Analysis

July 23, 2023

Final Thoughts

Written by Michael Cowden

I’ll dive into the latest sheet market trends in a moment. But first some big news: We’re less than a month away from the start of SMU’s Steel Summit in Atlanta!

Nearly 1,100 people were registered to attend when I last checked on Friday. The pace of registrations has picked up, so we’ll probably be over that figure by the time many of you are reading this on Monday.

If you haven’t made plans to attend, what are you waiting for? Register here and catch up with 1,100+ of your closest friends in steel. Nearly 1,300 people attended last year, let’s break that record this year!

For those new to the SMU community, Steel Summit runs from Aug. 21-23 at the Georgia International Convention Center (GICC). It’s connected to Atlanta Hartsfield-Jackson airport by a free tram – so the convenience is hard to beat.

Hotels on the GICC campus are sold out. Suggestions for nearby hotels here.

Now, back to the steel market…

Steel Market Survey

Sheet prices have slipped. Was that a temporary blip before mills roll out another hike or the resumption of the downward trend the market was on for most of Q2?

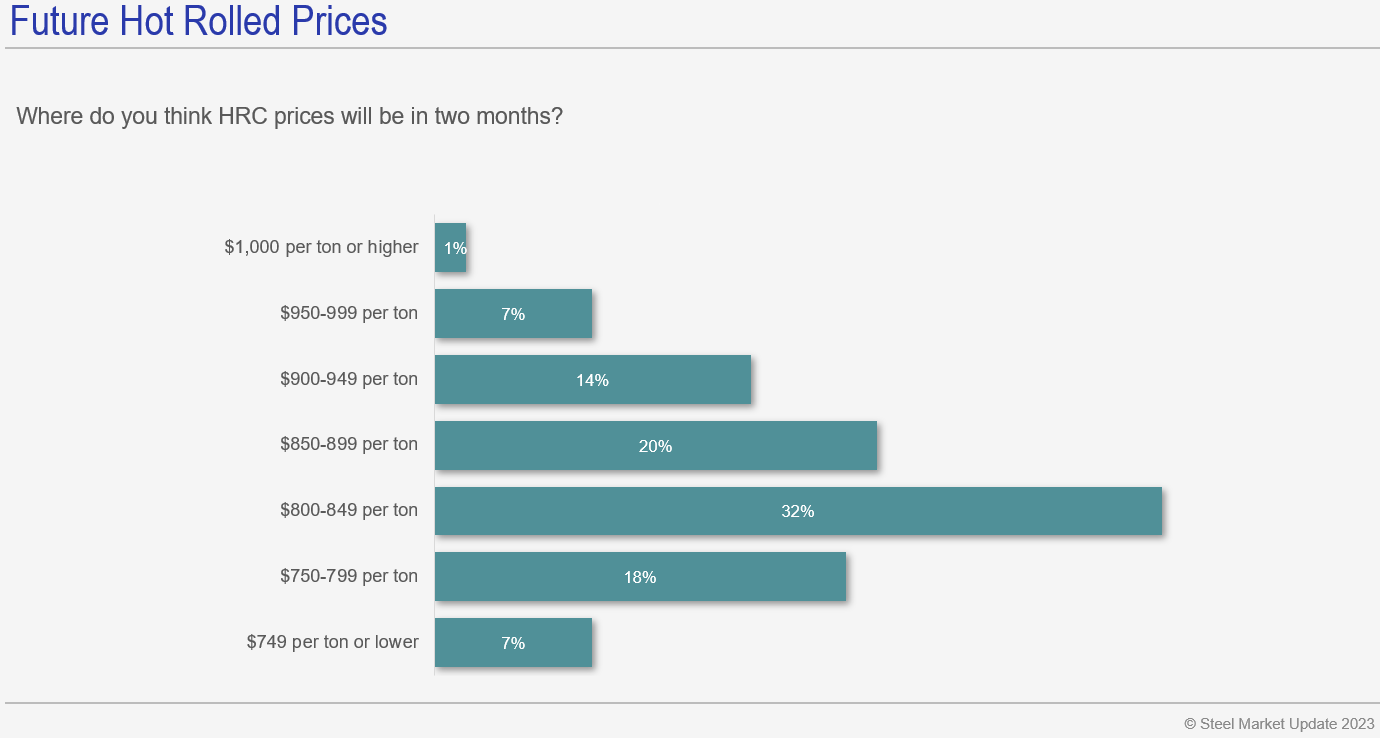

I turned to our latest steel market survey for some clues. Let’s start with where people think hot-rolled coil prices will be in two months:

Nearly one-third of respondents said HRC prices would be $800-849 per ton ($40-$42.45 per cwt) two months from now. That’s lower than where SMU’s HRC price is now but hardly falling off a cliff. But the idea that prices will hold above $900 per ton is no longer a consensus among the steel buyers we surveyed.

