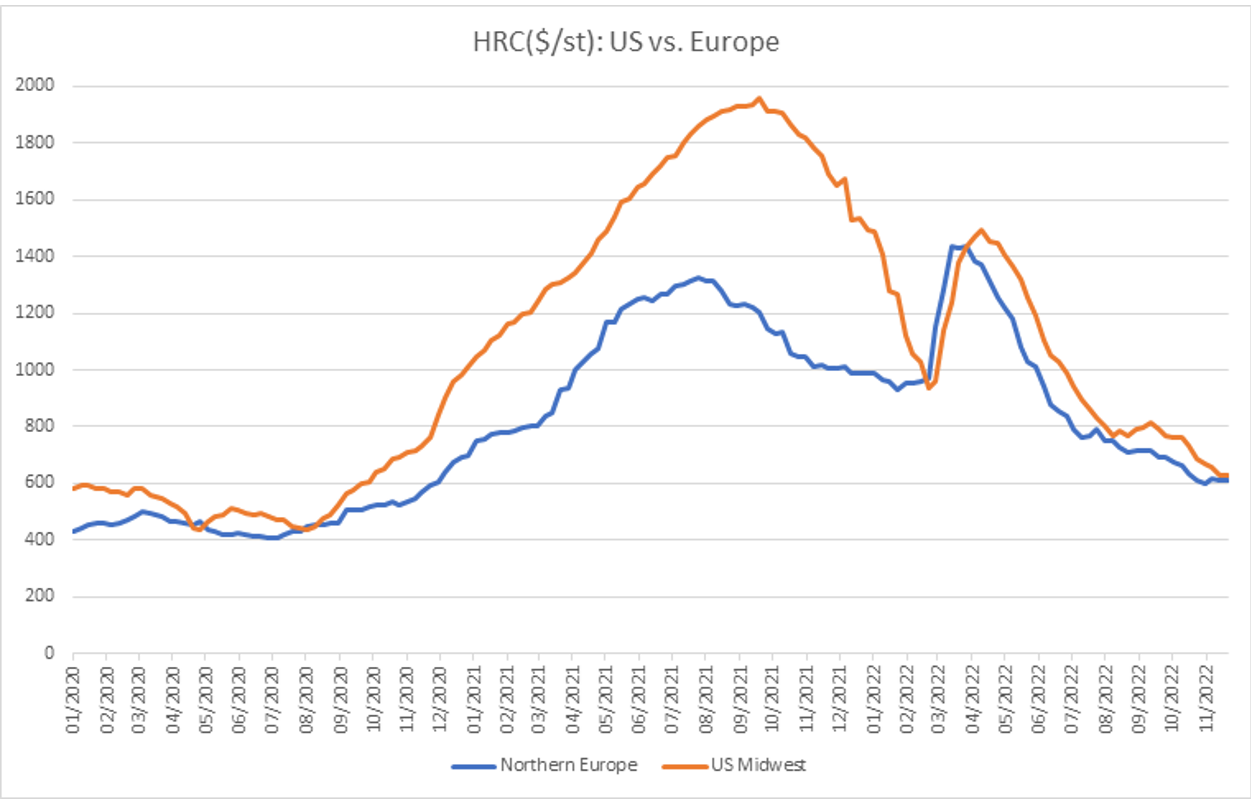

As seen above, Midwest HRC has been declining while European HRC has been steady over the past few weeks, which has caused the spread between Midwest and European HRC to close. Midwest spot is currently only trading at about a $15 premium to Northern Europe now.

Trading activity has been muted in Europe which is standard as the holidays are approaching. Some deals are happening within a tight range of €600-650/metric ton (US$630-684/metric ton).

While not much tends to happen in December, sentiment in the US does appear to be turning up. Last week, market participants had anticipated mills raising prices in the near future. This past Monday, leading producer Cleveland-Cliffs announced a $60/ton increase in spot market prices. Other steelmakers have since followed.

On the economic data front, GDP, Durable Goods Orders, Dallas Fed Manufacturing Activity, and University of Michigan Consumer Sentiment all slightly beat expectations last week.

