Prices

February 9, 2023

CRU: The Impact of Earthquakes on Turkish Steel and Scrap Markets

Written by Thais Terzian

By CRU Senior Analyst Thais Terzian, Analyst Anton Perevezentsev, and Research Analyst Rosy Finlayson

On February 6-7, a series of devastating earthquakes struck several provinces in southeastern Turkey and northwestern Syria, leaving thousands dead and many injured. The quakes also resulted in a massive destruction to the infrastructure of both countries.

The first quake measured 7.8 in magnitude and the epicentre was in the Turkish province of Gaziantep, near the border with Syria. The Turkish government declared a three-month state of emergency in 10 provinces hit by the earthquakes.

Turkey is an important player in the steel market, being a large exporter of finished steel as well as the biggest importer of scrap globally. At the time of publication, the extent of the impact on Turkish steel mills in the earthquake-affected region is uncertain.

Turkey is an important steel producer

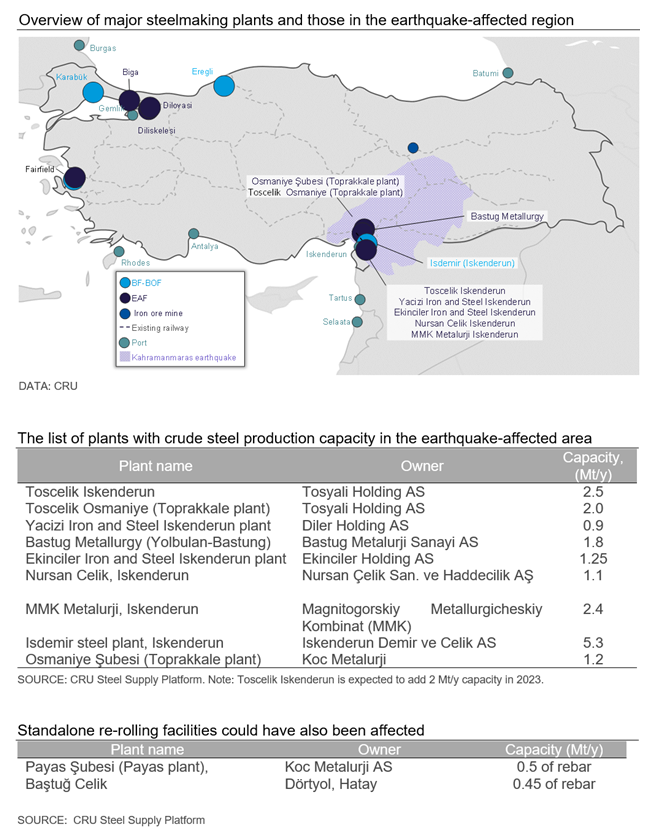

Turkey is a large steel producing country, with installed capacity of crude steel production of over 51 million metric tons per year (Mt/y), located in different regions of the country. In 2022, Turkish mills produced around 36 Mt of crude steel, representing 4% of total world ex. China production. Of this volume, around 72% came from EAF/IF-based steelmaking. This represents a large group of scrap-consuming facilities, which receive scrap supply from various sources, including maritime shipments from the US and the EU, among others.

The earthquakes spread across ten provinces in the southeast part of the country – Osmaniye, Kahramanmaraş, Gaziantep, Malatya, Diyarbakır, Kilis, Şanlıurfa, Adıyaman, Hatay, Adana. The Osmaniye province, particularly the Iskenderun area, is home to several steel mills. In this area, crude steel installed capacity totals around 18.5 Mt/y, or over 35% of the country’s total volume.

At the time of writing, the impacts of the earthquakes on the Turkish steel sector are uncertain. However, based on CRU’s assessment and market contacts, there has been no critical damage to the steel mills in the impacted area. But all operations have been suspended due to supply chain issues as well as the overall state of emergency in the earthquake-stricken provinces. At the same time, roads, natural gas supply as well as energy and logistics infrastructure are interrupted or damaged in the Iskenderun area and other districts.

On 7 February, fires were reported at Iskenderun’s containers port, which forced operations to stop. Meanwhile, no damage was reported to the bulks port. However, vessels are unable to discharge, and some were diverted to other ports.

Supply disruptions will likely hit local and export markets

More than 60% of the production capacity of the suspended steel mills are focused on long products production. As a result, longs supply is expected to fall dramatically until mills resume production. In case of prolonged disruptions, market balances of long products would tighten locally and globally, pushing prices upwards. At the same time, domestic demand in the impacted regions will likely plummet in the short term at least. However, we believe the impact on supply would be greater than the fall in domestic demand.

