Analysis

June 1, 2025

Final Thoughts

Written by David Schollaert

Well, I guess there’s nothing quite like ending the week with a bang! What most thought would be a victory lap for U.S. Steel and its “planned partnership” with Nippon Steel turned into a breaking news extravaganza.

Trump flexed his muscles, saying he would double Section 232 tariffs on imported steel from 25% to 50%. Maybe it was response to the US Court of International Trade (CIT) ruling on Wednesday that found that the president could not use the International Emergency Economic Powers Act (IEEPA) to impose tariffs?

With higher tariff rates on steel and aluminum set to go into effect on Wednesday, June 4, a new round of chaos across the supply chain is likely in store. Expect a significant impact on manufacturers and metal fabricators.

But even before the latest round of Trump-tariff whiplash on Friday evening, there was a lot of interesting data coming out of SMU’s steel-market survey.

Yes, more uncertainty, mayhem, and panic buying might come this week because of higher tariffs on steel and aluminum. But our data indicates that it will come against the backdrop of a much softer market than what we saw during a previous Section 232 buying frenzy in Q1.

Just a few examples: Mill lead times are the shortest they’ve been since 2022. Sentiment remains cautious. And at least through last week, mills were cutting deals and lowering prices as they sought to entice new orders.

Here are some of our latest results as well as a sampling of comments from survey respondents.