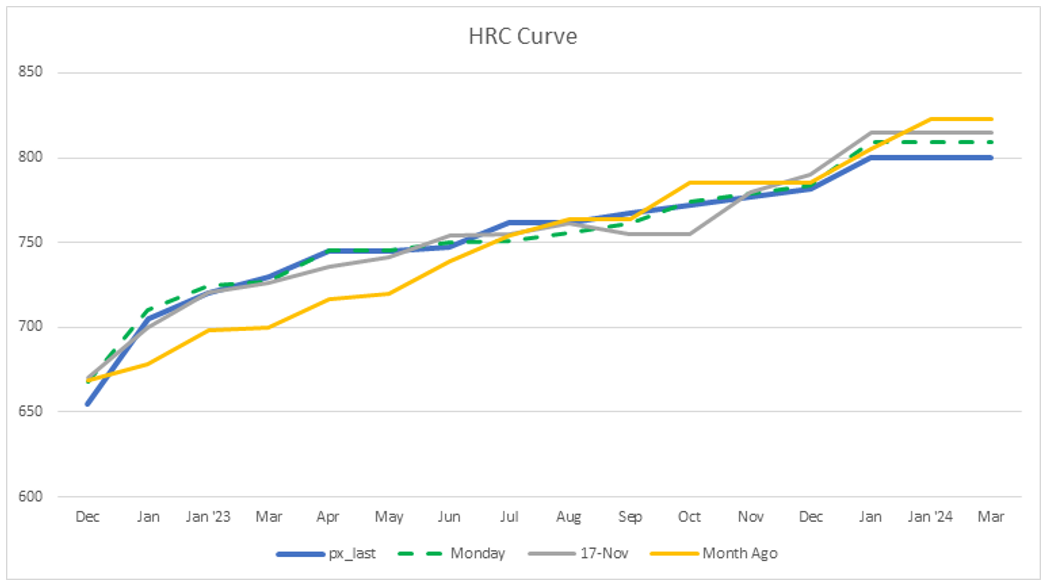

The CME futures curve hasn’t moved much over the past month. Dec is still trading at $655/ton despite the previous two CRU points being about $627 and $626.

Notably, the front end of the curve has steepened with Dec/Jan now valued at about $50 contango, Dec/Mar at $70 contango, and Dec/Q2 ’23 at $90 contango.

This is reflective of steel seasonality which tends to be strong in Q1, whereas consumers typically only buy hand over fist into year end. Market consensus seems to be that prices will remain in the mid $600/ton range before rallying in the new year. However, a continued economic downturn would likely prevent prices from rallying far.

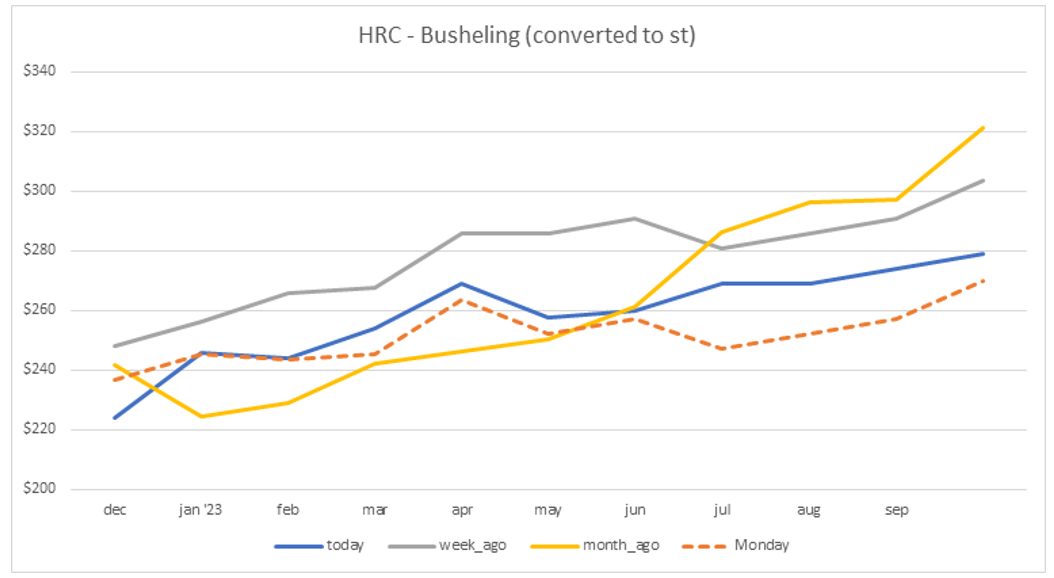

The spread between HRC and busheling is currently about $220/ton, down from $250 last Friday, suggesting that mill margins continue to fall. However, if the futures curves are any indication, the spread should recover about $30-60 next year.

