Analysis

August 28, 2025

Final Thoughts

Written by Michael Cowden

Another record-breaking SMU Steel Summit is in the books. Thanks to all of you – attendees, speakers, sponsors, and exhibitors – for making it possible in what has been an uncertain year for steel.

All told, more than 1,500 people attended Summit this year. And hundreds of you participated in in our snap polls during the opening of the conference on Monday.

If you were there, you might have snapped a photo of the results. And even if you weren’t, I’d like to share with you now the wisdom of a sizeable steel crowd.

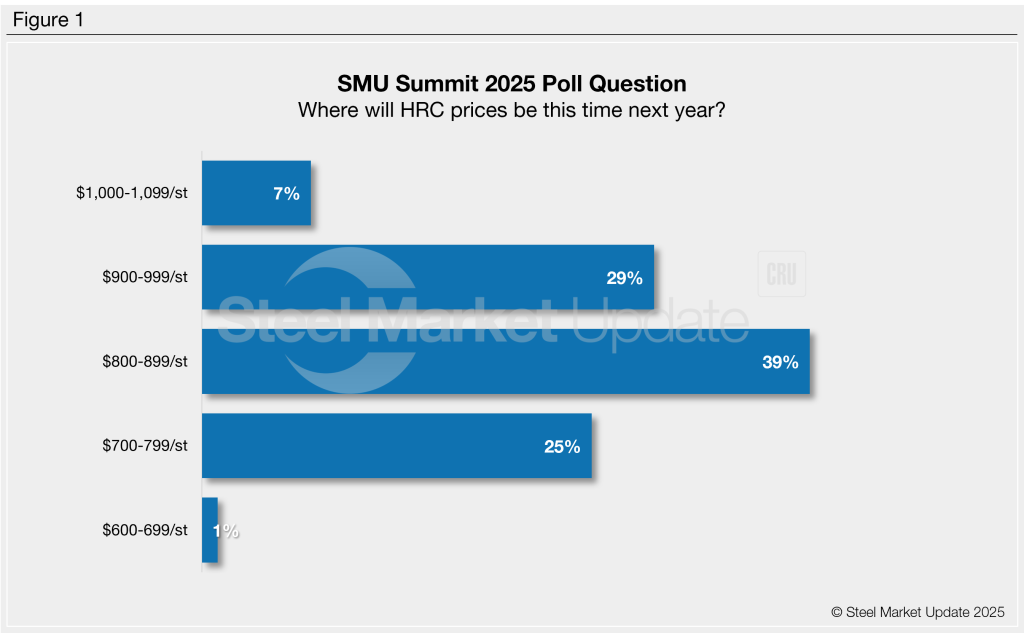

Where will HR be in August 2026?

We started with a perennial question: Where will hot-rolled (HR) coil prices be a year from now? Here are the results.

The responses look like a bell curve. The most common response (39%) was that prices would be in the $800s per short ton (st). In other words, roughly where we are now or a little higher.

Approximately equal numbers think prices will be significantly higher, in the $900s/st (29%), or significantly lower, in the $700/s st (25%), a year from now. And small minorities predicted that prices would either explode higher into the $1,000s/st (7%) or collapse into the $600s/st (1%) next year.