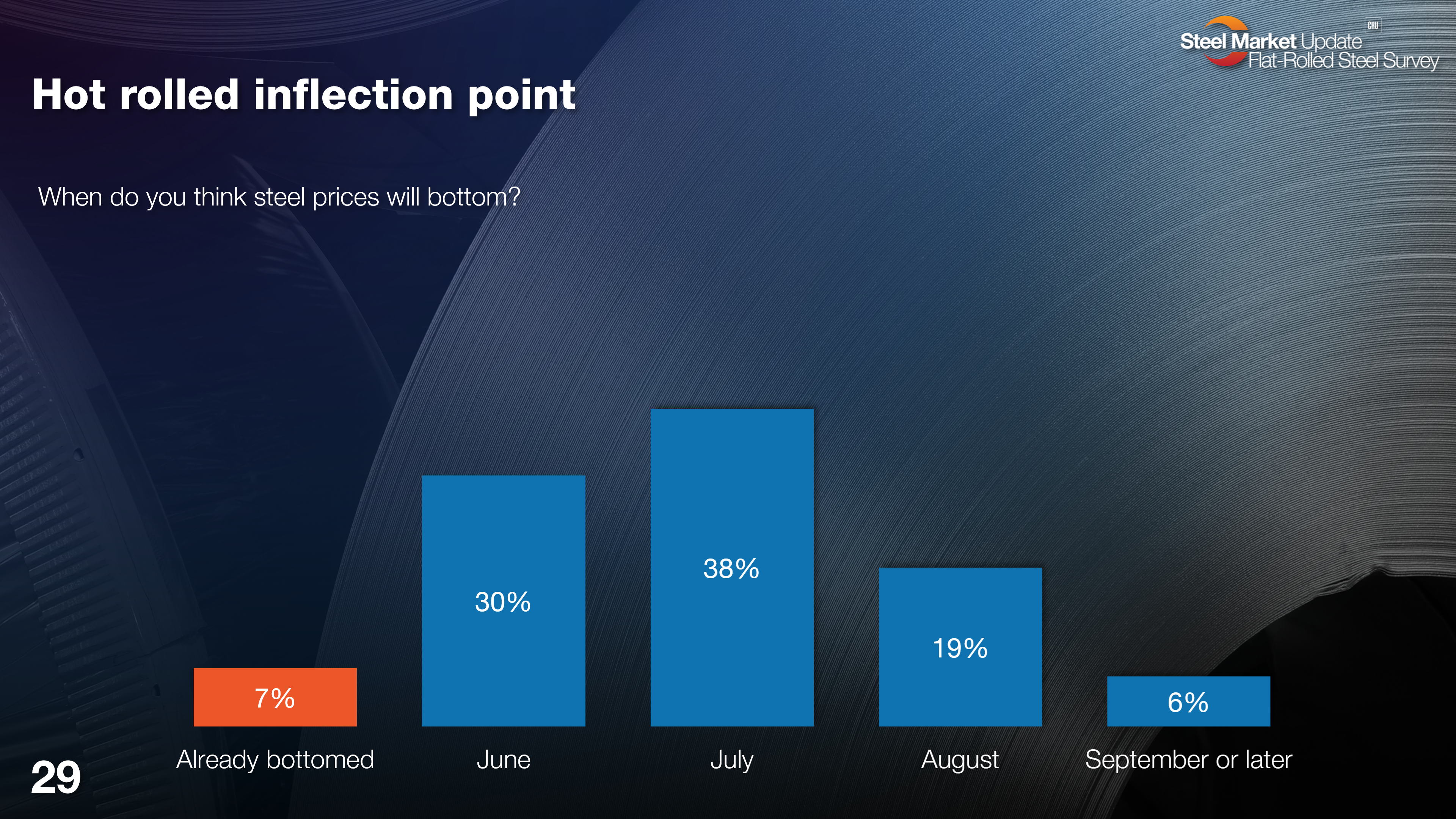

Survey says it’s a downhill ride this summer

In late March, all things pointed to a market on the rise. Many expected prices would peak in June.

That sentiment turned sour quickly, and now the wisdom of the crowd now says that prices won’t bottom until July or later. A small minority (6%) of survey respondents think that bottom might not form until as late as September. (Editor’s note: You can click on any of the images below to expand them.)

Here is what some of them had to say:

“Lower scrap prices and improved capacity utilization will support lower selling prices.”

“Backside of auto slowdown period and scrap bouncing along the bottom for two months will provide mills with some justification to push prices northward.”

“Surplus in supply, sluggish demand, slow construction, and heavy inventories. Could see a snap back to a higher market if supply is taken out of the market.”

“Demand just is not here, and a manufacturing rebuild will take too long.”

“Some service centers seem to be driving pricing down despite cost inputs going up, very counterintuitive, but I don’t think they can continue for much longer.”

“We are thinking that pricing will continue to erode until we’re into September lead times. Just too weak of demand.”

“Seasonal slowdown and administrative policies are still uncertain.”

“It’s currently a slow price decline we’re seeing, and I think it may take a good few months for prices to bottom out. Other than clarity on tariffs, especially tariff relief, it’s hard to see what’s going to cause prices to increase very much.”

“Too much capacity and not enough demand.”

“Economic slowdown due to tariffs, coupled with increases in North American capacity.”

“Steel mills will try to gain more orders by lowering prices.”

“The effects of tariffs are still to be seen on the general industry demand.”

