Analysis

January 22, 2024

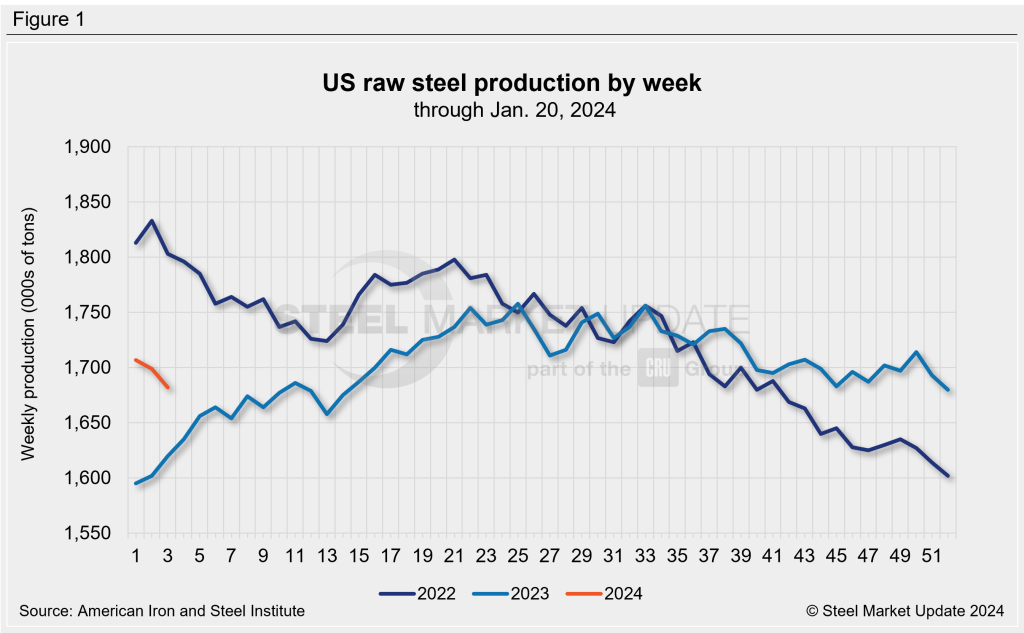

Raw steel output moves lower again: AISI

Written by David Schollaert

Domestic production of raw steel edged lower for a second straight week, according to the most recent data from the American Iron and Steel Institute (AISI).

Steel output in the US totaled an estimated 1,682,000 short tons (st) in the week ended Jan. 20. That’s down 1% from the previous week and from the same week last year when production stood at 1,697,000 st.

The mill capability utilization rate was 75.7% during the third week of 2024, down from 76.5% a week earlier and down slightly from 75.9% a year ago.

Production by region is shown below, with the week-over-week changes shown in parentheses:

- Northeast – 132,000 st (up 9,000 st)

- Great Lakes – 543,000 st (down 10,000 st)

- Midwest – 188,000 st (down 5,000 st)

- South – 754,000 st (down 15,000 st)

- West – 65,000 st (up 4,000 st)

Editor’s note: The raw steel production tonnages provided in this report are estimated. The figures are compiled from weekly production data provided by approximately 50% of the domestic production capacity combined with the most recent monthly production data for the remainder. Therefore, this report should be used primarily to assess production trends. The AISI production report “AIS 7”, published monthly and available by subscription, provides a more detailed summary of steel production based on data supplied by companies representing 75% of U.S. production capacity.