Mexico

March 19, 2023

Final Thoughts

Written by David Schollaert

Price increases have dominated the headlines thus far in 2023. Since Jan. 1, we’ve had one blitz of tag hikes after another. In the eleven weeks since the start of the year, there’s only been a single week in which not a single mill announced a price increase.

It sometimes felt like one mill had to outdo the next. For my poker players out there, it’s almost as though all the mills are just reraising one after another and no one at the table is making a call.

“I see your $50 per ton increase and raise you $100 per ton.”

“I see your $100 per ton increase and raise you $150 per ton.”

Now, there are rules to how many times you can reraise during a poker match, usually 3-4 times. But in no-limit and pot-limit games, unlimited raises are allowed.

Steel Market Update’s hot-rolled coil (HRC) price now stands at $1,115 per ton on average, up $40 per ton from last week. (We’ll update our prices again on Tuesday.) We’ve seen HRC tags increase by $490 per ton on average since Thanksgiving, when prices first turned upward. They’ve surged by $335 per ton over the past six weeks.

And what began as a surprise to many now seems commonplace. Regardless, all eyes are glued on the “game” to see who reraises next.

But none of this is news to you. I get that.

The overarching theme since prices began their present rally was that higher tags weren’t due to a single driver, but rather a myriad of reasons that taken together had resulted in a temporary supply squeeze. A few big factors were these: better-than-expected demand coupled with new capacity being slow to ramp up. Also, limited output at Altos Hornos de México (AHMSA) resulted in a supply deficit in a region that had been expected to see a glut. Such dynamics have driven prices to their highest level in 39 weeks.