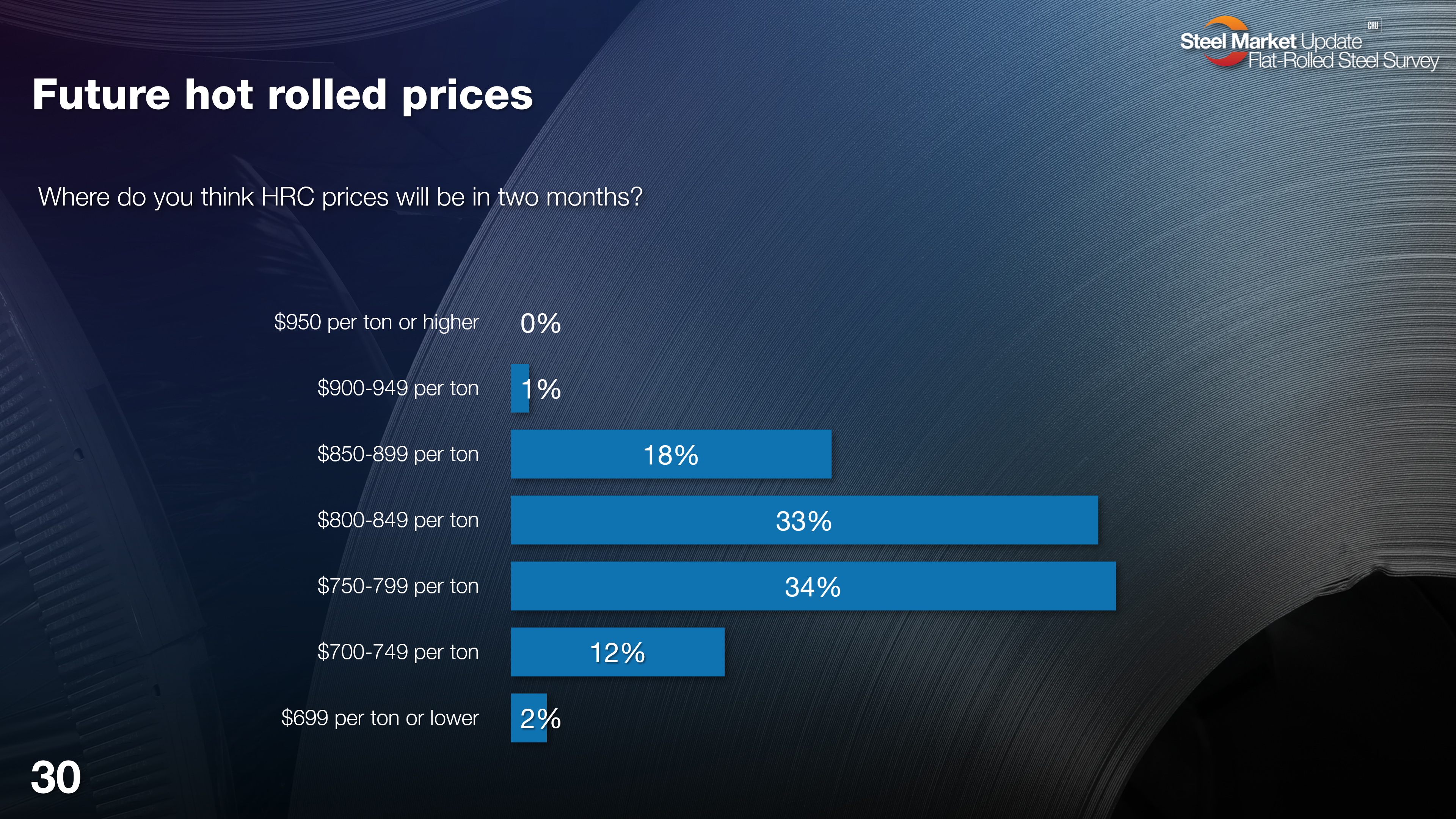

How low can it go?

Another reflection of that general bearishness: Nearly half of survey respondents think the hot-rolled (HR) coil prices will be below $800 per short ton (st) in August. And a few think we could dip into the $600s/st – as we did last summer.

Roughly one-third think that prices will remain approximately where they are now. And only 19% think that HR prices will be higher in early August.

Recall that HR prices averaged $840/st in SMU’s latest market check on May 27. Also, hot band has been down $110/st over the past 10 weeks.

While very large buyers might already be securing numbers in the high $700s (where the low end of our range is), most are somewhere between $800 and $900 for standard spot buys. The variance depends somewhat on the steelmaker and buying power.

It’s hard to tell how the next bit will shake out, especially with the latest tariff threat. But here is what some of our survey respondents had to say before the S232 news broke on Friday.

“Too much HRC capacity.”

“It won’t go below $800/ton.”

“Demand is softening and unstable.

“Reaching market support and no big economy moves to drive either way.”

“This pricing cycle will follow the same pattern as the last several.”

“Reluctance to buy from end customers and mills’ willingness to try and fill open capacity.”

“Futures have been in the $800-$820 per ton range. I think mills will draw a line in the sand.”

“I initially thought we’d trend down into the high-$700s and that’d be it. But there is enough macro ‘noise‘“‘ to where I now think it drifts lower than that.”

“High average for past 24 months.”

“There’s too much mill capacity for sheet prices to stay elevated, and there are more mills coming online.”

“Too much supply, lack of discipline with mills, and service center pricing.”

“This is a comfortable number for the mills and the industry.”

“After getting lower over the next month, they start to rebound.”

