Market Segment

February 2, 2023

Hot Rolled Futures: Cliffs Price Hike Boosts HRC Gains

Written by David Feldstein

Editor’s note: SMU Contributor David Feldstein is president of Rock Trading Advisors. Rock provides customers attached to the steel industry with commodity price risk management services and market intelligence. RTA is registered with the National Futures Association as a Commodity Trade Advisor. David has over 20 years of professional trading experience and has been active in the ferrous derivatives space since 2012.

If the groundhog sees his shadow, does the rally continues for another six weeks? Something like that? Today is Groundhog Day, and that can only mean one thing… we got January’s auto sales data yesterday. Ward’s Total Vehicle Sales jumped to a better-than-expected 15.74 million seasonally adjusted annual rate (SAAR) in January.

Ward’s U.S. Auto Sales SAAR

So it shouldn’t be terribly surprising that auto-heavy Cleveland Cliffs announced yet another price increase today. I can’t help but wonder if the auto supply chain is due for a restocking following last year’s paltry 13.7 million light vehicles sold. Oil-country-tubular-goods (OCTG) prices exploded last year as the energy industry returned after hibernating in 2020. My understanding is the energy industry is roughly 10% of flat-rolled demand, while transportation accounts for 30% of demand.

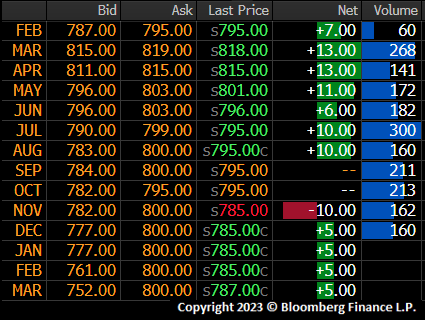

The hot-rolled coil (HRC) futures curve reacted to today’s price hike announcement with $10 – $15 gains in the March through August futures as of settlement, which now occurs at 11:00 a.m. CST.

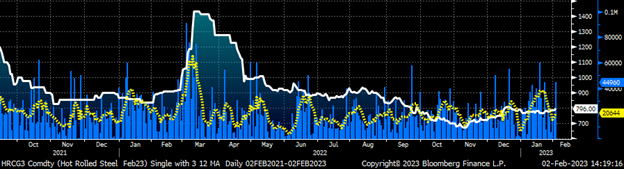

In the chart below, the vertical blue lines show the daily volume total for all months on the curve. The yellow line is a 5-day moving average, which turned sharply lower last week. This was likely due to the Chinese Lunar New Year holiday slowing liquidity across the ferrous futures landscape. However, today’s trading volume jumped above 45k tons.

February CME HRC Future $/st w/ Aggregate Curve Volume & 5-Day Avg.

The HRC futures market bottomed on Nov. 9. Since then, the futures curve has shifted from a steep contango (upward sloping) to relatively flat. However, the March and April futures have rallied ahead of the other months so far this week, perhaps indicating the curve is in the early stages of shifting from flat into backwardation (downward sloping).

CME Hot Rolled Coil Futures Curve $/st

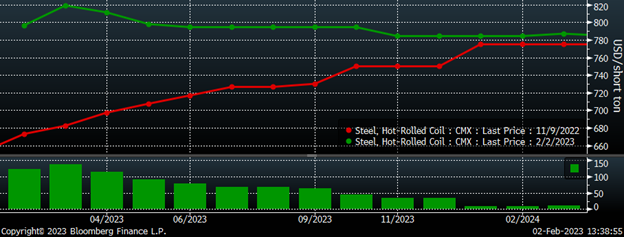

For the past three months, open interest has remained steady around 475k tons. Will we see open interest expand as it did starting in early February 2020? Since bottoming at $633 on Nov. 9, the rolling second month future has gained 29.4%. Rule of thumb is the 20% threshold indicates a bull or bear market, so by that metric, HRC futures are in a bull market. However, rule of the other thumb is for it to be a strong bull/bear market, open interest has to be expanding.