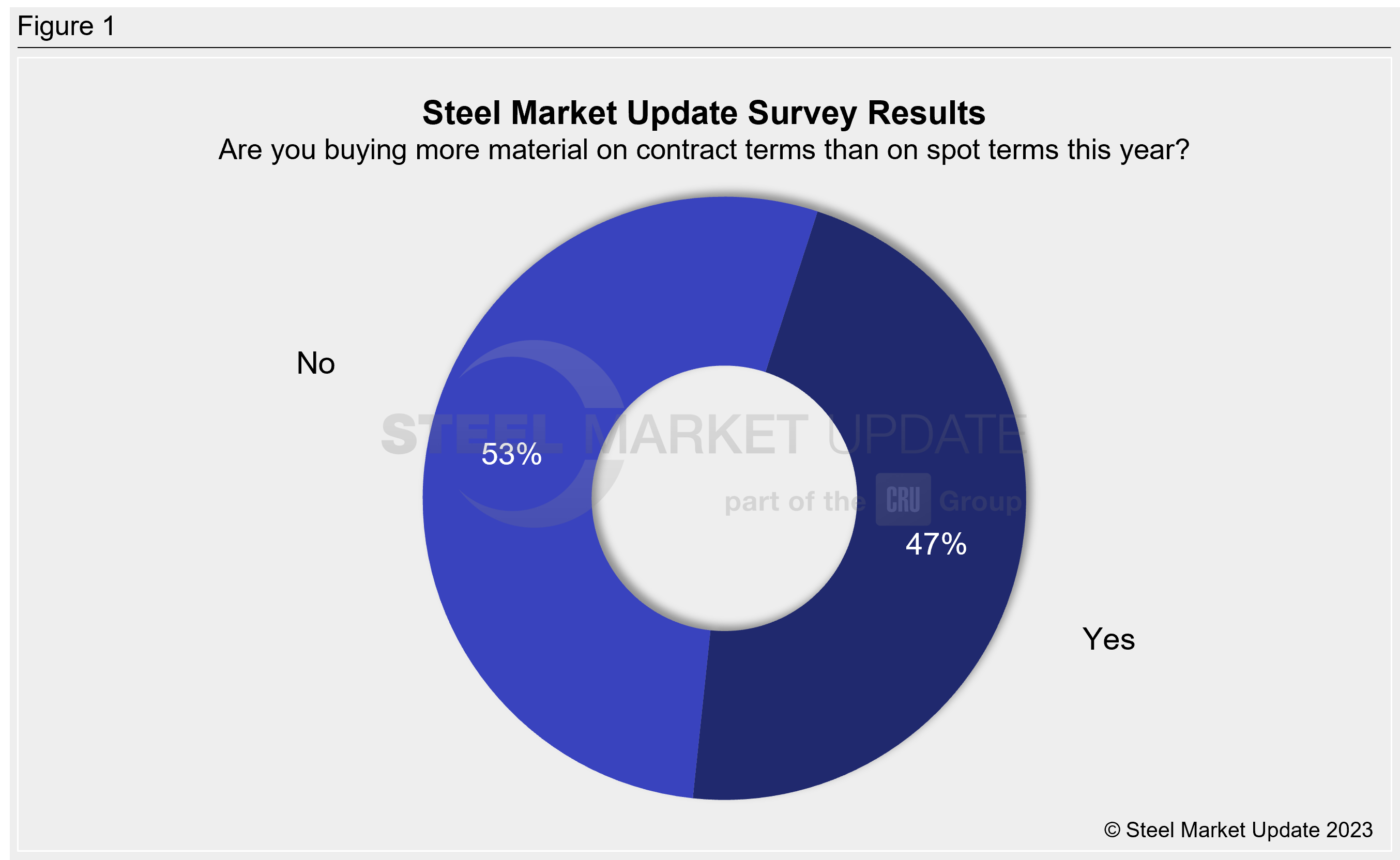

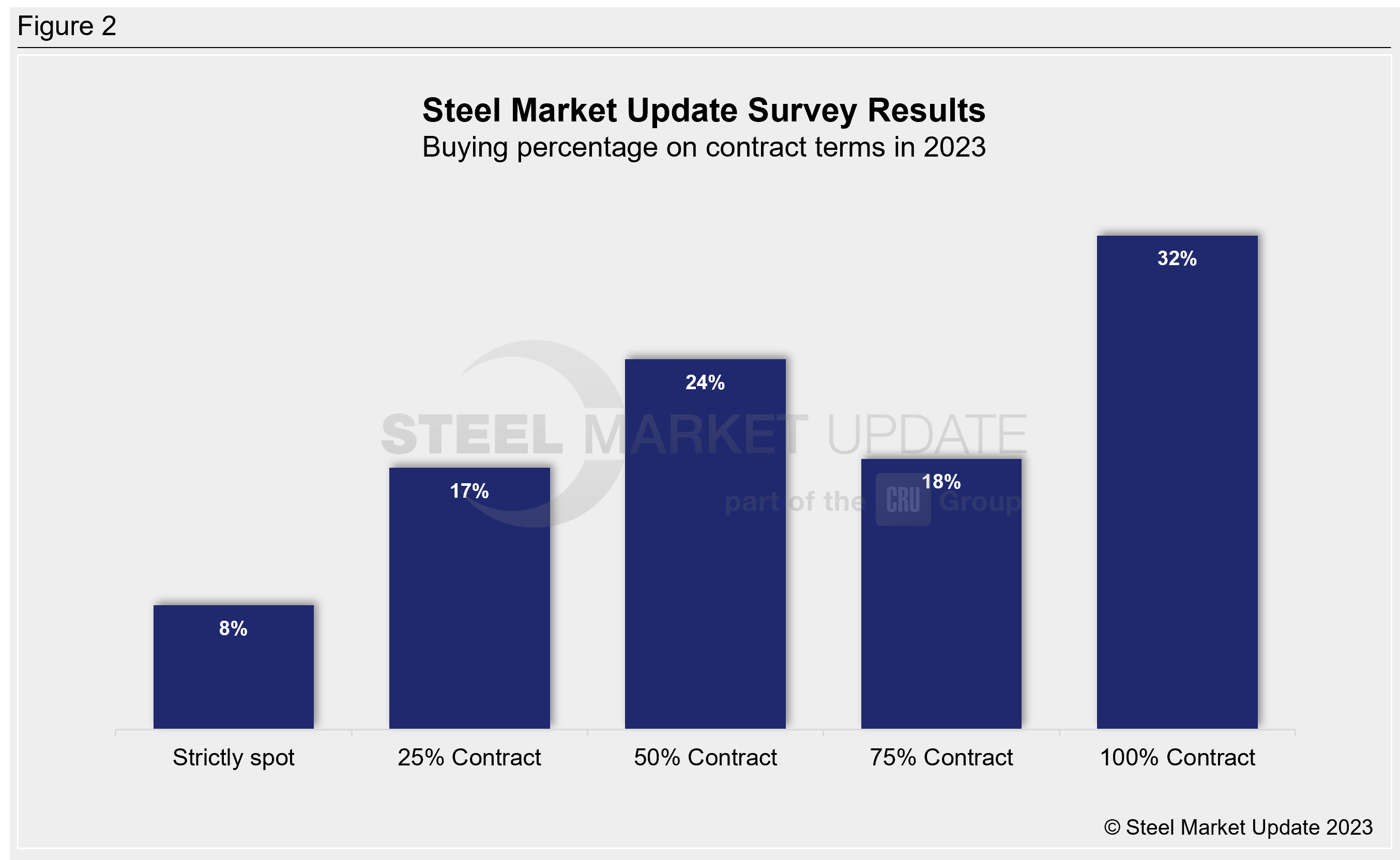

We polled our survey respondents – mainly manufacturers and service centers – asking them whether they are buying more material on spot terms than on contract terms this year, and what their contract/spot buying mix was for 2023.

We saw good response rates to these two questions. Here are the results:

Forty-seven percent of respondents (Figure 1) said that they increased their contract buying in 2023. Fifty-three percent said their sourcing approach had not changed.

The second question (Figure 2) indicates that nearly three-quarters of respondents have at least 50% of their requirements on contract terms. Of those, almost half of them have secured their entire order book on contract.

If the scales remain heavily tilted toward contract buying, the supply squeeze could be more widespread in the spot market. Unforeseen production disruptions, even small ones, could result in sharp price increases. On the flip side, if demand were to falter or supplies increase, prices could drop quickly.

SMU Events

We are less than a month away from our LIVE Steel 101: An Introduction to Steelmaking and Market Fundamentals training course. It will in Cleveland on April 11-12. The workshop will include a tour of Cleveland-Cliffs integrated steel mill in the heart of downtown Cleveland. Click here to register.

Also, don’t forget to register for Steel Summit this Aug. 21-23, our flagship event and the largest flat-rolled steel conference in North America. You can learn more and register here.

Keynote speakers this year will include Cleveland-Cliffs chairman, president, and CEO Lourenco Goncalves; Barry Zekelman, executive chairman and CEO of Zekelman Industries; ITR economics president Alan Beaulieu; and Gene Marks, president of The Marks Group PC. We’ll be announcing additional speakers in the weeks ahead.

By David Schollaert, david@steelmarketupdate.com