Prices

July 6, 2023

Futures: Will Holding Pattern in HR Tags Stick Out Summer Lull?

Written by Jack Marshall

A short week with the July 4th Holiday kind of sums up recent HR futures activity. Subdued spot activity and not much change from the previous weeks’ indexes leaves the market time to roll exposures.

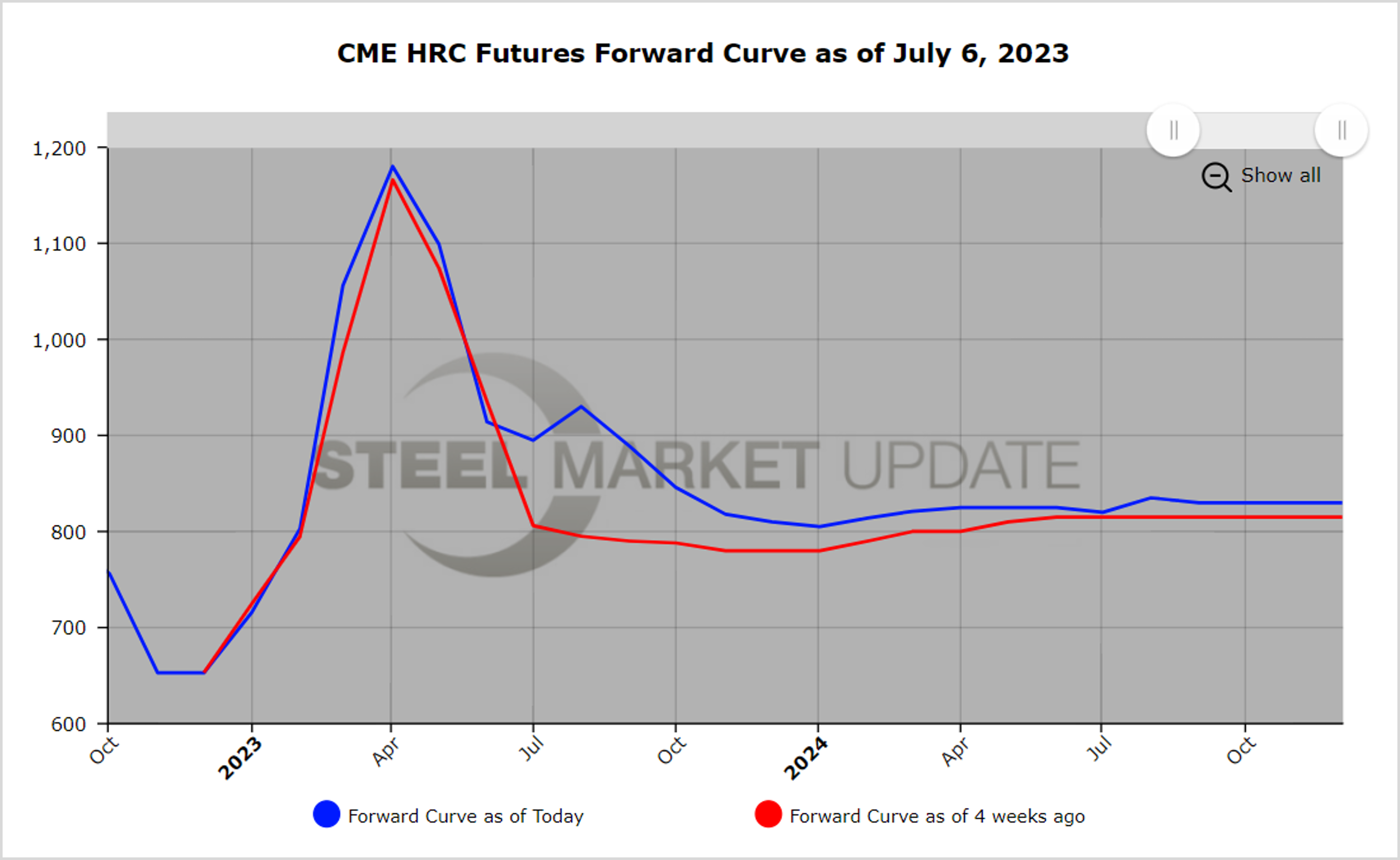

The recent price increases appear to have given spot prices a pause. Heading into the cyclical summer soft spot, mills are trying to hold the line on prices. Some of the indexes reflect some price increases. (Spot Index $880/ST roughly.) The jury is still out as to whether there is enough demand to move prices higher on the back of soft manufacturing data. But given fairly tight inventory control at the service center level, any unexpected outages could be supportive of the current push to move the spot index prices higher, especially for certain regions and grades. The latest front month settlement values Jul’23 HR at $895/ST, up slightly from the latest average of HR indexes. However, lower global HR prices point to strong import competition and an increase in selling interest from importers.

