Prices

September 18, 2025

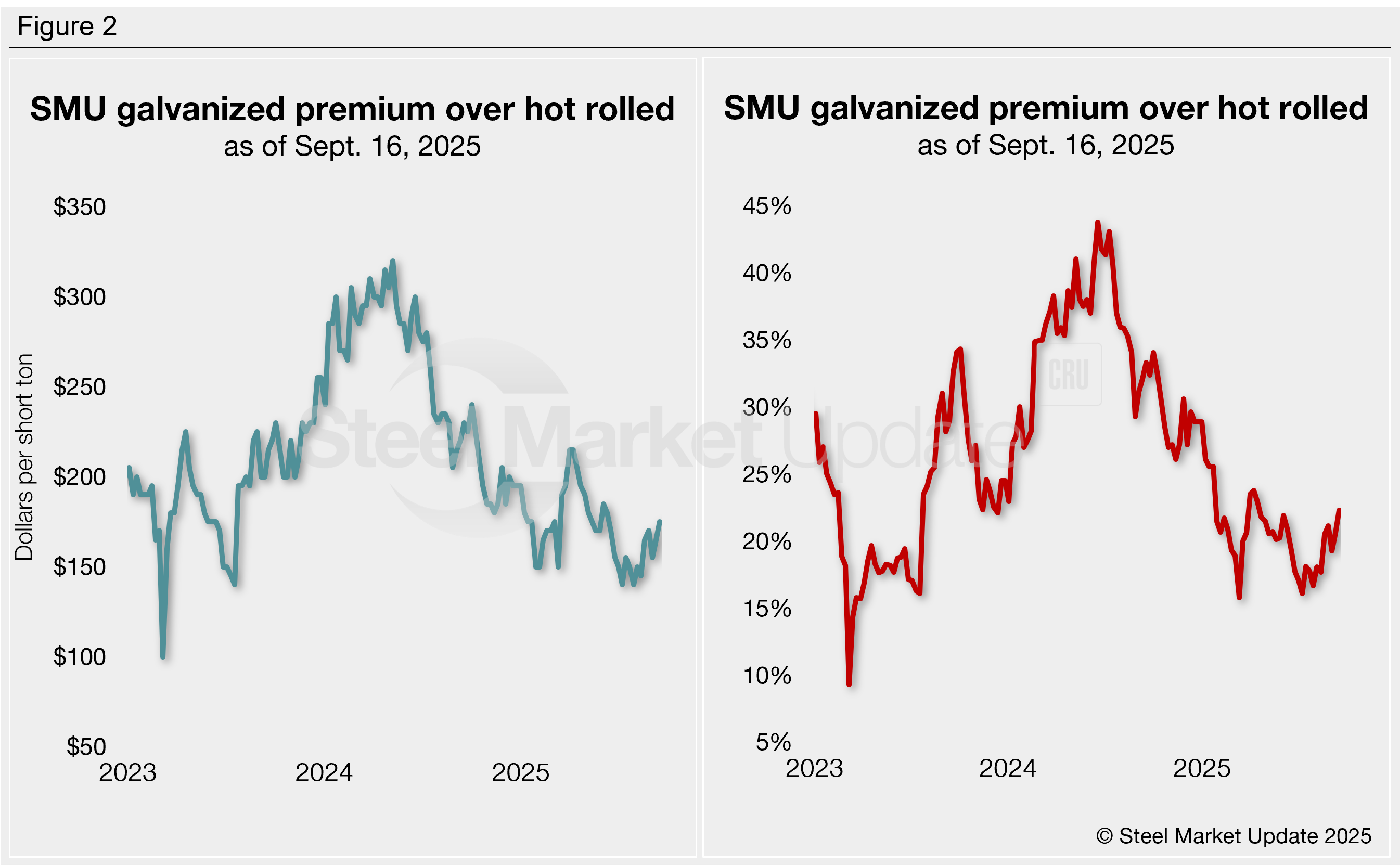

HRC-galvanized price gap edges higher

Written by Brett Linton

The premium galvanized coil carries over hot-rolled coil (HRC) coil has marginally widened in recent months. As of Sept. 16, the spread between these two products reached a three-month high of $175 per short ton (st), though it is still low by historical standards.

Recent trends

SMU’s average HRC price fell $15/st this week to $785/st. Prices have gradually fallen since peaking in the first week of July, holding steady or declining each week since for a total decline of $95/st. Prices today are 11% lower than they were three months prior and 17% below rates seen six months ago.

Meanwhile, galvanized (base) prices eased $5/st week over week (w/w) to $960/st. Unlike HRC, galvanized prices have somewhat stabilized recently, holding within a $15/st range over the last six weeks. Overall, galvanized prices have fallen $90/st, or 9%, since peaking in mid-June, down 16% from levels seen six months prior.

Figure 1 shows the pricing relationship between these two products since 2023. Visit our Interactive Pricing Tool to dive deeper into our steel prices and data.

