Market Data

December 22, 2022

Consumer Confidence Surprises in December, Gains Ground

Written by David Schollaert

US consumer confidence provided a bit of a boost and a hopeful sign for the economy as it bounced back in December. Following back-to-back monthly declines, the headline index in December rose sharply as American consumers’ confidence in the economy grew as high inflation continued to ease, The Conference Board reported.

The headline Consumer Confidence Index rose 6.9 points to 108.3 in December from 101.4 one month ago.

The business think tank’s latest consumer confidence index saw a significant jump from the upwardly revised measure in November, and ahead of consensus estimates the index would come in at 101.

December’s measure is the highest reading for the index since April 2022, the report said.

“The Present Situation and Expectations Indexes improved due to consumers’ more favorable view regarding the economy and jobs,” said Lynn Franco, The Conference Board’s senior director of economic indicators. “Inflation expectations retreated in December to their lowest level since September 2021, with recent declines in gas prices a major impetus.”

The latest survey showed that consumers’ intentions to spend money on vacations advanced but plans to purchase homes and big-ticket appliances cooled further, a trend likely to continue into 2023, Franco said. “This shift in consumers’ preference from big-ticket items to services will continue in 2023, as will headwinds from inflation and interest rate hikes.”

The Present Situation Index, which measures consumer sentiment toward current business and labor market conditions also improved in December after repeated declines in October and November. The index rose 4.9 points to 147.2. The Expectations Index, which assesses the short-term outlook for income, business, and labor market conditions, rose to 82.4 from 76.6 the month prior.