Rolling 2nd Month CME Hot Rolled Coil Future $/st & Open Interest

Sneaky tight flat-rolled fundamentals, perhaps a restocking in auto, China, Europe, and some other factors could prove to be upside catalysts. BMO analyst David Gagliano noted “some market sources indicating spot tightness has emerged in the Midwest and the South” in not one, but two of his daily email updates this week.

That’s the first I’ve seen of said vocabulary in a long time. Mexican steelmaker AHMSA’s production issues and complications at Steel Dynamics Inc.’s (SDI’s) Sinton mill in Texas have tightened the southern market, relatively speaking.

Historically, we have seen meteoric HR rallies preceded by a clustering of supply-side issues that compound until the proverbial straw that breaks the camels back. We saw this in 2014 and again in early 2021, the former being the accident at Middletown, Ohio, and the latter February’s ice storm across the deep South and Texas. Are these two production issues just the beginning?

The latest potential hiccup revealed itself earlier this week as maintenance on a number of dams along the Illinois river system that connect Lake Michigan and Chicago to the Mississippi River will take place from June 1 through Sept. 30.

This will seriously disrupt barge transportation, with the scrap trade between southern mills and Midwest scrapyards the most relevant issue. However, coil shipments north from Houston and southern mills will also be affected. How will it play out? Will there be a rush by southern mills ahead of the closure to secure feedstock? If so, will that spark a rally in busheling?

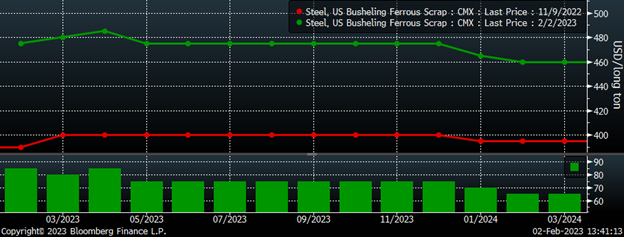

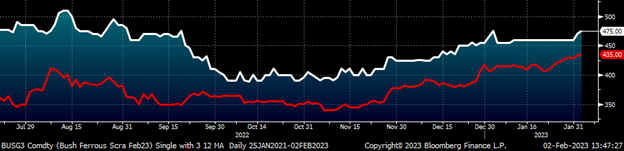

Since Nov. 9, busheling futures have rallied around $80, with the curve flat in this product as well. The January HRC future settled last week at $716, a month-on-month (MoM) gain of $63, but the January busheling future gained $59.45 MoM meaning only a piddly $4 increase to the metal spread. The February busheling future settled today at $475, indicating a $25 MoM gain.

A week from tomorrow brings February’s scrap settlements. Will we see the current $25 MoM increase indicated by the February future slip lower, or will it continue to percolate higher each day as it did in January? With the Federal Open Market Committee (FOMC) and European Central Bank (ECB) meetings behind us, we have scrap negotiations to look forward to next week. There is also a little football game next weekend, but I digress.

CME Busheling Futures Curve $/lt

Turkish scrap has also been in rally mode, along with a number of commodities of late. Since bottoming at $340 in November, Turkish scrap has gained almost 28%.

Rolling Front Month Busheling $/lt and Turkish Scrap Futures $/mt

The catalyst behind much of the rally in commodities has been China’s evolving government policy shifts, most notably reversing their COVID-zero policy. Many commodities, iron ore included, have been in a holding pattern for the past two weeks, likely due to China on holiday last week, following a multi-month rally. After peaking last March at $171/ton, iron ore fell 56% from peak to trough. Since bottoming on Halloween, iron ore has rallied as much as 73%.

Rolling 2nd Month SGX Iron Ore Future $/t

So what will happen in the weeks and months ahead for Midwest flat-rolled, ferrous raws and other commodities? Of course no one knows (see my Jan. 12 article), but tune in here every Thursday night for not only your steel market update, but also your steel futures market update. Keep an open mind about where HR prices may go in 2023. Buckle your chinstrap, and keep your voice broker on speed dial!

Disclaimer: The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Feldstein should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.

By David Feldstein, Rock Trading Advisors