Analysis

April 23, 2026

HR Futures: HRC curve reprices higher as market extends tightness into Q3

Written by Gaby Ain

As the steel market works through the first month of Q2 and the spring outage season, the US HRC futures curve continues to reflect a market adjusting to tightening conditions. The recalibration of near-term expectations sets the stage for how the curve has developed in recent weeks.

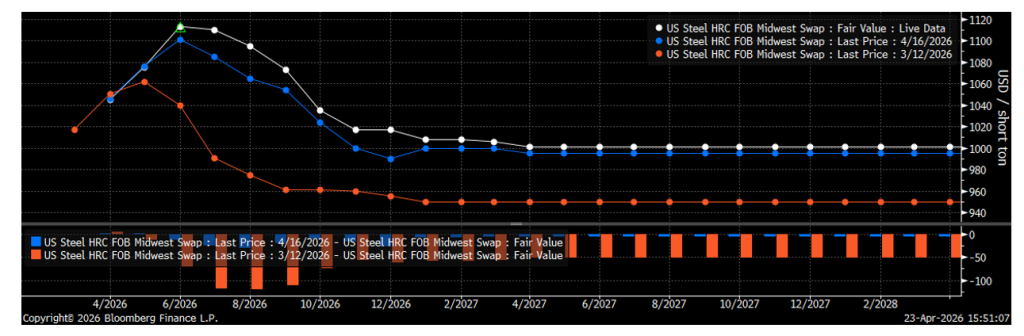

Back on March 12, the HRC forward curve (orange) was repricing stronger conditions, with the market starting to consider the duration of tightness. The peak was being priced around $1,060 in the May contract before declining more steeply into Q3’26, reflecting expectations that while tightness would persist near term, eventual normalization remained likely. A month later, April 16, that view had accelerated. The curve (blue) had repriced higher across the front half, with the peak of the strip shifting into June and approaching the $1,100 level. While the back half of the curve continued to reflect expectations for some easing, it did so at a higher level, indicating the market was assigning greater weight to the persistence of tight conditions. And those tight conditions being seen as a developing constraint leads us to today, April 23. The curve (white) has firmed again, with June and July futures now breaching the $1,100 threshold. Q3 and Q4 2026 have also moved higher, while the deferred months of the curve are pricing in a ~$1,000 band. The structure of the curve continues to reflect a market weighing near-term scarcity against expectations for some degree of longer-term normalization within the current tariff framework.

CME Midwest HRC Futures Curve (4/23 in white, 4/16 in blue, 3/12 in orange)

During this time, domestic raw steel production has ramped up, with weekly output reaching its highest levels since 2021 and capacity utilization ticking up to rates last seen in August 2024. Historically, increases in production during a rally have been associated with conditions observed prior to a peak. However, part of the recent increase may reflect mills positioning ahead of planned outages rather than a sustained shift in supply availability. Notably, despite higher production levels, spot availability remains constrained, raising questions about the pace at which supply is effectively reaching the market. Another factor complicating the outlook is imports, which indicated early signs of increased activity, albeit very gradually. Ongoing trade flow disruptions and logistical challenges may delay arrivals, extending the timeline for meaningful supply response. Additionally, US trade officials have signaled ahead of USMCA renegotiations that steel tariffs on key partners such as Mexico are unlikely to revert to prior levels, reinforcing a structurally higher tariff environment.

On the demand side, conditions that had appeared relatively stable are now showing signs of modest improvement. The ISM Manufacturing PMI has remained in expansion for three consecutive months, and certain end markets, including automotive, have demonstrated resilience. If demand remains stable or improves further while supply responses are delayed, the timing of market rebalancing may become less certain.

Taken together, a question that arises is whether supply can respond sufficiently under current conditions. The market has not experienced this degree of tightness within a higher tariff environment. The evolution of how this dynamic will play out will likely be reflected in lead times, the pace and timing of actual import arrivals, and whether the back end of the futures curve moves higher.

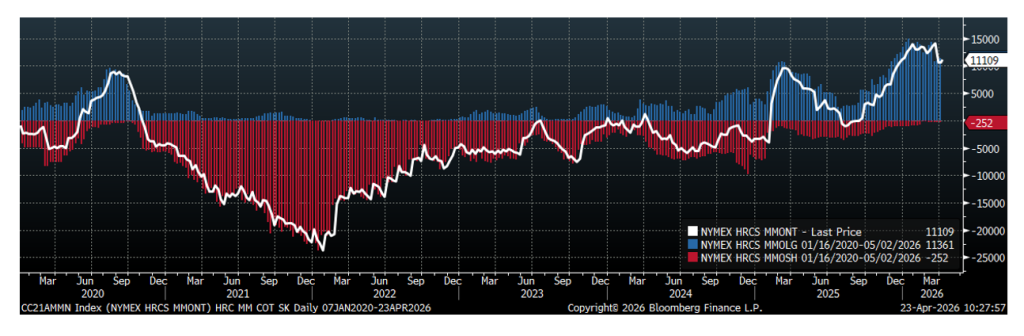

CME HRC Money-Manager Positioning

CME HRC money manager positioning remains net long alongside the rally. However, that build appears to have moderated, with recent changes in positioning relatively limited. Notably, this stabilization is not being driven by an increase in short positions, which remain near historically low levels, suggesting positioning is not yet crowded but may be transitioning away from a purely momentum-driven phase.

Overall, the market continues to reflect tight conditions, and recent price action has remained firmer than earlier expectations. Mills continue to demonstrate significant pricing discipline. Spot availability remains limited, lead times are extended into July and in some cases August, and pricing has continued to move incrementally higher, reflecting sustained control over order books.

The curve continues to reflect constrained conditions, and a shift in that dynamic will likely depend on whether supply begins to respond.

Disclaimer: The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Flack Global Metals or Flack Capital Markets should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his or her opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice of a financial professional before taking action in financial markets.