Recall mills in June announced $50-per-ton price hikes in mid-June and target HRC prices of $900-950 per ton, depending on the mill. In late June, nearly 40% of survey respondents thought HRC prices would climb above $900 per ton. Now only 20% think that threshold will be crossed.

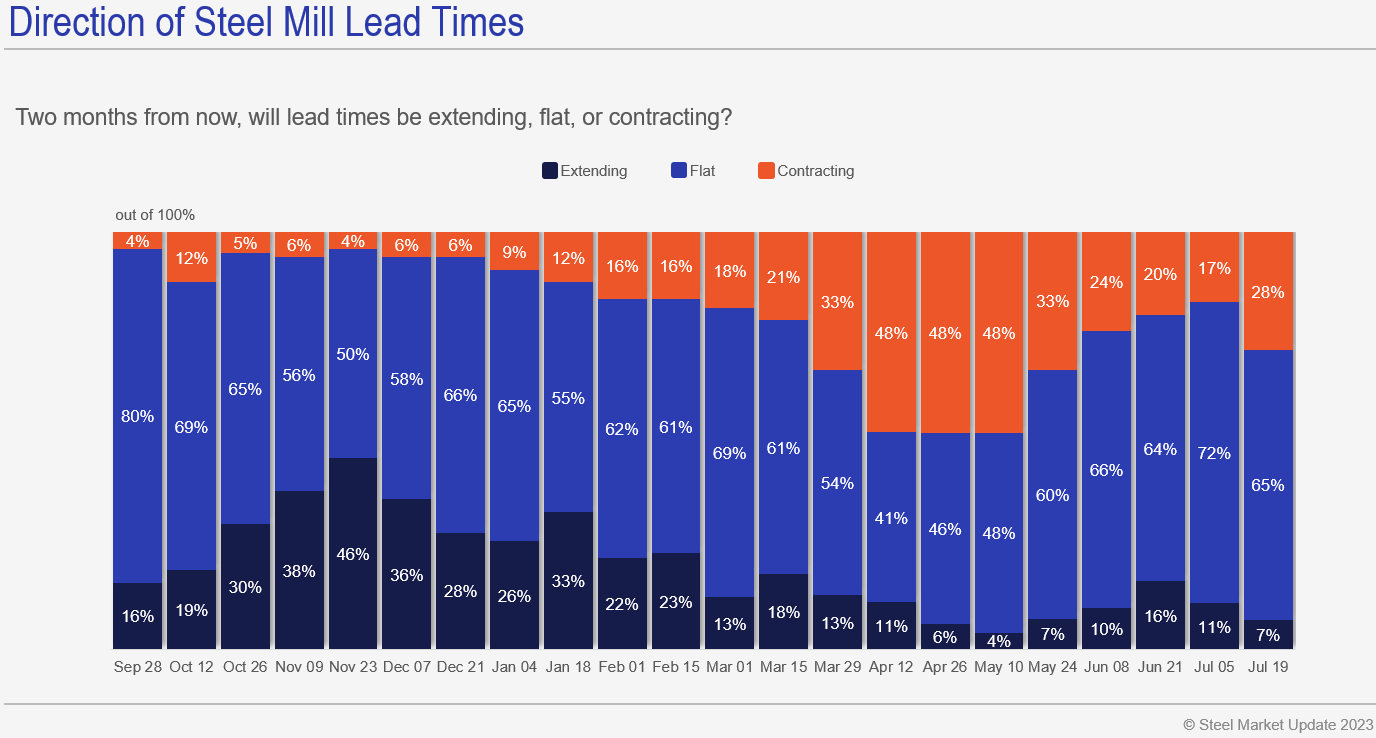

We also asked where lead times would be in two months. There, too, we’ve seen a shift in opinion:

Since late May, there had been a steady increase in the number of respondents predicting that lead times would increase or at least hold steady. More recently, we’ve seen an uptick in the number of people who predict that lead times will be lower two months from now.

Are we seeing evidence yet in our surveys of a drop in demand? Not really.

