Worthington Steel logged higher earnings in its fiscal fourth quarter of 2025, though sales fell on softer prices and toll volumes.

The Columbus, Ohio-based service center logged net earnings of $55.7 million in its fiscal fourth quarter ended May 31, up approximately 5% from $53.2 million a year earlier. However, net sales fell nearly 9% to $832.9 million in the same comparison.

Volumes, meanwhile, dropped 5% to 982,180 short tons (st) in the quarter vs. a year earlier.

Worthington said lower net sales were driven primarily by lower average selling prices as well as lower toll volumes.

The company reported that the mix of direct tons vs. toll tons processed in fiscal Q4’25 was 60% to 40%, compared with 58% to 42% in the year-earlier quarter.

“Despite a mixed economic environment, our team executed well in the fourth quarter, advancing key growth initiatives while maintaining our focus on safety and partner relationships,” Worthington President and CEO Geoff Gilmore said in a statement after markets closed on Wednesday.

Among the highlights of the quarter were Worthington closing on its acquisition of Sitem earlier this month. The deal allows Worthington to further its investments in electrical steels and to gain market share in key sectors, Gilmore said.

Sitem SpA is an Italy-based producer of electric motor laminations.

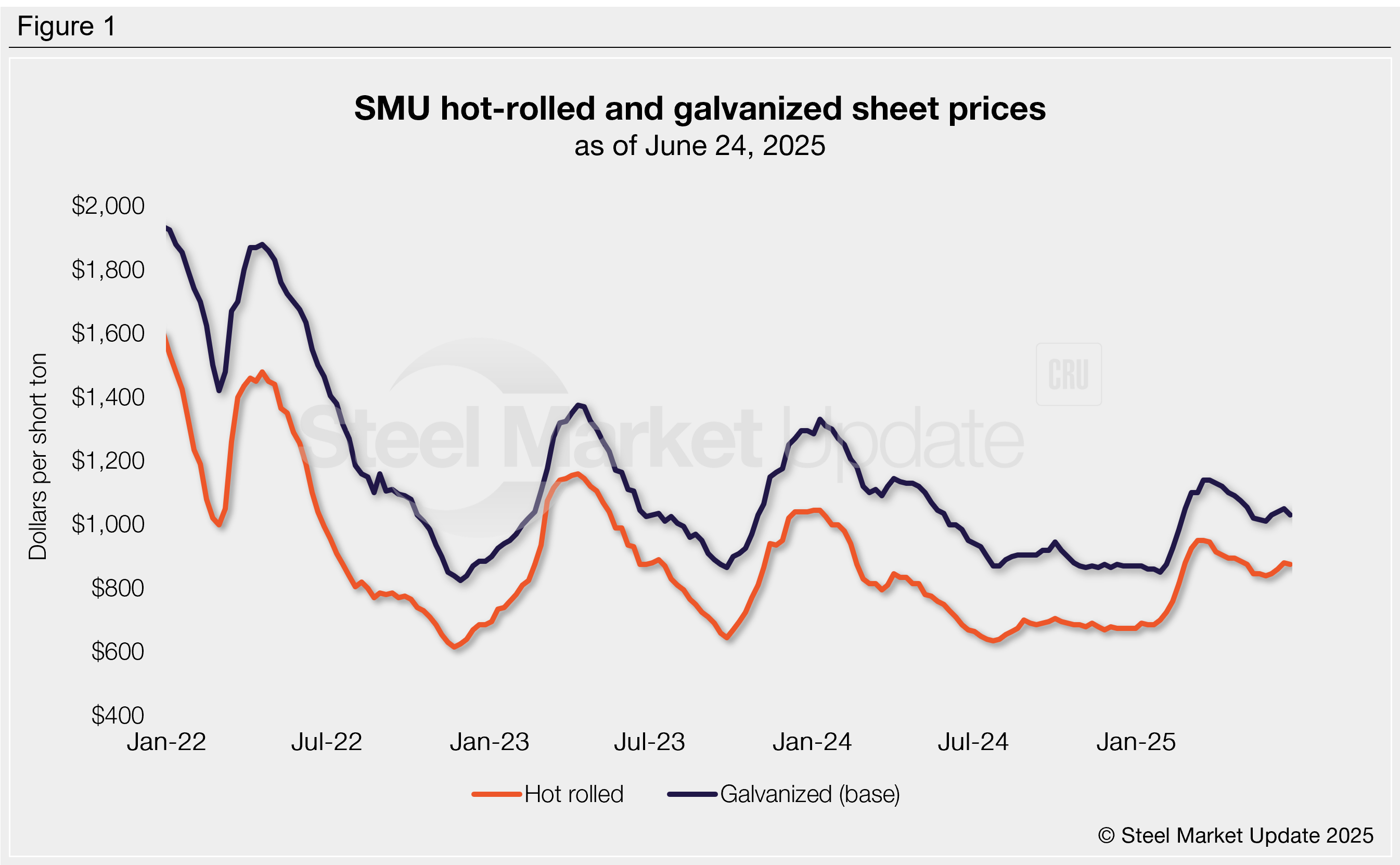

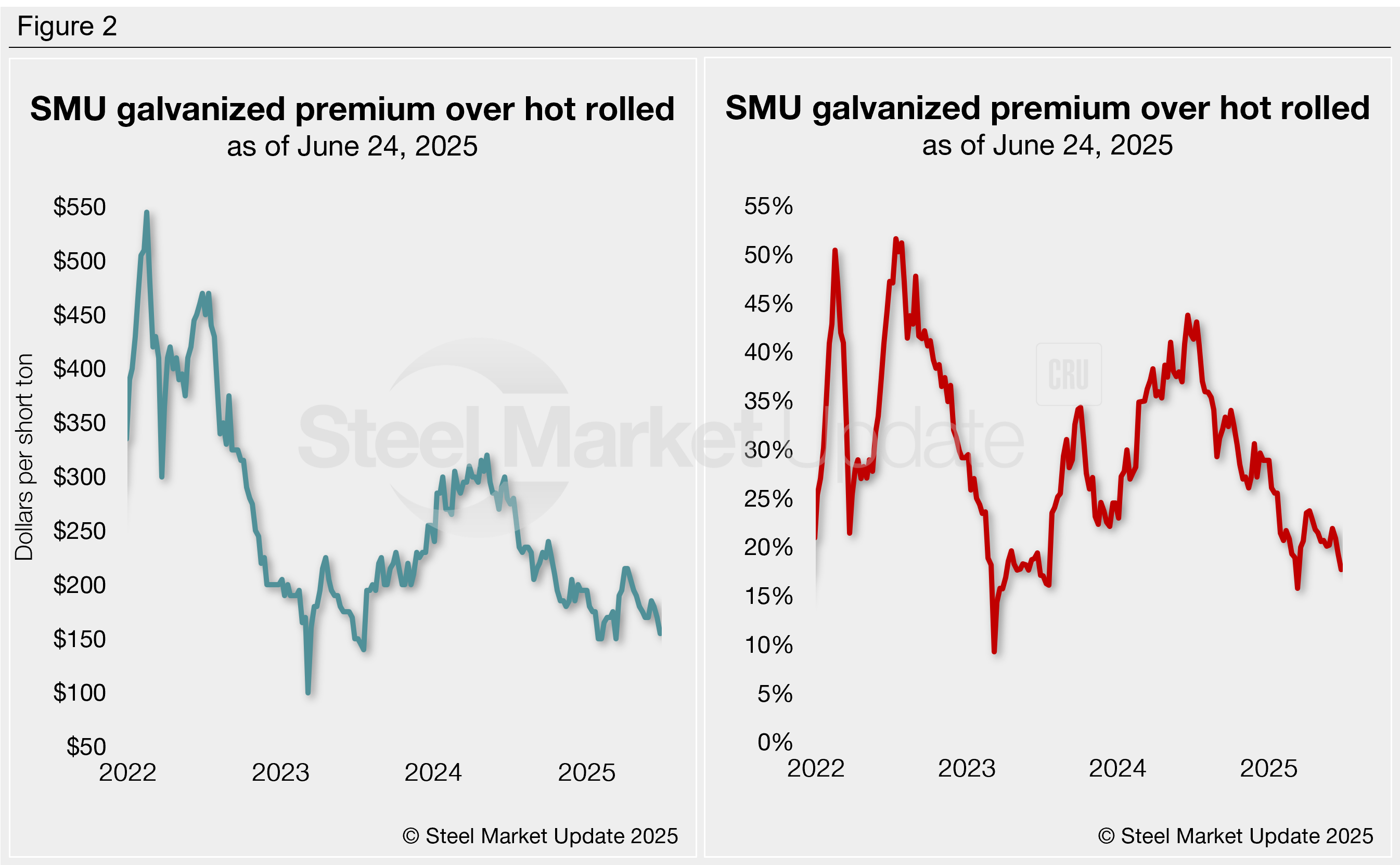

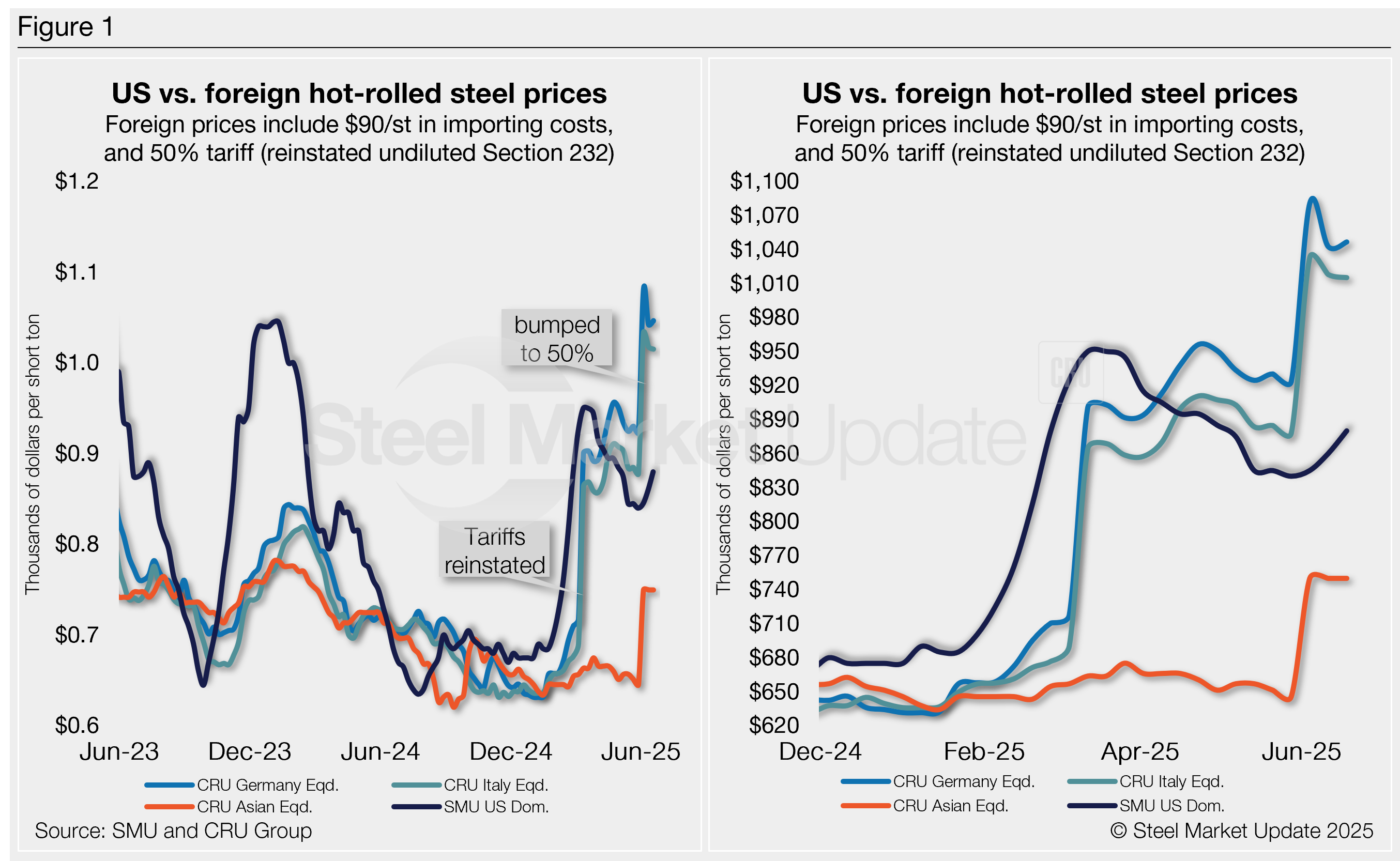

The premium galvanized coil carries over hot-rolled (HR) coil has narrowed further since our May update, shrinking for the third consecutive month. As of June 24, the spread between these two products is just $5 per short ton (st) above the lowest level recorded in almost two years.

Recent trends

SMU’s average hot-rolled coil (HRC) price eased by $5/st this week to $875/st, the first week-over-week (w/w) decline since late May. Meanwhile, our galvanized index slipped $20/st w/w to $1,030/st (base), also the first weekly decline in three weeks. Prior to June, both HRC and galvanized prices had trended lower from late March through late May.

HRC prices today are 7% lower than they were three months ago but up 27% compared to the start of 2025, while galvanized prices are down 10% and up 18%, respectively. Figure 1 shows the pricing relationship between these two products since 2022.

Galvanized premium shrinking

Currently, galvanized commands a $155/st price premium over HRC, marginally above the $150/st-low seen three times since mid-2023 (Figure 2, left). Spreads over the past month resemble those of February, March, and July 2023.

Around this time last year, we saw spreads between $270-300/st, though over the last 12 months it has averaged exactly $200/st. Historically, pre-pandemic spreads ranged mostly between $85-220/st during the 2010’s.

Another way to compare these products is to look at the galvanized premium as a percentage rather than a dollar value. The right graph in Figure 2 shows the hot-rolled/galvanized price spread as a percentage of the hot rolled price.

The percentage premium tells a similar story. It has shifted lower across the last year, falling to 18% this week. This is the second lowest percentage premium recorded in almost two years, just above the 16% low seen one week back in March.

This time last year the premium touched a near two-year high of 44%, an upwards trend generally witnessed since the March 2023 low of 9%. Compare this to the record high of 52%, which was seen in July 2022.

We’ve all received the email sign-off: Thank you for your attention to this matter. Just a bit of corporate formality. A way to grease the wheels in inter-office communication. Unless you’re President Donald J. Trump talking on your Truth Social account. In that case, the stock phrase may be a warning to both Israel and Iran to respect a newly announced ceasefire.