Several mills have halted larger HRC deals below $600/ton, citing that finished steel prices have gotten too close to the cost of production.

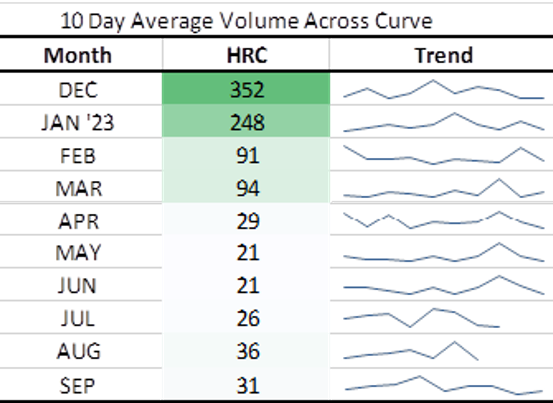

Above are the average trading volumes for each HRC contract; liquidity has been drying up into year end.

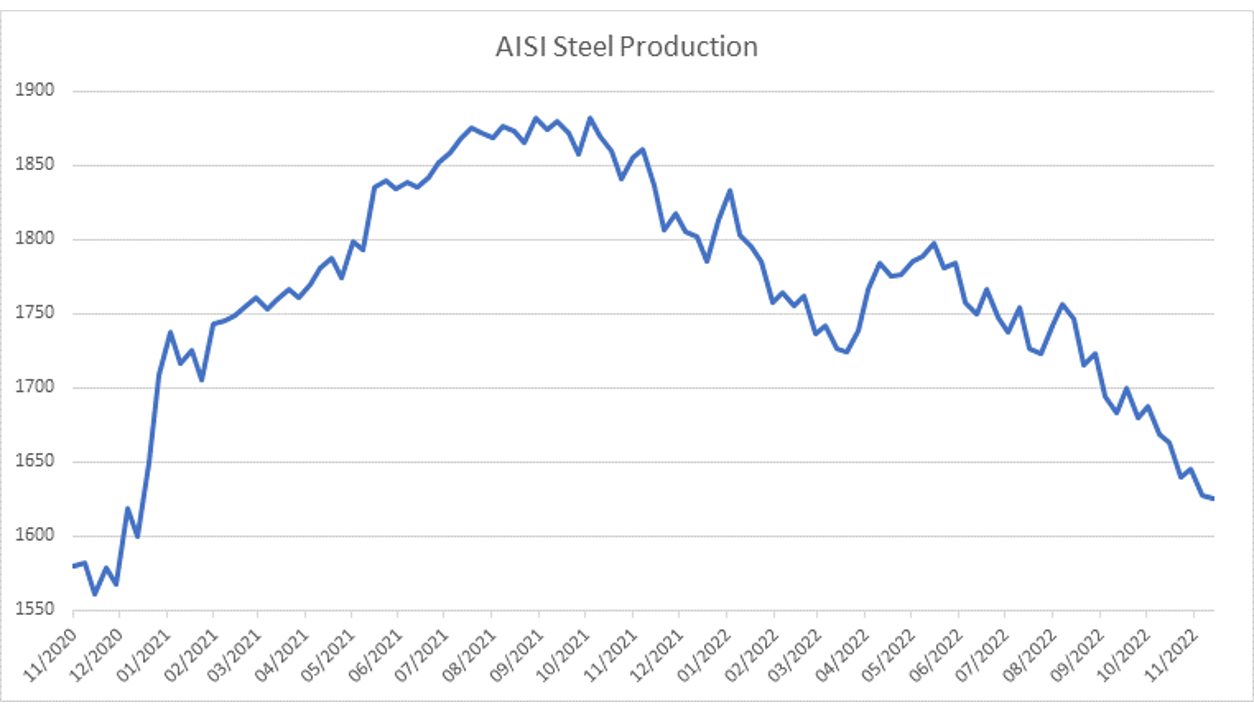

US steel production (AISI data) continues to plummet. Production fell again during the week ending Nov. 26, this time by 3,000 tons to 1.625 million tons, which is the lowest level since early January 2021. The US steel capacity utilization rate inched down to 72.8% from 73.0%.

