Analysis

December 5, 2023

Final thoughts

Written by Michael Cowden

I want to thank the Heating, Air-conditioning & Refrigeration Distributors International (HARDI) for the opportunity to speak at their annual conference in Phoenix.

I enjoyed the proceedings and participating in a panel for HARDI’s sheet metal/air handling council.

I can’t recap all that we discussed in a few hundred words. But I’d like to share with you some of my thoughts on a couple of the questions we covered.

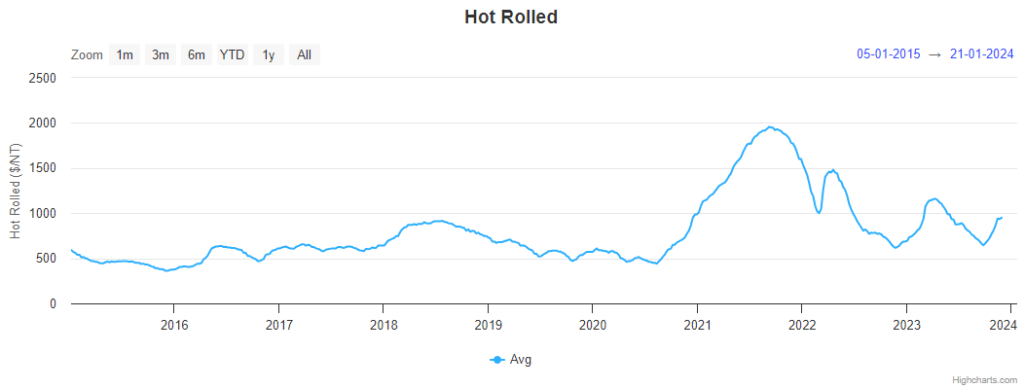

Why have steel sheet prices been so volatile since the pandemic?

A quick visual of just how volatile: This snip is from SMU’s interactive pricing tool.

Another way to look at it: Annual average HRC prices for every year (and 2023 year to date) back to 2015:

- 2023: $886 per ton

- 2022: $1,015 per ton

- 2021: $1,612 per ton

- 2020: $587 per ton

- 2019: $598 per ton

- 2018: $829 per ton

- 2017: $616 per ton

- 2016: $526 per ton

- 2015: $452 per ton

The volatility over the last three years reflects some truly jarring world events. In 2020, the pandemic initially hammered demand, and prices plunged. Then, in late 2021, we saw a snapback in demand, and prices soared. In 2022, supply overtook demand, and prices fell. But, the outbreak of war in Ukraine and a panic over raw materials supply caused a historic price spike.

In early 2023, we saw another huge price spike. It was arguably a combination of overly bearish sentiment late in Q4’22, low imports, and AHMSA unexpectedly going out around Christmas. Certain buyers (and mills) realized what had happened and started buying up everything that they could. Also, some new capacity struggled to ramp up. The result was a shortage instead of the glut that had been anticipated. And by February, US mills were raising prices almost weekly – and by as much as $100 per ton.

We saw something similar happen this fall with the UAW strike. People expected prices to plunge and then spike after the strike was over. So when prices got low in mid/late Sept, savvy buyers figured the upside risk was greater than the downside risk. They pulled forward orders. And then there was a flurry of fall maintenance outages. The result: Lead times are now into January or February. And if you want spot tons, they won’t come cheap.

What is the new floor and peak for sheet?

I’m going to set aside 2020-21 because they were so distorted by the pandemic. In 2022, HRC bottomed at $615 per ton on average. And we bottomed at $645 per on average in late September of this year. So is $600-650 per ton our new bottom?

True, prices fell into the $400s per ton in 2015. But there is one big difference between now and then. We have seen more consolidation among integrated mills. And there are fewer of them. A lot of that $400s per ton was driven by competing integrated mills running flat out. Basically, keeping costs low by maintaining high volumes. That makes sense, but it can be self-defeating if everyone is doing it.

What about new capacity now? Yes, there is a lot of it, and more to come, as our chart here shows. But almost all of it is EAF-based. Let’s use the analogy that integrated mills are like a light switch – they can only be on or off. EAFs are more like a dimmer. They can be turned up or down gradually.

So, yes, more supply and steady demand should lead to lower prices. But perhaps not as low as we’ve seen in the past if EAFs dial back supply when demand slips.

I know some of you think that sheet is fundamentally more sentiment-based than, say, plate. Buyers tend to leave the market and re-enter it all at once. That leads to wild gyrations in prices. And that behavior is unlikely to change.

I’m going to try to square those views this way: Yes, sheet prices might remain volatile. But could they be volatile in a narrower bandwidth over the next three years than what we’ve seen in the last three?

Tampa Steel Conference

I’m tossing out ideas here. Want to get an expert analysis of where the steel market is headed in 2024 and beyond?

Register for the Tampa Steel Conference on Jan. 28-30! Leading steel industry analysts will present their steel price forecasts. They’ll be joined by mill CEOs as well as economists and experts on key end markets like automotive, construction, and energy.

You’ll come away with your finger on the pulse of the market, and with ideas on where to take your business in the years ahead.