But is there a ceasefire? We hesitate to write anything at this point because the geopolitical situation in the Middle East is about as clear as the hot-rolled coil market in North America. Heck, it might be giving the tariff situation a run for its money in terms of not knowing which way is up.

Also, whatever we write will probably be out of date by the time we type it.

What is clear is that there is a lot to watch out for, especially these days, as far as international shipping, the flow of scrap, and the like, goes.

On the lookout

There are several things to be careful about as we attempt to transact business in the current market fray.

Firstly, do not overcommit your assets or business strategy to newly minted policies that can change at the decision of one man or one government department at any time.

A prime example would be the US tariffs. They are implemented, then delayed, or they are suspended. When we thought they would be fixed at a certain percentage, the next day, they were doubled. Resist the temptation to go all in on a policy that initially benefits you. The next day, they could be going against your interests.

Be aware of geopolitical events that may impact your markets or increase your costs. The large increase in ocean freight rates from the US could have drained the profits of exporters if they had not paid attention to the overall geopolitical and economic situation.

Another example is the upcoming port fee increases for Chinese-built ships and the fleets containing them. Although this has been watered down, thankfully, it may reduce the supply of ships available for international trade.

Expect the unexpected, no matter how unlikely you think certain things can happen. Did anyone think the US and Israel would be bombing Iran a month ago? Maritime freight rates have increased for cargoes originating in Southeast Asia and destined for the MENA region. Did anyone think that DRI, pig iron, and autos would be subject to tariffs?

Don’t underestimate the level of tariff retaliation by other nations and the collateral damage they can cause. An example is the reduced steel production in other countries as a result of tariffs and protectionism. This affects the flow of products like scrap and other ferrous raw materials.

Rough waters ahead?

We’ve said before we wanted to refrain from writing “buckle up.” In this case, though, perhaps the better analogy is: When on the water, be sure to have access to a life preserver. And if you’re on land, map out your nearest shelter, or at least be ready to stop, drop, and roll. Or is that for a fire?

Regarding fire, perhaps the best course of action in such times is to hold onto your common sense—and keep your powder dry.

Or, maybe, hope against hope, everything will end up turning out A-OK. Stranger things have happened…

Uneven demand for galvanized steel in June reflects a market that remains mired in uncertainty, according to industry sources.

That was the consensus during Tuesday’s monthly Heating, Air-Conditioning & Refrigeration Distributors International (HARDI) Sheet Metal/Air Handling Council call.

SMU provides sheet updates to the council of wholesalers, service centers, distributors, and manufacturers who buy or sell galvanized steel at each month’s call.

“I think no one really knows what to make of this market,” said one executive at an HVAC supplier.

The also noted the latest curveball: a conflict in the Middle East.

“We’re barely in the $50s [hundredweight], and we now have 50% tariffs. It’s an uncertain market. There are a lot of fundamentals that would typically put prices above where people would expect them to be. It just speaks to subpar demand,” the HVAC executive said.

Tariff uncertainty remains a primary concern. Buyers have opted for caution as they wait to see how long a 50% Section 232 tariff will be applied to imports. In the meantime, they are “buying only what’s needed when it’s available,” he said.

“May saw lower demand across all segments, and June has picked up a bit. We are definitely surprised by the continuation of black swan events and how they’ve not triggered more demand or more pulling forward of demand,” a service center executive said.

He continued, “I think buyers are fatigued right now.”

Another service center executive told the group that mills are mostly delivering on time and that inventory levels remain balanced. He predicted that pricing would remain relatively flat through the summer.

“The last week or so has been a little quiet compared to what we had in May. I would say overall our inventory levels are good. Overall volume has been steady. Since lead times are short and we’re able to get steel, centers can just wait for stuff to come in,” the second service center source said.

“I think pricing is going to just bounce in a fairly steady range for a while until we see whether buyers begin to purchase onshore again. I don’t know what will do that. You would think a 50% tariff would, but we are not seeing that reflected in the mill books yet,” he said.

A fabricator executive stated that customers are become numb to steel news and are purchasing only as needed.

“They’re not confident enough that the president is going to stick with tariffs this time around. And there is enough supply to absorb any demand punches that come through,” he said.

In an informal poll conducted at the close of the call, most participants saw prices remaining relatively flat, give or take $2/cwt for the next 30 days. Callers expect base prices to increase by more than $2/cwt in the next six months. And the majority of callers expect prices to be in the $50s/cwt a year from now.

Executives also considered what might happen with the price gap between hot-rolled coil and galvanized steel base prices. That spread has been roughly $10/cwt for most of the post-pandemic market. But that figure has narrowed more recently to pre-pandemic levels of approximately $7-/cwt.

SMU participates in a monthly steel conference call hosted by HARDI and dedicated to better understanding the galvanized steel market. The participants are HARDI member companies, wholesalers who supply products to the construction markets. Also on the call are service centers and manufacturing companies that either buy or sell galvanized sheet and coil products used in the HVAC industry and are suppliers to HARDI member companies.

