Analysis

March 5, 2024

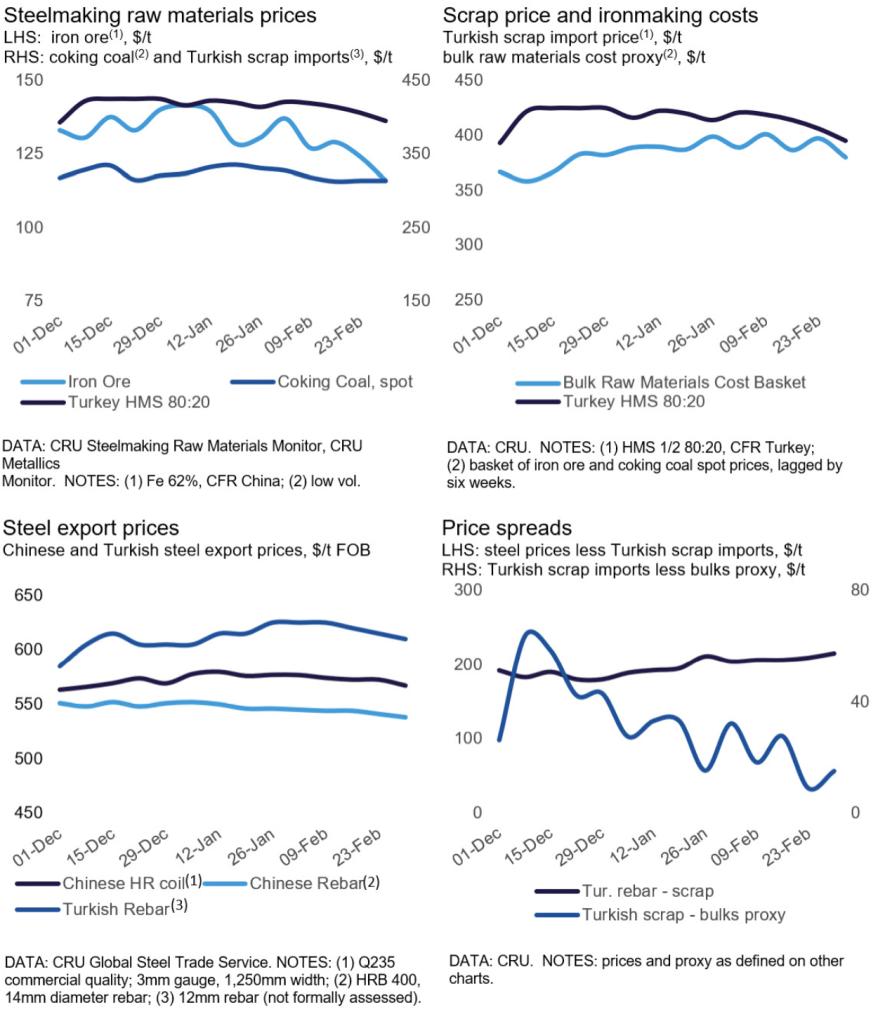

CRU: Turkish scrap import prices decline as tags come down in main supplier markets

Written by Rosy Finlayson

Turkish scrap import prices consistently declined over the past month due to persistently weak domestic demand and lower prices in main supplier markets in recent weeks. CRU’s assessment for HMS1/2 80:20 is $395 per metric ton (mt) CFR, down by $11/mt week over week (w/w) and $26/mt month over month (m/m).

Turkish scrap import prices fell last week partly due to prices in Turkey’s main supplier markets of the US and Europe decreasing. At the same time, in the domestic market, mills continued to hold off scrap purchases due to lackluster finished steel demand. Turkish rebar and hot-rolled (HR) coil prices fell again last week by $5/mt w/w to $610/mt FOB and $690/mt FOB, respectively.

Demand has weakened in the domestic Turkish scrap and steel market ahead of the start of Ramadan on March 11, and the local elections at the end of the month. Scrap demand generally slows seasonally around Ramadan. Market participants are also taking a wait-and-see approach due to uncertainty related to the local elections. Although the local elections are smaller, there is still a risk that President Erdogan could introduce stimulus measures, as he did ahead of the national elections last year. This would have large implications for the country because it will likely frighten investors, who have recently re-entered the market since the Turkish Central Bank’s shift back to mainstream monetary and fiscal policy.

This article was first published by CRU. Learn more about CRU’s services at www.crugroup.com/analysis.