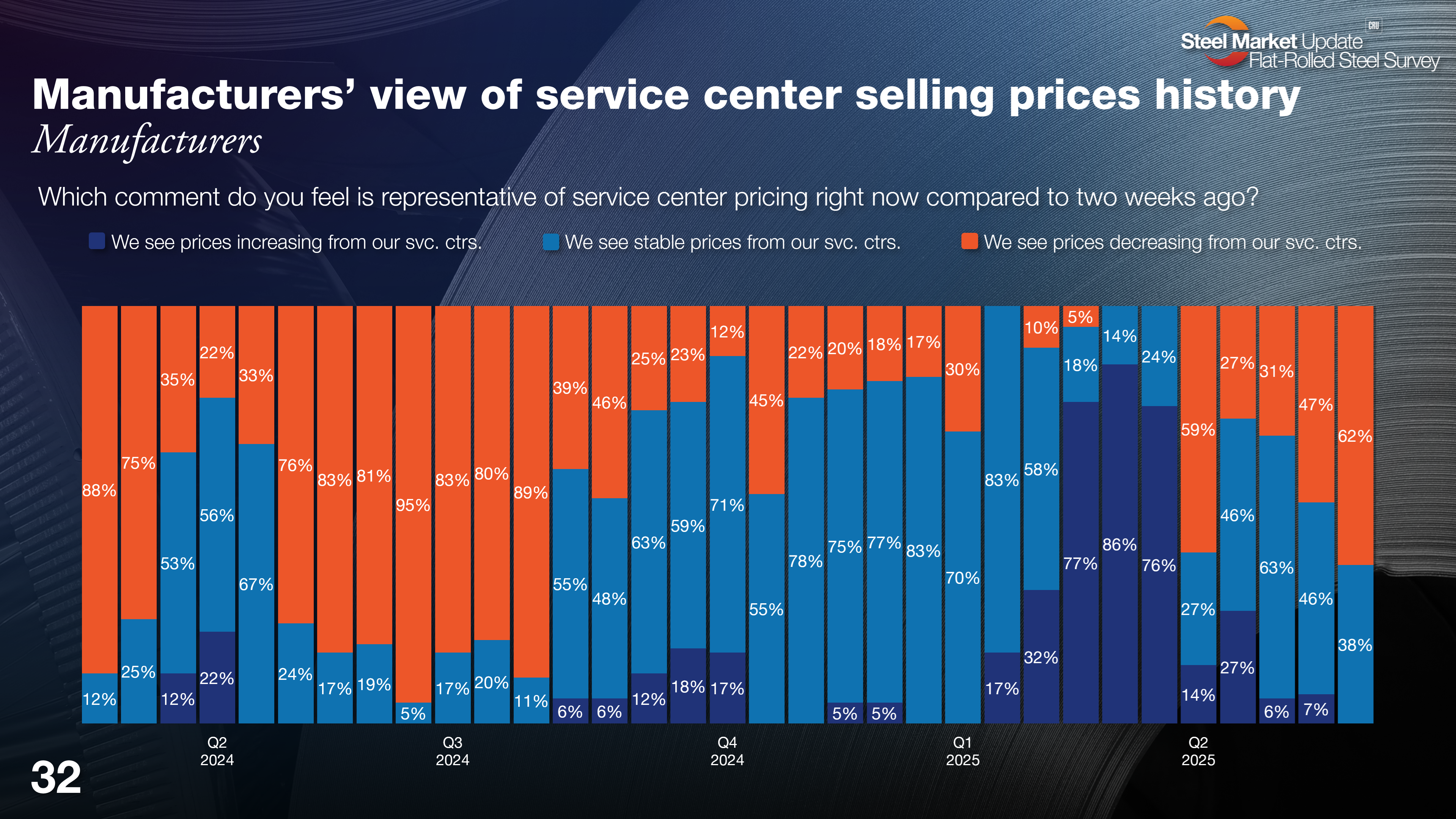

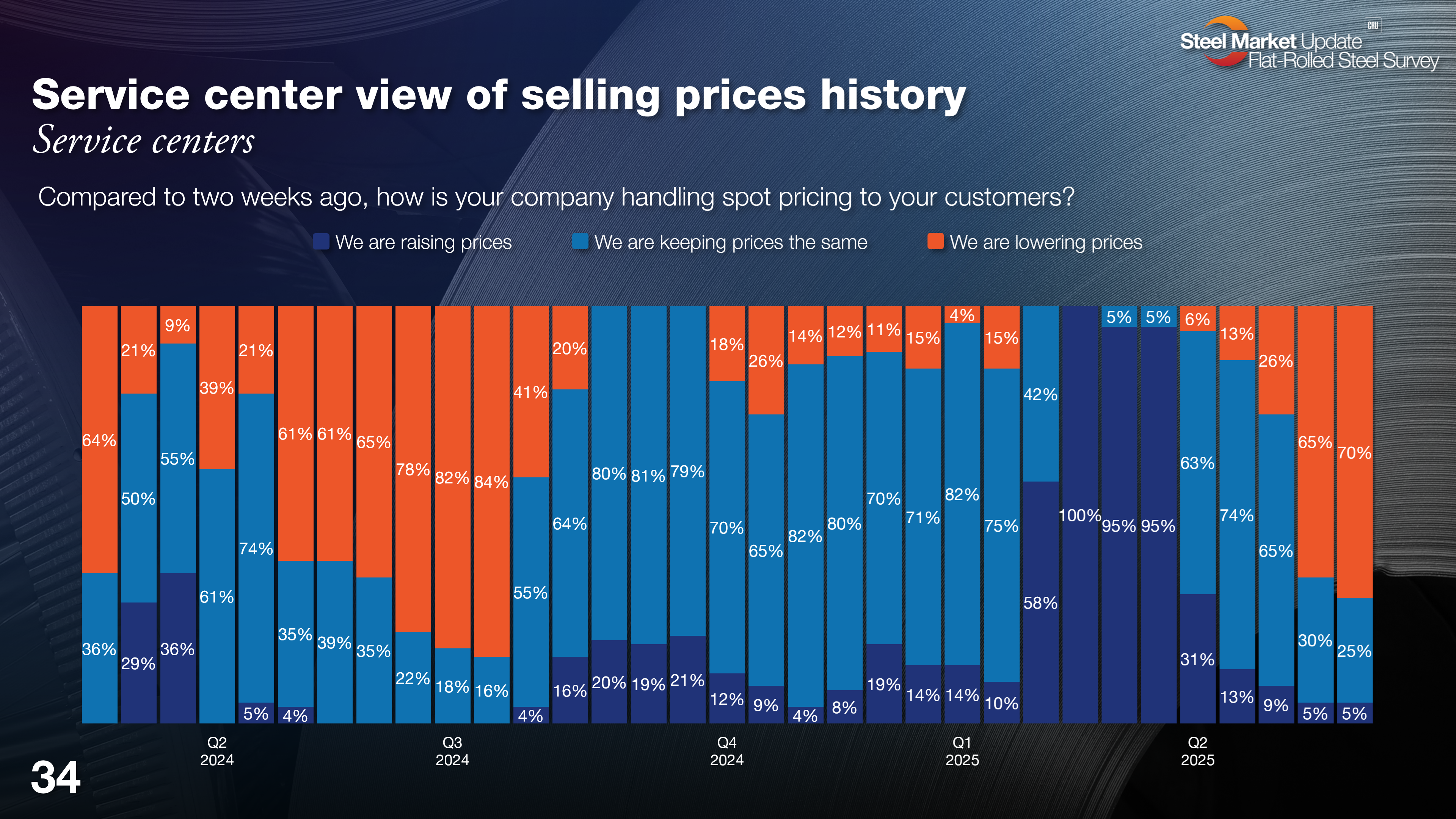

Service centers continue to lower prices along with mills

It’s not just mills that are lowering prices. Service centers continue to lower prices to their customers as well – as you can see in the next two charts.

Prices shot up in Q1 in anticipation of a revamped Section 232 tariff regime. But they’ve fallen throughout Q2 to date on uncertainty caused by ‘Liberation Day’ tariffs, a raft of other S232 investigations and tariffs, and the on/off nature of the trade measures.

A few comments:

“I’m not big on ‘shopping.’ Yet two service centers are looking. Some are rather close on pricing (.50 cwt variance).”

“Not only are service centers lowering their numbers, they are doing it aggressively. So we get the feel that they’re all bleeding a bit.”

“Lowering prices and still losing orders.”

“Forced to adjust to competitors seemingly dumping/aggressively pricing based on replacement cost (or lower).”