Prices for steel sheet edged down this week despite Section 232 tariffs remaining at 50% and a US strike on nuclear facilities in Iran over the weekend.

Case in point: SMU’s hot-rolled (HR) coil price stands at $875 per short ton (st) on average. That’s down $5/st from last week and marks the first decline since President Trump announced plans in late May to double S232 tariffs.

The declines reflect continued uncertainty about tariff policy and demand. Noting limited spot activity, several market participants said that tariff fatigue had been replaced by a more broad-based fatigue. And while inventories have declined, lead times haven’t significantly extended – meaning buyers don’t feel much urgency to buy now.

In the past, for example, a massive increase in tariffs combined with a conflict in the Middle East would have sent oil prices soaring – and steel prices along with them. But market participants said such shocks have become normalized to the point that they have lost their ability to shock markets.

But not everyone took that view. Some sources predicted that uncertainty around demand would keep buyers cautious – something that could lead to higher prices in late Q3 or Q4, especially should imports remain low and should buyers continue to reduce inventories.

They also noted that current pricing, while not as high as some had predicted initially after the 50% tariffs were announced, was still strong by historical standards. At current levels, they noted, mills remained profitable. And there is no need for producers to chase HR toward $1,000/st, a number which might only serve to make imports attractive again.

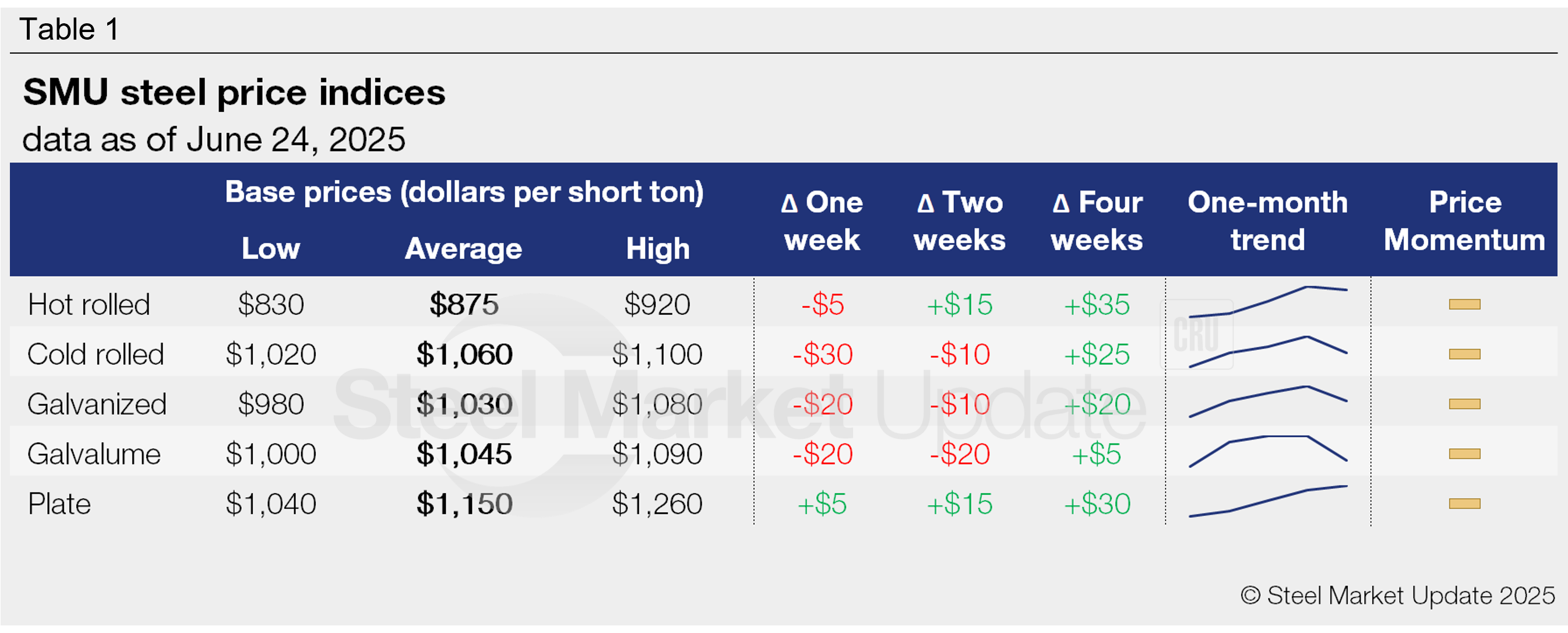

In light of this, SMU’s price momentum indicator has been adjusted from higher to neutral for all sheet and plate products, signaling that we see no clear direction for prices over the next 30 days.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil