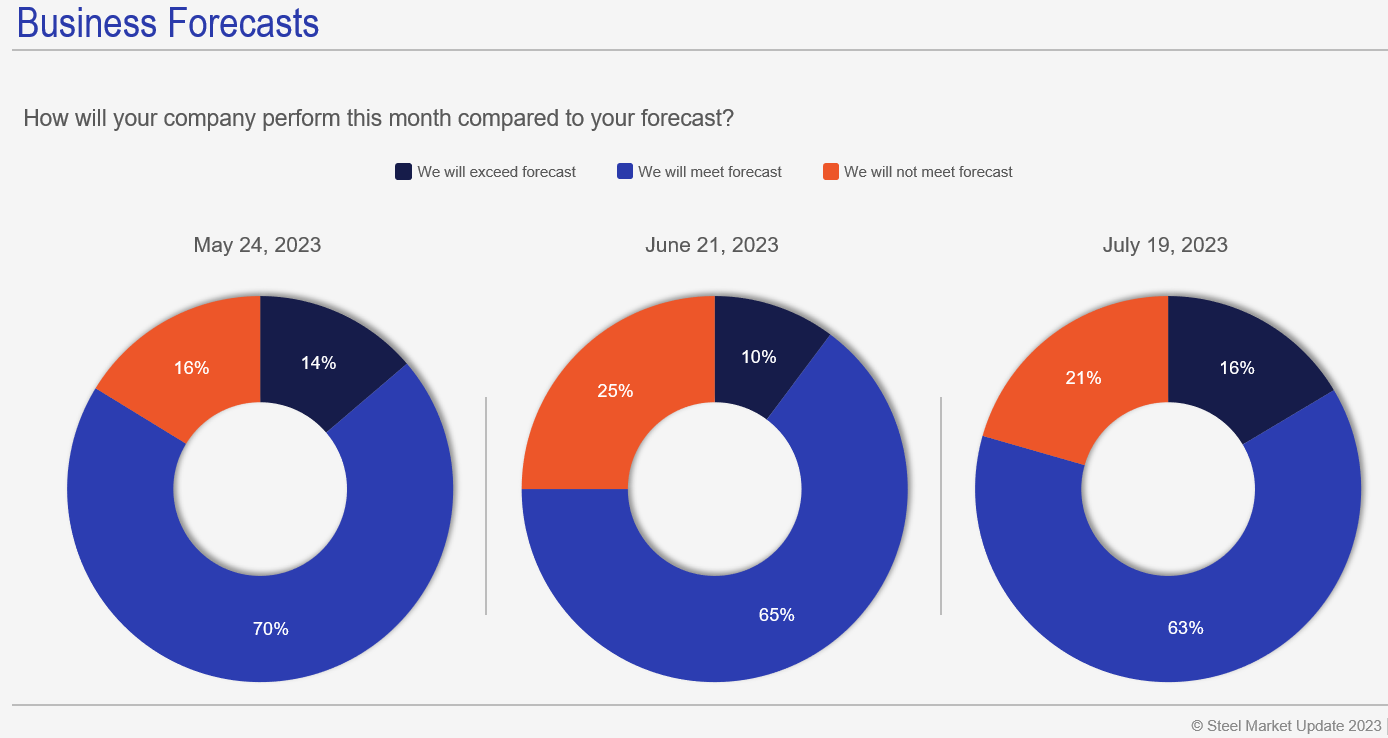

This is one of my favorite questions, whether people are meeting forecast:

The numbers have been stable since May. Most people (60-70%) have since then reported that they think they will meet forecast. The number of people who think they will exceed forecast (~15-25%) continues to slightly exceed the number who think they will miss forecast (~10-15%).