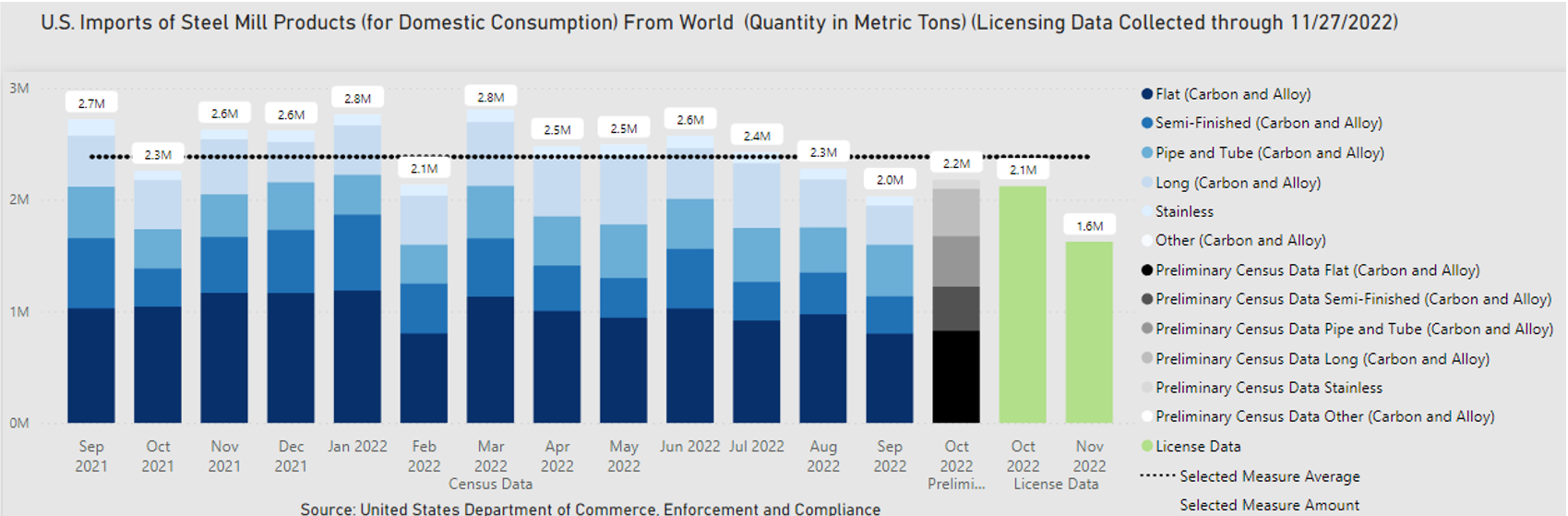

Based on licensing data, imports for the first 27 days of November were projected to be 1.6 million metric tons, implying just 1.8 million metric tons for the month, which would be the lowest since February 2021. Imports, along with AISI domestic production, put into perspective how weak demand has been.

Economic Data of Note

Nov. 23 – Durable Goods Orders: 1.0% (Est. 0.4%)

Nov. 23 – U. of Mich Sentiment: 56.8 (Est. 55.0)

Nov. 28 – Dallas Fed Manufacturing Activity: -14.4 (Est. -21.0)

Nov. 30 – GDP Annualized QoQ: 2.9% (Est. 2.8%)

Dec. 1 – Personal Spending: 0.8% (Est. 0.8%)

Dec. 1 – Construction Spending MoM: -0.3% (Est. -0.2%)

Dec. 2 – Wards Total Vehicle Sales

Dec. 2 – Unemployment Rate

By Michael D’Angelo, Marex, mdangelo@marex.com