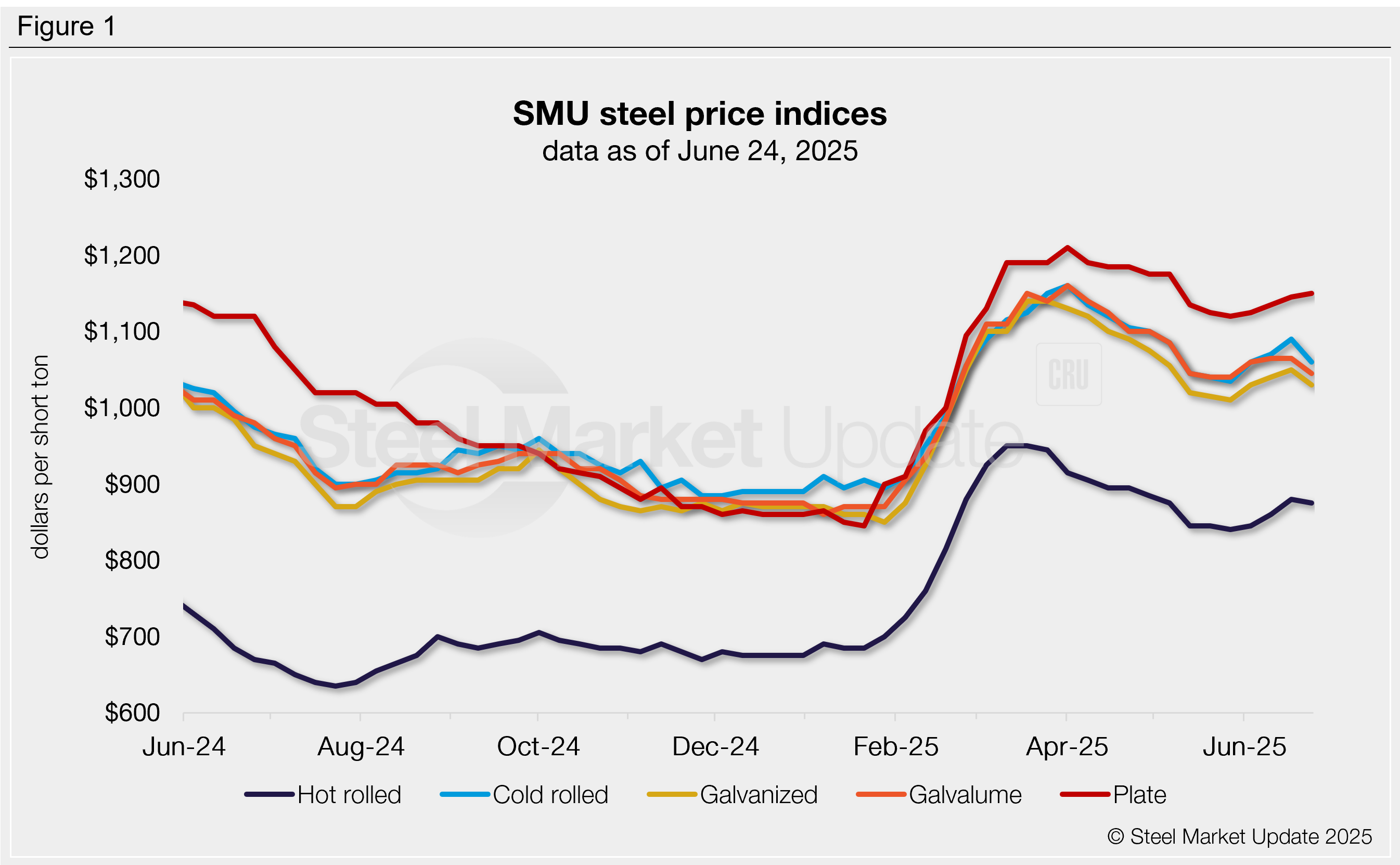

The SMU price range is $830-920/st, averaging $875/st FOB mill, east of the Rockies. The lower end of our range is unchanged w/w, while the top end is down $10/st. Our overall average is down $5/st w/w. Our price momentum indicator for hot-rolled steel has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Hot rolled lead times range from 3-6 weeks, averaging 4.7 weeks as of our June 12 market survey. We will publish updated lead times on Thursday.

Cold-rolled coil

The SMU price range is $1,020–1,100/st, averaging $1,060/st FOB mill, east of the Rockies. The lower end of our range is down $20/st w/w, while the top end is down $40/st. Our overall average is down $30/st w/w. Our price momentum indicator for cold-rolled has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Cold rolled lead times range from 5-9 weeks, averaging 6.8 weeks through our latest survey.

Galvanized coil

The SMU price range is $980–1,080/st, averaging $1,030/st FOB mill, east of the Rockies. The lower end of our range is unchanged w/w, while the top end is down $40/st. Our overall average is down $20/st w/w. Our price momentum indicator for galvanized steel has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $1,058–1,158/st, averaging $1,108/st FOB mill, east of the Rockies.

Galvanized lead times range from 4-8 weeks, averaging 6.3 weeks through our latest survey.