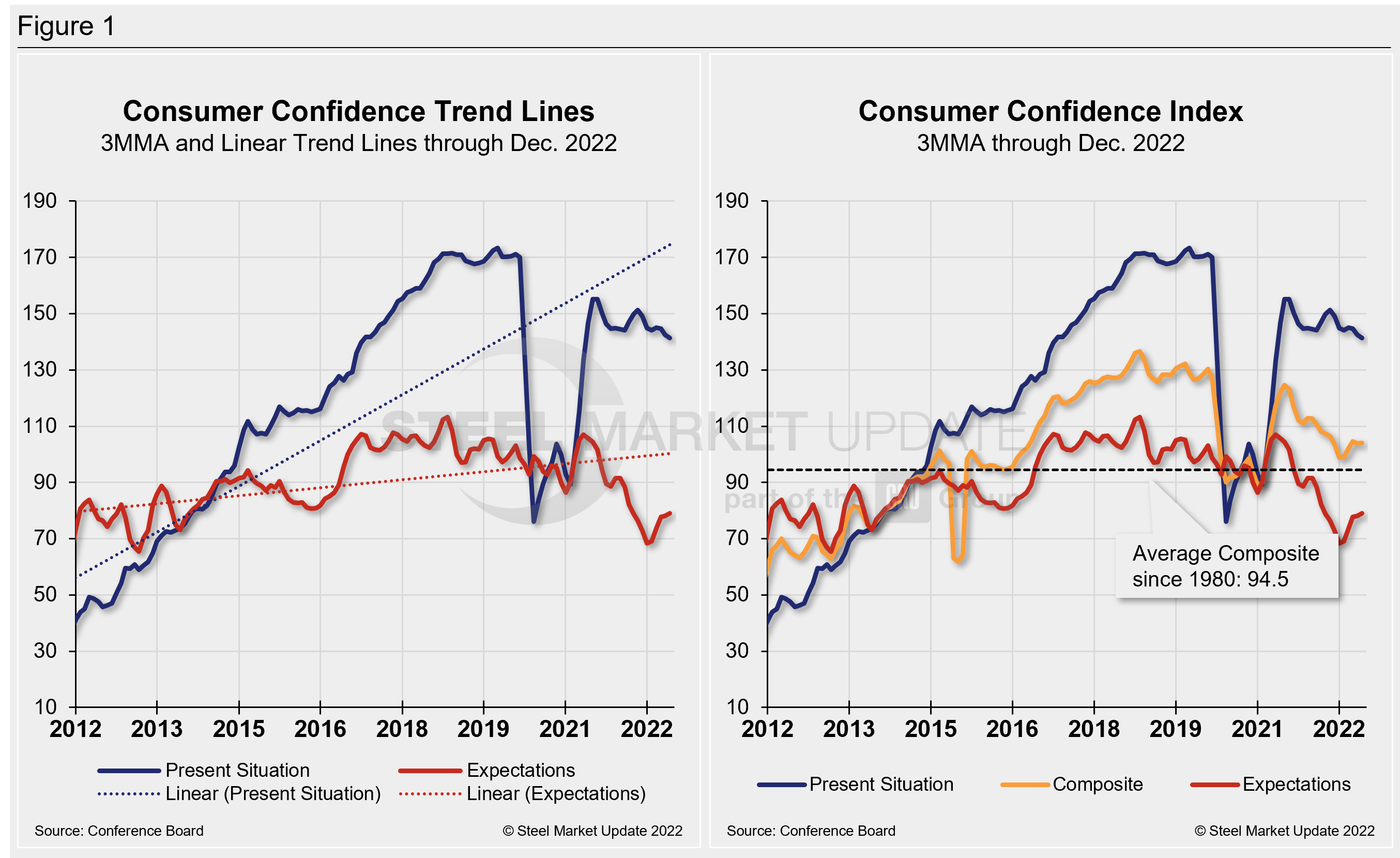

Calculated as a three-month moving average (3MMA) to smooth out volatility, The Conference Board’s Composite Index was 104, a 4.8-point increase vs. November. The figure rebounded after slipping for the first time in four months in November. Despite the recovery, the reading remains well behind a pre-pandemic high of 130.4 set in February 2020.

The Composite Index is made up of two sub-indexes: consumers’ view of the present situation and their expectations for the future. Figure 1 below notes the 3MMA linear trend lines from January 2012 through December 2022 vs. the trend lines of all three subcomponents of the index: Present Situation, Composite, and Future Expectations. All three were above the average composite line prior to the pandemic before falling consecutively through February 2021. The surge from March through June of 2021 pulled all three indexes above the composite line once again. But economic uncertainty continues to weigh on confidence and expectations.

