Analysis

June 12, 2026

CRU: Global sheet prices diverge, USA stands out with gains

Written by Juliana Guarana

This item was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

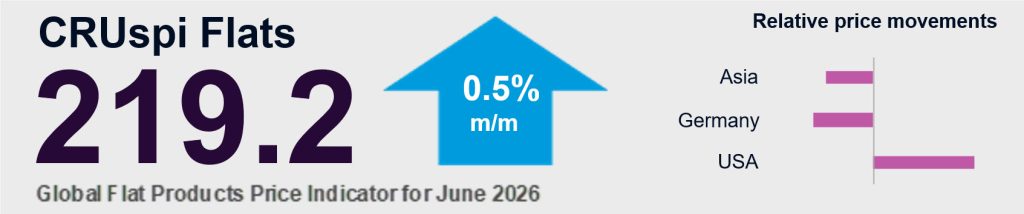

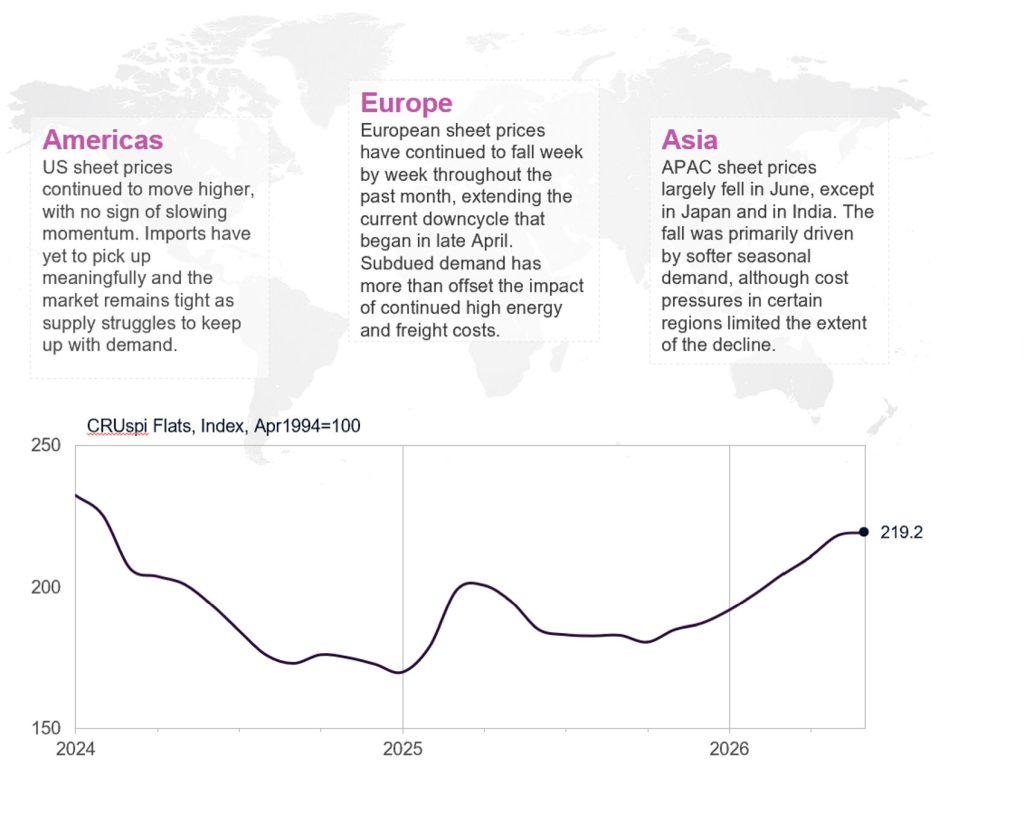

CRU’s Global Flat Products Price Indicator (CRUspi Flats) was 219.2 in June 2026, up 0.5% m/m. Sheet prices in the USA continued to move higher over the past month as supply remained tight in the country, while prices in APAC diverged amid weak seasonal demand. In Europe, prices continued to fall due to subdued end-use demand.

APAC sheet prices diverge amid weak seasonal demand

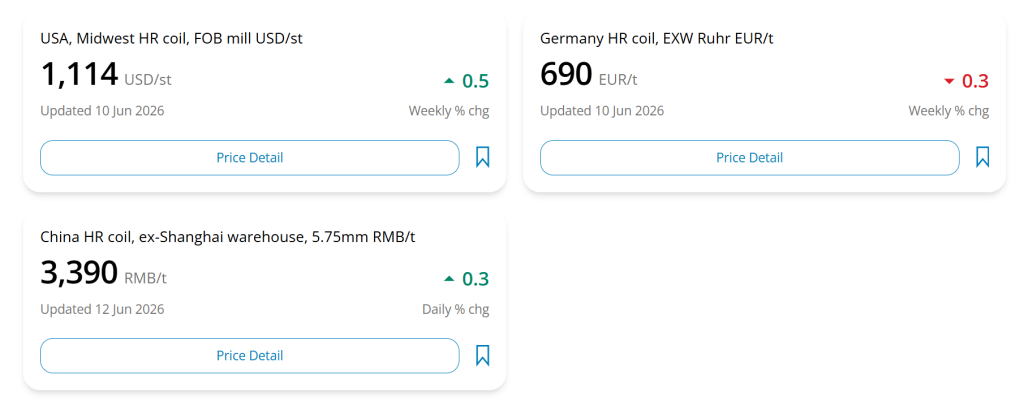

Domestic sheet prices in China largely decreased over the past month on the back of subdued end-use demand and elevated production levels. The rainy season and high temperatures in the country weighed on construction activity, while resilient manufacturing demand partially offset the downside. Meanwhile, relatively elevated margins encouraged Chinese mills to sustain ample output.

In Southeast Asia, sheet prices also declined m/m amid subdued regional demand. Japan bucked APAC’s regional trend and average sheet export prices increased in the country over the past month as Japanese mills continued to pass through higher production costs.

Indian domestic sheet prices remained largely unchanged m/m as higher production costs offset the downward pressure stemming from subdued market activity. Indian buyers restricted purchases to immediate needs. Major Indian mills, however, were reluctant to lower price offers due to cost pressures and redirected more volumes to the export market to manage rising inventories.

EU sheet prices continue fall amid subdued demand

In Europe, sheet prices continued to decline over the past month, despite high energy and freight costs, due to reduced end-use demand. Inventory levels in the region remained elevated and EU buyers continued to hold back on new purchases, suppressing apparent demand. Most sheet prices in Europe, however, remained above pre-Middle East conflict levels.

In Turkey, domestic HR coil prices continued to edge up m/m despite weak demand driven by higher energy prices and more expensive steelmaking raw materials and semi-finished products.

US sheet prices rise further as supply remains tight

US sheet prices continued to move higher on the back of steady demand from the automotive sector and data centres construction. Supply constraints are reinforcing the upward price trajectory and spot availability remained scarce as service centre inventories continued to decline. In parallel, import volumes remained well below monthly averages that were the norm before the reinstatement of Section 232 in 2025.

In Brazil, domestic sheet prices increased m/m in June amid broadly stable demand conditions and a reduction in imports given the antidumping duties imposed earlier this year on Chinese material.