Galvalume coil

The SMU price range is $1,000–1,090/st, averaging $1,045/st FOB mill, east of the Rockies. The lower end of our range is down $10/st w/w, while the top end is down $30/st. Our overall average is down $20/st w/w. Our price momentum indicator for Galvalume steel has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,268–1,358/st, averaging $1,313/st FOB mill, east of the Rockies.

Galvalume lead times range from 5-7 weeks, averaging 6.3 weeks through our latest survey.

Plate

The SMU price range is $1,040–1,260/st, averaging $1,150/st FOB mill. The lower end of our range is up $10/st w/w, while the top end is unchanged. Our overall average is up $5/st w/w. Our price momentum indicator for plate has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Plate lead times range from 4-8 weeks, averaging 5.6 weeks through our latest survey.

SMU note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is also available on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

The US OCTG Manufacturers Association (USOMA) is cheering US Customs and Border Protection (CBP) for catching another Thai company illegally transshipping Chinese oil pipe to the US.

In a preliminary decision last month, CPB found that Boly Pipe Co. (also known as Baoli Steel Pipe) has transshipped Chinese OCTG to the US through Thailand to avoid paying hefty anti-dumping and countervailing duties (AD/CVDs) on Chinese pipe. The applicable AD duty rate would be the PRC-wide entity rate of 99.14% and the all-others CVD rate of an additional 27.08%.

The preliminary finding has led CBP to launch a formal EAPA (Enforce and Protect Act) investigation into two US importers, Commercial Steel Products LLC and JOL Tubular Inc.

Boly Pipe and JOL Tubular appear to be affiliates of Chinese OCTG producer Jianli, according to the allegations brought to CBP by USOMA.

Those allegations cast doubt on whether Boly Pipe actually produced any of the OCTG in its exports, according to CBP’s notice of initiation.

CBP is looking into all subject pipes imported by those companies from Jan. 14, 2024, onward.

In a related EAPA investigation earlier this year, the agency found 10 importers guilty of duty evasion for importing Chinese-origin OCTG transshipped through Thailand via two other Thai companies. It ordered the importers to backpay the duties owed.

Domestic OCTG industry responds

The domestic energy tubulars industry cheered the launch of CBP’s probe.

“USOMA commends US Customs for their commitment to investigating possible evasion of US trade laws,” said Guillermo Moreno, president of Tenaris USA and chairman of USOMA.

The members of Washington, D.C.-based USOMA represent 75% of OCTG production in the US, according to the association. Members include Tenaris USA, Vallourec North America, Borusan Pipe US, PTC Liberty Tubulars, Welded Tube US, Axis Pipe and Tube, and BENTELER Steel and Tube. Combined, the companies operate 20 facilities across 10 states, employing nearly 8,000 people.

Moreno, who became USOMA’s new chairman earlier this month, said duty evasion robs the US government of billions of dollars in revenue.

Jacky Massaglia, senior vice president of Vallourec North America and vice chairman of USOMA, concurred, further noting, “Customs’ second finding of evasion of the AD and CVD orders on Chinese OCTG through the false front of operations in Thailand demonstrates the persistent challenges US producers face, even with trade orders in place.”

He added, “Only through strong enforcement can American manufacturing and American workers truly thrive. USOMA remains committed to working closely with US Customs to identify and stop evasion wherever it occurs.”

Moreno further highlighted that the domestic OCTG stands ready to serve customers with high-quality, American-made steel products.

Why it matters

While the pipe under investigation in this case is seamless only (and not welded), it’s still important for the flat-rolled industry to be aware of the trade remedy laws that exist and be prepared to utilize them when needed.

Customs will investigate claims of duty evasion and take measures to remedy the situation if allegations are substantiated.

The Enforce and Protect Act, or EAPA, became law in 2016, setting procedures for any interested party to make a claim of duty evasion. Since its implementation, CBP has launched more than 300 investigations and identified over $1 billion in AD/CVDs owed to the US government.

And when importing steel, know who you are working with and stay informed about evolving trade rules and regulations.

Editor’s note: Steel Market Update is pleased to share this Premium content with Executive members. For information on how to upgrade to a Premium-level subscription, contact Luis Corona at luis.corona@crugroup.com.