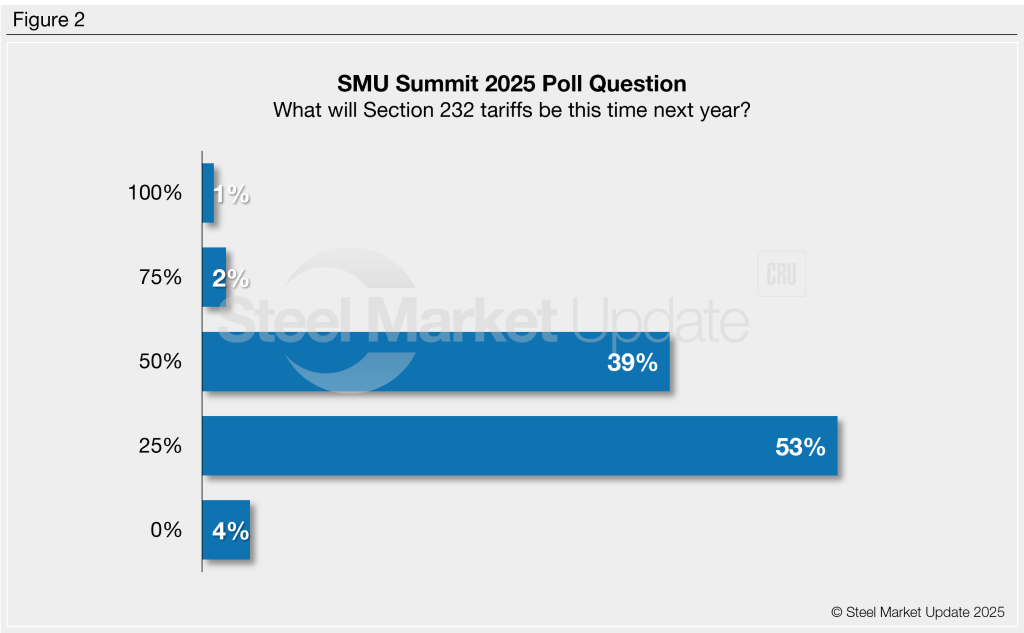

What will Section 232 tariffs be a year from now?

Your vote on HR prices might be strongly correlated with where you think Section 232 tariffs will be in August 2026. And that was the second question we asked the audience. Below are the results:

No bell curve on this question. Very few think Section 232 tariffs will be gone this time next year. And only a tiny minority think they’ll be increased to 75% or 100%.

The real debate is between those who think the Section 232 tariff remain at 50% and those who think it will be adjusted back to 25%. A narrow majority (53%) think President Trump will cut the Section 232 tariff back to the 25% by August 2026. And a sizeable minority (39%) think it will stay at 50%.

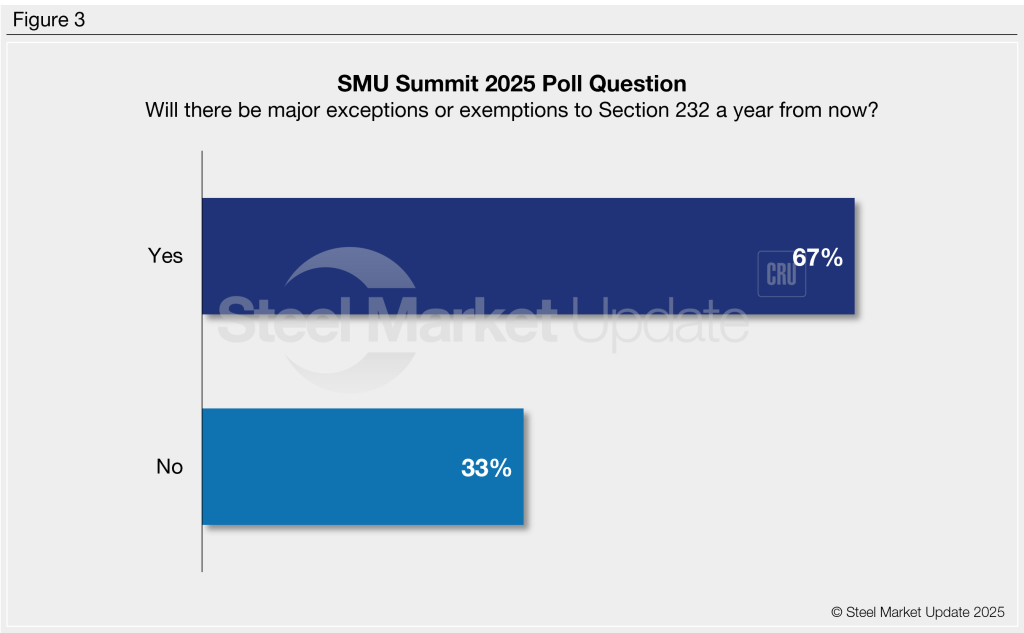

Will there be major exceptions or exemptions in ’26?