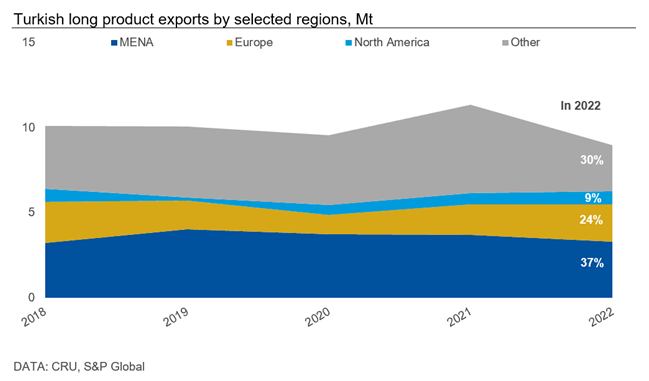

Turkey is also a significant long products exporter, with significant exposure to the European, Middle East and Northern African (MENA) markets. In 2022, longs exports totalled around 9 Mt, of which 37% and 24% of the total volume were shipped to the MENA region and European countries, respectively. The port of Iskenderun plays an important role in shipping finished material as it has direct access to the Mediterranean Sea compared to the Marmara and Karadeniz regions, making it a more convenient connection not only to European ports but also to African and Asian ports through the Suez Canal.

Should the disruption to the steel operations and logistics in Turkey continue for a prolonged period of time, the exposed markets will likely turn short on imports and will be forced to re-source from somewhere else. This creates an upside risk for longs prices to surge until the supply restores.

However, if exports infrastructure and logistics resume activity alongside steel mills in Iskenderun, more supply will be available for exports, given reduced domestic demand. Prices would be under downward pressure as a result of the oversupply. Meanwhile, in the longer term, local longs demand is expected to rise on the back of reconstruction works in the damaged areas.

Scrap imports stall

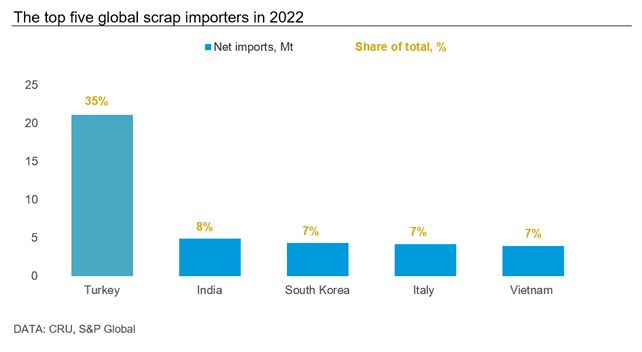

Turkey is the world’s largest scrap importer, given its higher EAF-based production share and insufficient domestic scrap supply. In 2022, Turkish scrap imports totalled around 21 Mt and represented 35% of total global imports and 72% of the domestic scrap consumption. To put these figures into perspective, scrap imports from India, the second largest importer, totalled only 5 Mt in 2022.

Despite no direct impact yet reported, the scrap trade has been paralysed in the Iskenderun region and the rest of the country.

Turkey also imports pig iron and HBI, but at much lower scale than scrap. In 2022, the country’s pig iron imports totalled around 1.5 Mt and HBI 0.6 Mt. Nevertheless, Turkey has become an important outlet for Russian ore-based metallics exports since the war in Ukraine started. Therefore, any disruption in Turkish demand would leave Russian exporters with fewer active buyers and could put pressure on prices.

Short-term impact will depend on the scale of damage

There is currently a great deal of uncertainty regarding the impact on global steel and metallics markets caused by disruptions and blockage in Turkey. On one side, we might expect finished steel exports from Turkey to be lower in the short term, which could give support to prices, particularly of rebar. On the other side, if infrastructure is permanently damaged and/or steel mills production remains limited, scrap imports demand will drop, loosening the global scrap supply balance and putting downward pressure on global export and domestic scrap prices.

In a more medium-term view, domestic steel demand in Turkey, particularly of long products, can be higher than our published forecast on the back of reconstruction works that will be required in the impacted regions.

A more accurate assessment of the impacts on markets and prices depends on the actual scale of the damages and the country’s ability to restore the regional infrastructure and resume economic activity.

CRU is closely monitoring the situation and we will provide more updates as this story progresses.

Restricting Exports Could Fit with the Green Deal

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com