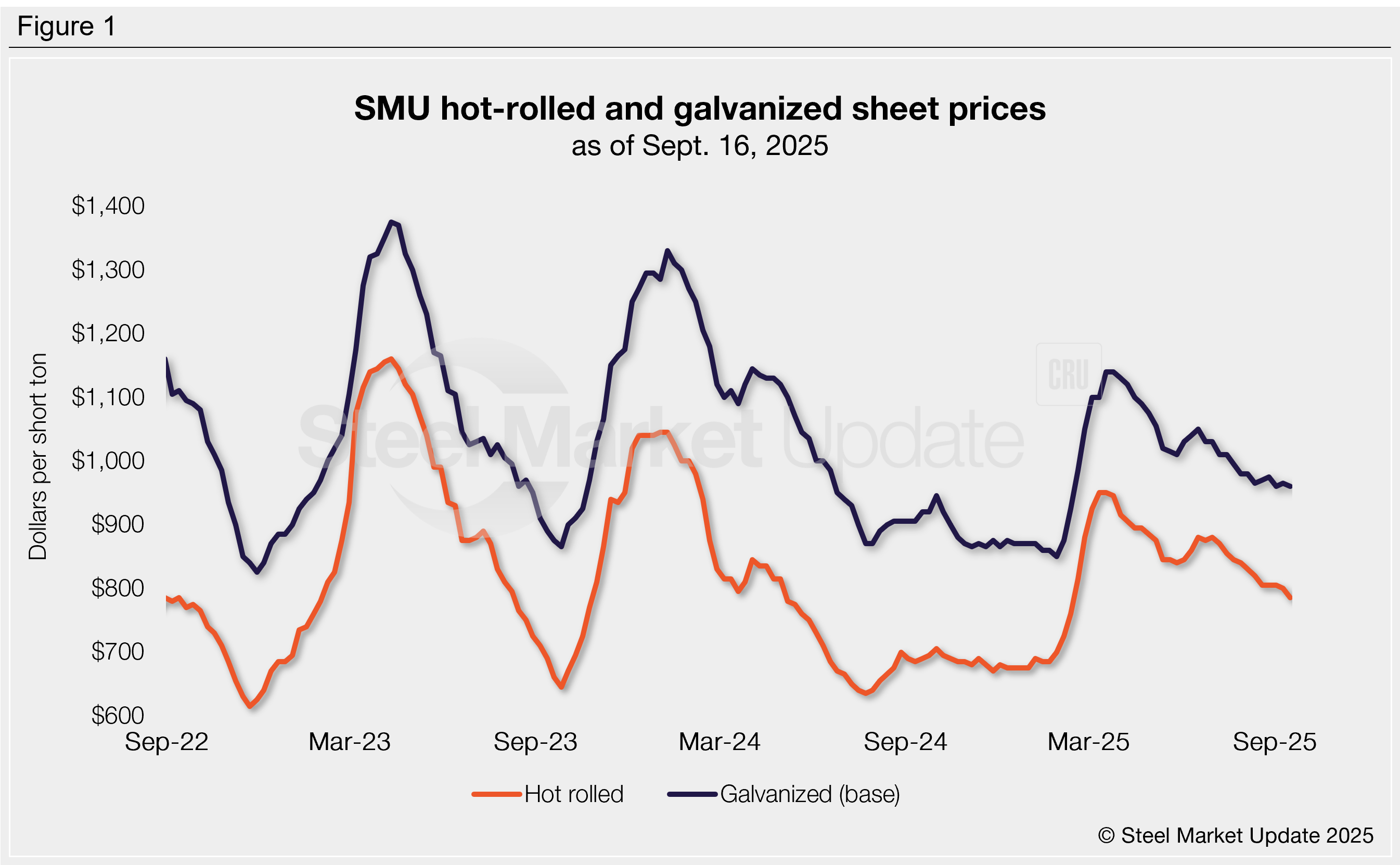

Galvanized premium shrinking

Currently, galvanized commands a $175/st price premium over HRC (Figure 2, left). Recently, the delta between these two products touched a two-year low of $140/st twice in July. Spreads over the past month resemble those seen around the start of this year and remain on the low side in comparison to recent years.

Around this time last year, we saw significantly higher spreads between $205-240/st. Over the past 12 months, the spread has averaged $179/st. Historically, pre-pandemic spreads were generally between $85-220/st in the 2010s.

Another way to compare these products is to look at the galvanized premium as a percentage rather than a dollar value. The right graph in Figure 2 shows the hot-rolled/galvanized price spread as a percentage of the hot rolled price.

The percentage premium tells the same story. After bottoming in July at 17%, it has ticked up since, rising to a three-month high of 22% this week. The July low was one of the lower percentage premiums recorded in recent years, just above the 16% low seen once back in March. This time last year the premium ranged from 30-35%, having eased from a near two-year peak of 44% seen last June.