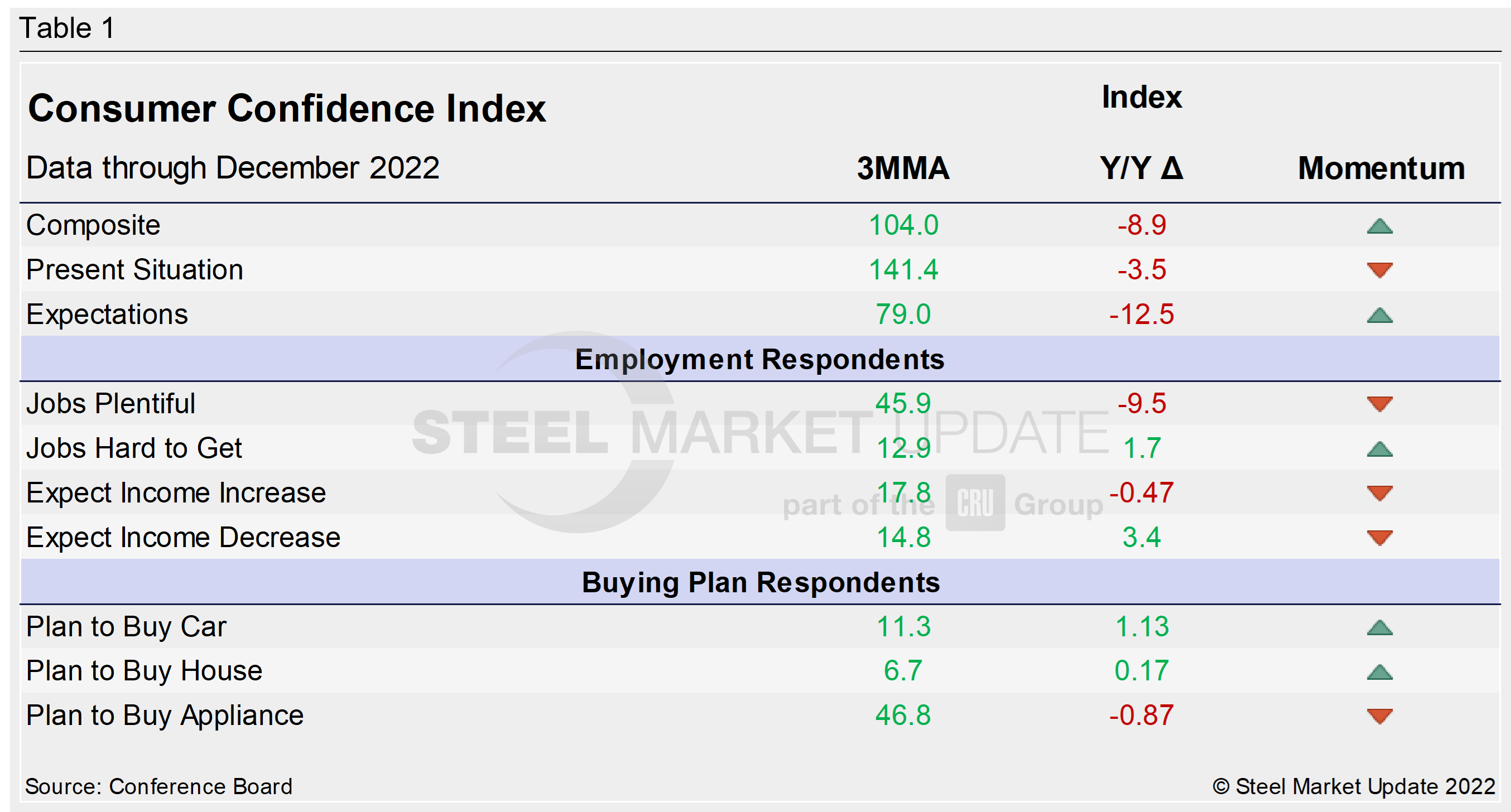

The table below compares December 2022 with December 2021 on a 3MMA basis. The headline index and its two sub-indexes have all been declining on a year-on-year (YoY) basis. Present Situation has seen a less aggressive fall, but they are all down notably, with Expectations showing the most volatility over the same period. Only the Present Situation, though, is showing declining momentum through December.

When compared to the same 2019 pre-pandemic period, the Composite Index is down 23.1 points on a 3MMA basis. The Present Situation is down 28.8 points, while the Expectations reading is down 19.3 points this month when compared to the same period in 2019. The Consumer Confidence report includes employment data and purchase plans. These are summarized in the table below.

