Market Data

May 9, 2024

SMU survey: HR, CR, and plate buyers find mills more flexible on price

Written by Ethan Bernard

Steel buyers said mills were more willing to discuss lower prices on spot orders for hot-rolled sheet, cold-rolled sheet, and plate.

Buyers of galvanized and Galvalume sheet, on the other hand, found mills less flexible on spot prices this week compared to two weeks ago.

The overall negotiation rate for all products SMU surveys remained roughly flat, according to our most recent survey data.

Every other week, SMU polls steel buyers asking if domestic mills are willing to negotiate lower spot pricing on new orders.

This week the rate was flat, with 75% of participants surveyed by SMU reporting mills were willing to negotiate prices on new spot orders. We have to go back to September to find two survey weeks where the rate was steady. In mid- and late September, we logged two consecutive surveys of 90% (Figure 1).

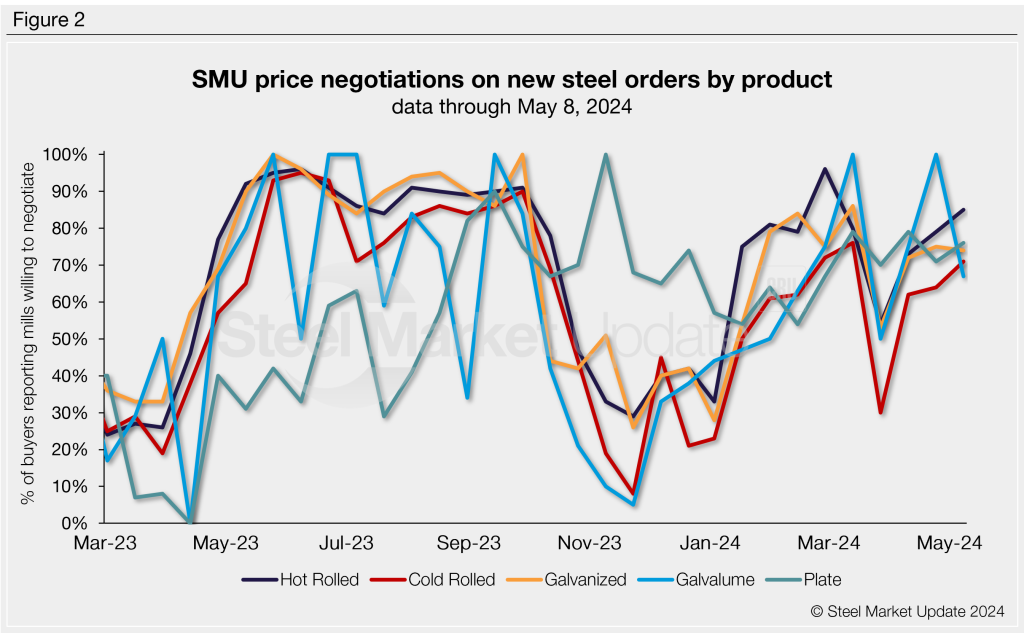

Figure 2 below shows negotiation rates by product. The rates for hot-rolled coil rose six percentage points to 85% this week, for cold rolled increased seven percentage points to 71%, and for plate jumped five percentage points to 76%.

At the same time, the rate for galvanized sheet slipped one percentage point to 74% and for Galvalume it fell 33 percentage points to 67% from the last market check.

Here’s what some survey respondents had to say on negotation rates:

“Depends on the mill (for hot rolled).”

“Depending on tonnage (for cold rolled).”

“Most mills still delivering in mid-June (on galvanized). Some out as far as August.”

“Plenty of HR capacity.”

“I feel they are (willing to negotiate on galvanized) and had intended to send out an RFQ later this week. But based on lead times and the direction the market is headed, I may be delaying that another week to verify how much they will negotiate.”

“Dependent on location and mill, they are willing to listen to offers (on plate).”

Note: SMU surveys active steel buyers every two weeks to gauge their steel suppliers’ willingness to negotiate pricing. The results reflect current steel demand and changing spot pricing trends. SMU provides our members with a number of ways to interact with current and historical data. To see an interactive history of our steel mill negotiations data, visit our website.