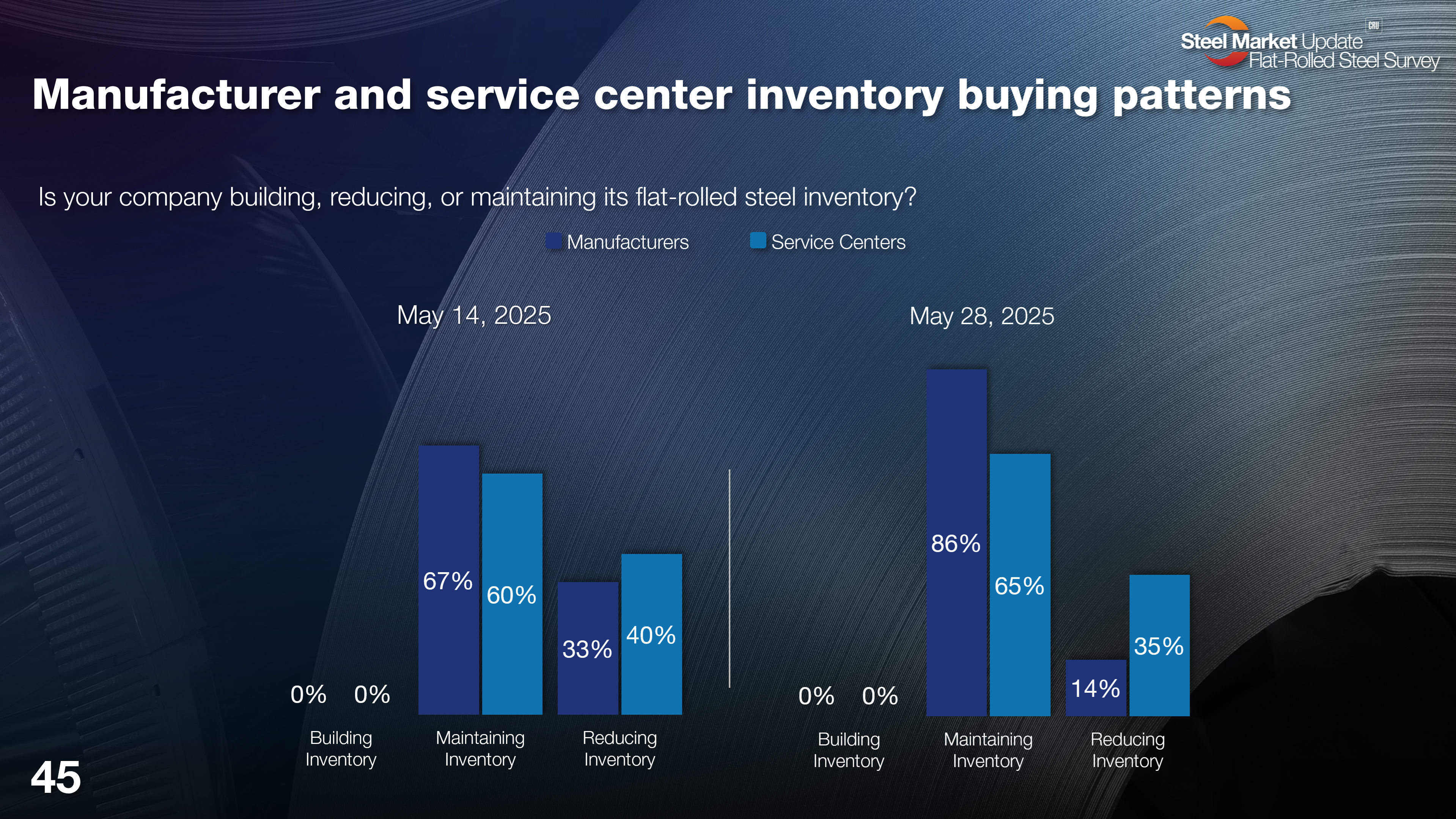

No one is restocking

But what remains very surprising, might I say astonishing, is that manufacturers and service centers alike are still completely refraining from building inventory. For the past three surveys – which cover the last six – steel buyers have been only maintaining or even drawing down their inventories.

It’s unprecedented. We haven’t seen a trend like that in our survey history. Not even during COVID.

Could that ultimately lead to a quick, sharp price reversal once buyers start building back inventories? It’s one worth thinking about, especially as the shock of 50% tariffs on imported steel hits the market this week.

Steel 101 Workshop

Don’t get caught singing the blues while some of your peers are strengthening their steel knowledge in Memphis, Tenn.!

SMU’s next Steel 101 will be held on June 10-11, 2025, in the Home of the Blues. Only four spots remain. You can get more info and register here. But don’t delay, space is going fast!

Our course is designed for professionals who want to quickly and effectively strengthen their steel industry expertise. We’ll do a deep dive into steel production, trading, and market dynamics. Not to mention an exclusive guided tour of Nucor Steel Arkansas.

And wherever we see you next – whether at Steel 101, Steel Summit, or one of our upcoming Community Chats – I want to say thank you for your time. All of us here at Steel Market Update truly appreciate your business.