SMU survey: Buyers report mills still willing to negotiate prices

Negotiation rates have edged lower from our previous market check, a downward trend witnesses since July.

Negotiation rates have edged lower from our previous market check, a downward trend witnesses since July.

SMU’s steel price indices showed mixed signals for a second consecutive week. Our hot rolled, cold rolled, and plate price indices inched lower from last week, as the galvanized index held steady and Galvalume's ticked higher.

Following June’s slump, the amount of finished steel entering the US market partially rebounded in July, according to SMU’s analysis of data from the US Department of Commerce and the American Iron and Steel Institute (AISI).

Global crude steel production fell by 4% month over month (m/m) in July, led by a major drop in Chinese output, which fell 9% m/m.

Construction spending in the US in July was slightly lower than June. Despite the decline, it increased notably year on year (y/y).

Growth in the US economy continues to struggle in most districts. The Federal Reserve’s Beige Book report for August shows two-thirds of reporting districts flat or declining economic activity.

We had a wonderful time at last week’s Steel Summit Conference, seeing so many familiar faces and catching up with friends within the industry.

SSAB plans to spend $12 million to boost production capacity at its electric-arc furnace (EAF) plate mill in Mobile, Ala. The Sweden-based steelmaker will do that by expanding the existing furnace there. Shot blast equipment will also be upgraded. The expanded capacity is expected to come online late next year. The mill currently has an […]

SMU’s Monthly Review provides a summary of important steel market metrics for the previous month. Our August report includes data updated through August 30th.

SMU’s latest steel buyers market survey results are now available on our website to all premium members. After logging in at steelmarketupdate.com, visit the pricing and analysis tab and look under the “survey results” section for “latest survey results.”

This CRU Insight explores how decarbonization will play a significant role in redefining steel trade patterns by shifting regional competitiveness and increasing steel demand needs.

“The US economy, despite some near-term weakness I suggest in early 2025, is going to be strong," Dr. Anirban Basu said this week.

The Chicago Business Barometer edged up in August but remains in contraction territory, according to the latest release from Market News International (MNI) and the Institute for Supply Management (ISM).

Current steel mill lead time averages are a few days longer than levels seen one month prior, but remain near historical lows for both sheet and plate products.

Both our Current and Future Indices are now up to multi-month highs, indicating continued optimism among steel buyers.

Steel buyers found mills slightly more willing to negotiate spot prices this week, according to our most recent survey data. Though this negotiation rate has ticked up vs. our previous market check, overall rates have been trending downward since July’s highs.

Steelmaking raw material prices have moved in differing directions across August, a change of pace from the declines seen in June and July, according to SMU’s latest analysis.

Canada’s government has ordered an end to the brief rail stoppage which had threatened to disrupt the movement of commodities.

The July AIA ABI score has recovered nearly six points over the last two months following the near four-year low recorded in May

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market events.

SMU’s Steel Buyers’ Sentiment Indices moved in differing directions this week. Both indices have generally trended downward across 2024, but continue to indicate optimism among steel buyers.

SMU's latest steel buyers market survey results are now available on our website. Here are some key points that we think are worth your time.

Chinese steel export prices decreased for the eleventh week in a row, with all steel products recording losses of 2-3.7% compared to the previous week.

Three out of four of our market survey respondents report that steel mills are open to negotiating new order prices this week, a slight decline compared to our previous market check.

Steel buyers continue to report short mill lead times for both sheet and plate products, according to SMU's latest canvass of the market. Lead times for hot-rolled and plate products marginally increased from our late July survey, likely due to limited restocking in anticipation of upcoming mill outages for scheduled maintenance.

This Premium analysis covers North American oil and natural gas prices, drilling rig activity, and crude oil stock levels. Trends in energy prices and rig counts are an advanced indicator of demand for oil country tubular goods (OCTG), line pipe, and other steel products.

New York state’s manufacturing activity improved in August but remained in contraction territory, according to the latest Empire State Manufacturing Survey from the Federal Reserve Bank of New York.

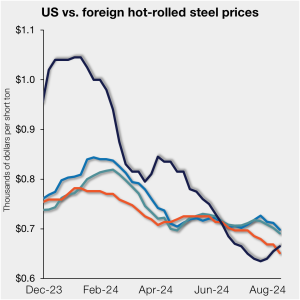

US hot-rolled (HR) coil prices are nearly even with prices for offshore material on a landed basis as domestic tags continue to inch up.

The Trade Remedies Authority (TRA) in the UK has proposed raising the tariff rate quota (TRQ) for imports of hot rolled sheet steel because of blast furnace closures at the Port Talbot works in south Wales. Tata Steel shut down one BF in July with the second to follow in September ahead of a switch […]

Steel Market Update is pleased to share this Premium content with Executive members. For information on how to upgrade to a Premium-level subscription, contact info@steelmarketupdate.com. Flat rolled = 64.2 shipping days of supply Plate = 60.9 shipping days of supply Flat rolled Flat-rolled steel supply at US service centers grew in July with restocking as […]