The current futures curve settles for Q3’23 HR average price ($905/ST) reflect a $65/ST bump higher in the average settlement price since the June 7 settles. The rest of the futures curve is basically flat, reflecting only a $15 lower average price as compared to the Q3’23 average price. It is too early to tell what futures activity for July will be following a fairly active June, which saw almost 33,000 contracts trade and open interest peak at roughly 28,500 contracts, a slight decline from May.

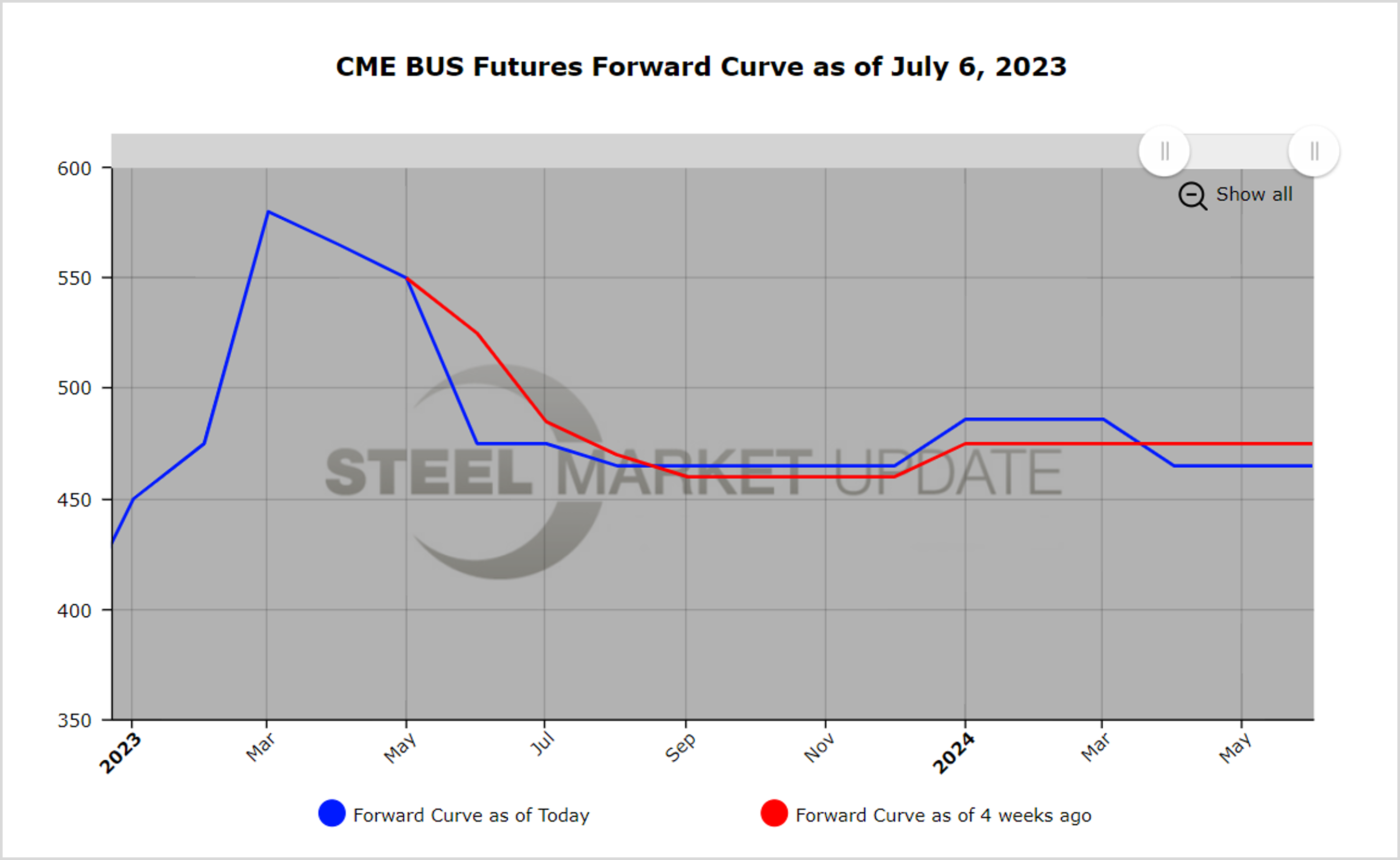

Early futures indications for July suggest another small price decline as latest offers for Jul’23 BUS reach $470/GT, which suggests almost a $25/GT drop. Interestingly, the front of the curve has dropped enough to flatten out the curve for the next 12 months. The prices for the back end of the futures curve are barely changed as settles averaged out to roughly $465/GT. The shape of the curve represents an opportunity as the metallics prices rarely stay flat for long. The current metal margin reflects an $80/ton backwardation from Q3’23 to Q4’23 dropping from roughly $440 to $360/ton. Even with the anticipated decline, that still represents a healthy margin when compared to the historic average.

By Jack Marshall of Crunch Risk LLC