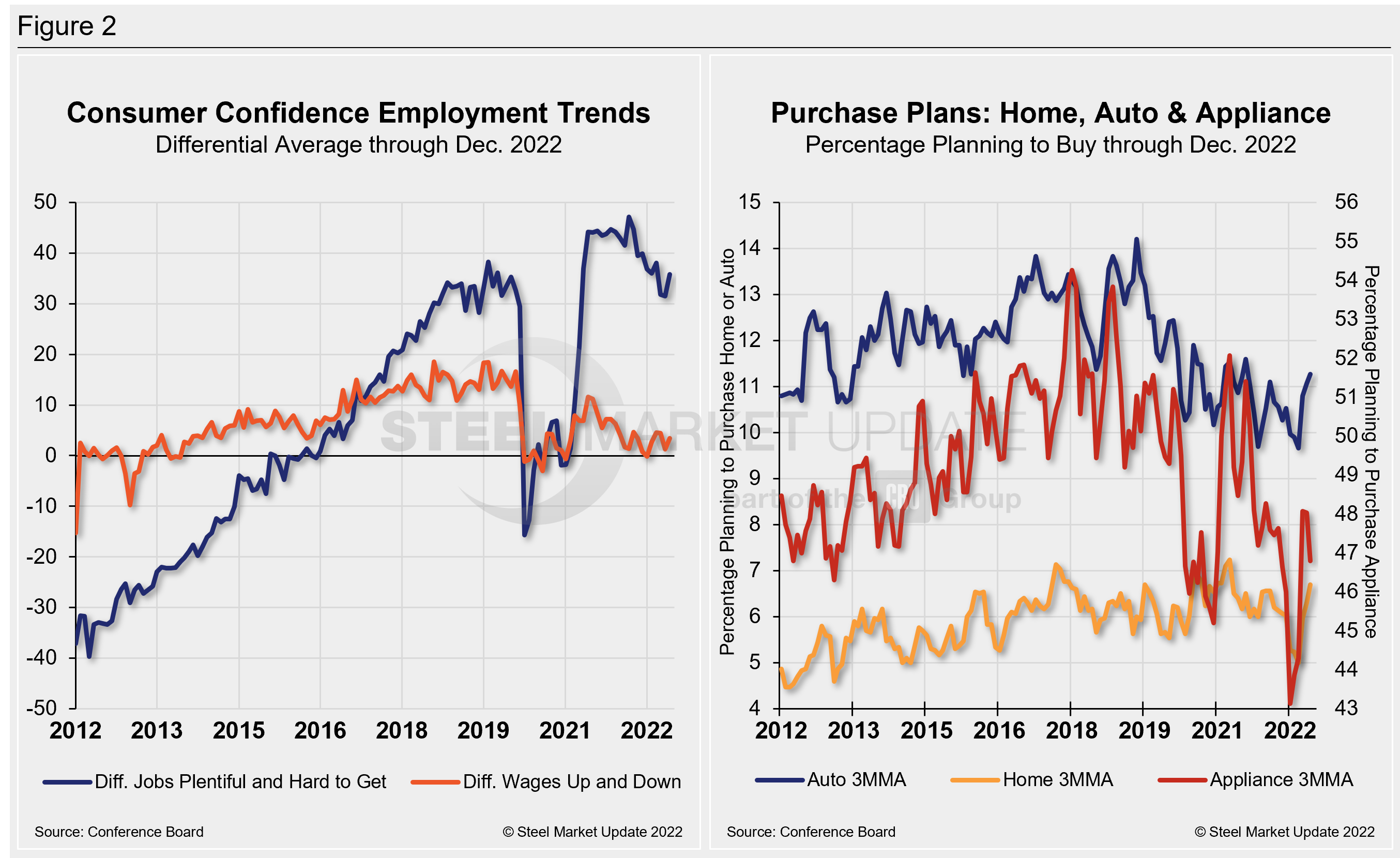

People found jobs more plentiful in December but were far less optimistic about wage increases compared to the month prior. The differential between those finding jobs and those having difficulty was 35.8 in December, up from 31.5 in November. The measure, though up month on month (MoM), is still trending further away from the most recent pre-pandemic high of 44.1 seen just about a year ago. The difference between those expecting wages to rise vs. those expecting wages to fall is 3.4, up 2.1 points MoM, and well removed from the recent high of 11.6 last June.

Buying intentions for big-ticket items — cars, homes, and major appliances — were mostly down in December, though auto buying improved ever so slightly MoM. The results continue to indicate that consumers continue to worry about the economy’s outlook, showing less interest in buying big-ticket items over the next six months, but have increased their travel plans, the report said.

The share of consumers planning to buy motor vehicles rose just 0.1 points MoM in December after falling by 2.5 points the month prior. Fewer consumers planned to buy appliances such as refrigerators and washing machines. Consumers were also less inclined to buy a house, as interest rates continue to rise amid high inflation.

Auto buying improved in December, up 1%. Home buying saw the sharpest decline, down 4.6% MoM in December, followed by major appliance buying (-4%) over the same period. These recent dynamics and historical movements are illustrated below in Figure 2.

Note: The Conference Board is a global, independent business membership and research association working in the public interest. The monthly Consumer Confidence Survey®, based on a probability-design random sample, is conducted for The Conference Board by Nielsen. The index is based on 1985 = 100. The composite value of consumer confidence combines the view of the present situation and of expectations for the next six months.

By David Schollaert, David@SteelMarketUpdate.com