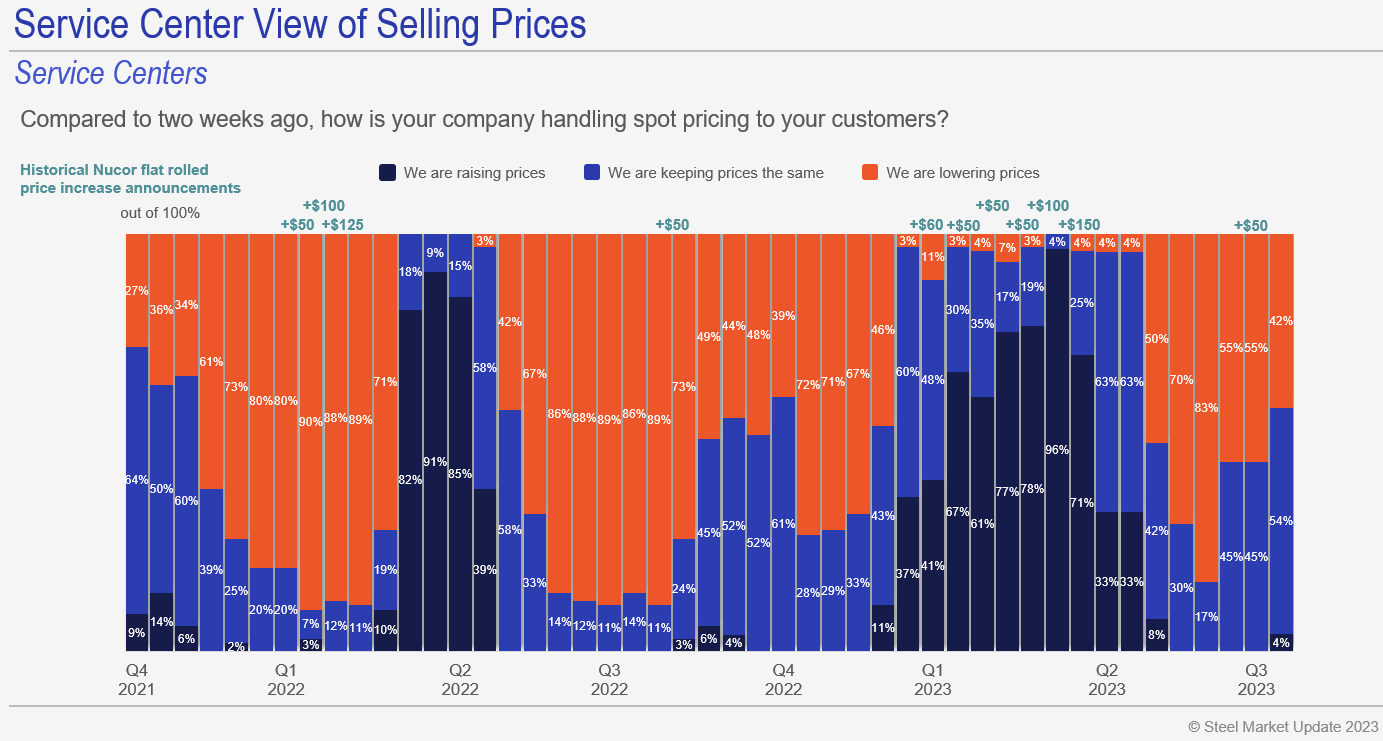

Meanwhile, nearly 60% of service centers respondents report that they are holding prices steady or increasing them:

That might not seem like much. But it’s a big change compared to late May when nearly 85% said they were cutting prices. In other words, the June price hikes did have an impact – even if it was mostly stabilizing prices downstream rather than increasing them.

What gives? Expectations around prices and lead times have come down even though most people continue to meet forecast. Why the gloom?

Let’s start with the obvious macroeconomic one. We’re in a world of higher interest rates and tighter lending standards. Various economists and armchair experts have been predicting a recession is around the corner for at least a year. Slowing down a big ship like the US economy takes time. But eventually, higher interest rates will do that, even if exactly when might be hard to call.

I know some of you are concerned about the outlook for automotive for the same reasons. You’ve noted an increase in less-profitable fleet sales as well as the increased potential for a strike in the fall given contentious talks between the UAW and the “Big Three” automakers – Ford, General Motors, and Stellantis.

But I continue to hear from many of you that skilled workers are still hard to find and keep. How is it that we’re seeing so much worry about the economy in general but still meeting forecast at our companies while having trouble hiring the people we need to make products to meet that demand?

Let me know if you have any answers. I’d be interested in knowing your thoughts.

SMU Community Chat

Barry Zekelman, executive chairman and CEO of Zekelman Industries – the largest independent steel pipe and tube product in North America – will be joining us for an SMU Community Chat webinar on Wednesday, July 26 at 11 am ET.

Zekelman is a student of the steel industry and one of the largest sheet buyers in North America – so what he says matters. We’ll talk about everything from steel and the economy to trade issues and his trial-by-fire entry into the industry. Join us, register here!

By Michael Cowden, michael@steelmarketupdate.com