But the devil is in the details. That’s why the next question we asked the crowd was whether there would be major exceptions or exemptions to Section 232 by this time next year. This is how Summit attendees voted:

Approximately two-thirds of Summit voters think there will be major exemptions to Section 232 by August 2026. And about one-third think that Section 232 will be little changed a year from now. You could frame that as a debate about whether TACO applies to steel or not. But I don’t know that that’s the best way to put it.

Barry Zekelman, executive chairman and CEO of Zekelman Industries, talked about a “Fortress North America” trade policy during his fireside chat with me on the first day of Summit. And other speakers made similar remarks. Namely, that the Section 232 tariff on Canada and Mexico might be eased as part of USMCA negotiations next year and/or if Canada and Mexico clamp down further on imports from overseas.

Fwiw, both countries are already trying to do that. But Zekelman, a Canadian, said Ottawa wasn’t acting quickly enough to protect Canadian steel companies that are “on their knees” in the face of a 50% Section 232 tariff from the US.

Another theme that ran throughout the conference was that most people – whether they were for or against tariffs – would like to have more certainty around US trade policy. Why? Simple enough: It’s hard to plan for the future when you don’t know what the rules will be, and when they can change at the speed of a president’s social media posts.

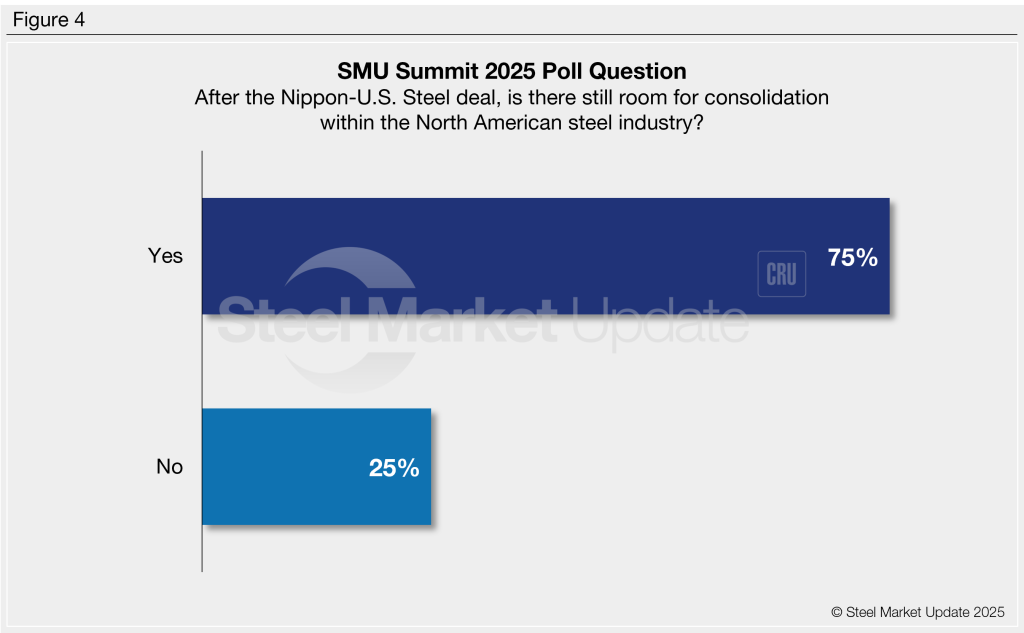

Summit attendees see more consolidation coming

Turning to M&A, last year, we asked Summit attendees about whether the Nippon/U.S. Steel deal would close. Two-thirds correctly predicted that it would. This year we asked a more general question – whether there was still room for consolidation within the North American steel industry. Here are the results.

A little to my surprise, three-quarters of voters said there was indeed still room for consolidation. Only 25% said there wasn’t.

As Wells Fargo Managing Director Timna Tanners noted during a panel discussion on Monday, there are only a handful of major flat-rolled steel mills left in North America, which limits the room for consolidation. That said, rebar – with only three major producers – is even more consolidated. And that market is characterized by high US prices, even in times of soft demand.

Meanwhile, as Reliance Inc. President and CEO Karla Lewis pointed out in a fireside on Tuesday, the service center level is far less consolidated than the mill level. Maybe that’s where Summit attendees see the consolidation happening?

I guess we’ll have to ask a more precise question next year.

Tariffs took center stage…

By the way, you might say I’m writing too much about tariffs in a year in which our keynote speaker was Astronaut Shane Kimbrough. My own goal for the event, which we started planning a year ago, was to move past election-year politics and have us thinking big and about the future.

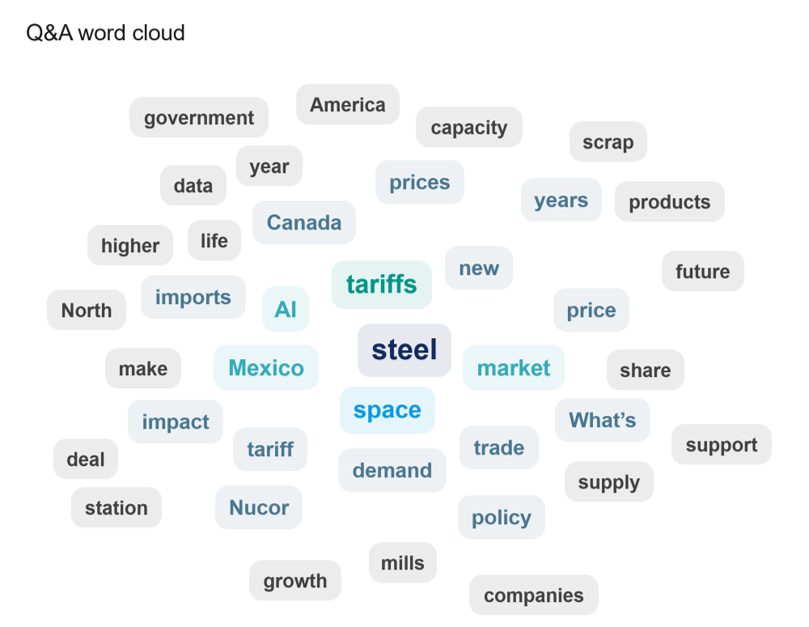

And we did achieve that, sort of. Take a look at the word cloud that we generated from the hundreds of questions submitted over the course of Steel Summit:

“Steel” will always be at the center. And, yes, you can see “tariffs” among the most-used words in questions. (I filtered out tariff-related terms like like “tariff” and “50%”.) You could also make the case that attendees asked about Canada and Mexico most often in the context of tariffs. (Btw, if I were able to form a word cloud from answers, I think “tariff” and “uncertainty” would be near the top of the list.)

But space and AI weren’t far behind

Still, attendees also asked a lot about AI, how people are already using it in their day-to-day business, and how they might be using it in the future.

Gene Marks, president of the Marks Group PC, provided a great overview of how AI is already in use everywhere from the office (e.g., preparing PowerPoint presentations) to the shop floor (e.g., self-driving forklifts). And many of the steel executives who spoke at Summit agreed that AI has a place in steel, that they were investing more into it, and that it was already playing a big role in certain aspects of business.

But there seemed to me to be more concern around moving AI into the physical world. Basically, trust is growing that AI can handle words and numbers in the digital space. But there is a leeriness about its readiness to handle physical things and physical processes.

Summit attendees asked a ton of questions to Shane about space, its mysteries, and his experiences outside the confines of Earth’s orbit. (I’m relieved to see I wasn’t the only space junkie.) So, again, thanks to everyone your participation. You helped steer the ship that was Summit ’25.

See you in the not-so-distant future!

We’ll next bring the steel community together at the Tampa Steel Conference on Feb. 11-13, 2026, at the JW Marriot Tampa Water Street. You can register here.

And don’t forget to mark your calendar for Aug. 24-26, 2026. That’s when we’ll gather again for the next SMU Steel Summit.

In the meantime, enjoy the Labor Day weekend. (We at SMU will be doing so. There will be no Sunday issue this week.) And drop me a line if you have any good ideas for next year’s Summit.