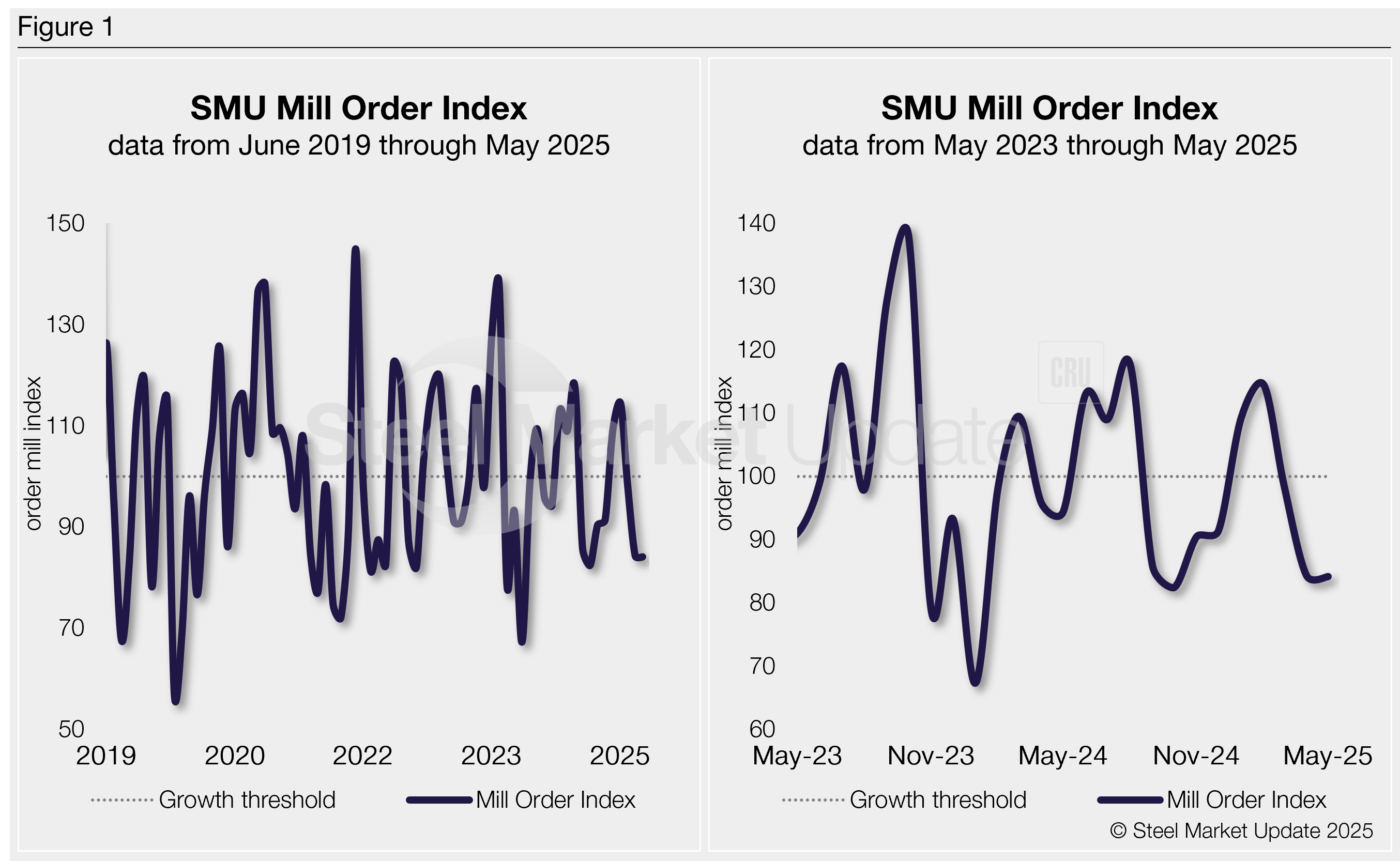

SMU’s Mill Order Index (MOI) declined for a third straight month in May, but only slightly. Still, the easing trend continued after repeated gains at the start of the year, according to our latest service center inventories data.

The decline was muted as intake inched up and new order entries edged down slightly in May. The trend is likely an indication of services centers continued efforts to right-size inventories, especially with downstream supply still stocked and a weaker demand environment.

The MOI now stands at 84.1, down just 0.2% from 84.3 in April. The result is, however, far removed from a six-month high of 114.5 in February. And it’s still the lowest reading since October.

Methodology

SMU’s MOI, which evaluates the latest change in service center mill order entries, is a relative index derived from our monthly service center inventories data. This index is a good indicator of current service center buying patterns, displaying perceived demand and lead times. This is notable given that lead times are typically a leading indicator of steel price moves.

The MOI uses a base period, presently 2022-24, to establish a reference point for measuring service centers’ mill orders over time. This base period is assigned an index value of 100. Subsequent MOI values are then calculated relative to this base.

An index score above 100 indicates an increase in buying, and a score below 100 indicates a decrease.

Figure 1 shows the nearly six-year history of the index on the left and provides a closer look at the MOI readings of the past two years on the right (100 = 2022-24 average).

Background

In the second half of 2024, large buyers capitalized on discounted prices with strategic, bottom-dollar purchases. But as demand weakened, the focus shifted sharply to inventory control.

Despite brief price spikes—driven by sudden price increases from mills— market conditions stayed soft due to sluggish end-use demand (as shown in the right-side chart in Figure 1 above).

In response, a rise in intake volume was reported for most of Q1. A boost in buying from downstream customers, pulled forward demand ahead of tariff-fueled price increases. The increase in service center orders was met with a rapid rise in mill prices.

The skinny

Weak demand across most sectors was evident, especially once the tariff-driven buying surge fizzled out. With downstream buyers largely stocked, both intake and new order entries should remain subdued. SMU’s MOI could still edge lower, but most likely will see little variation in the near-term with service centers keeping inventories in check.

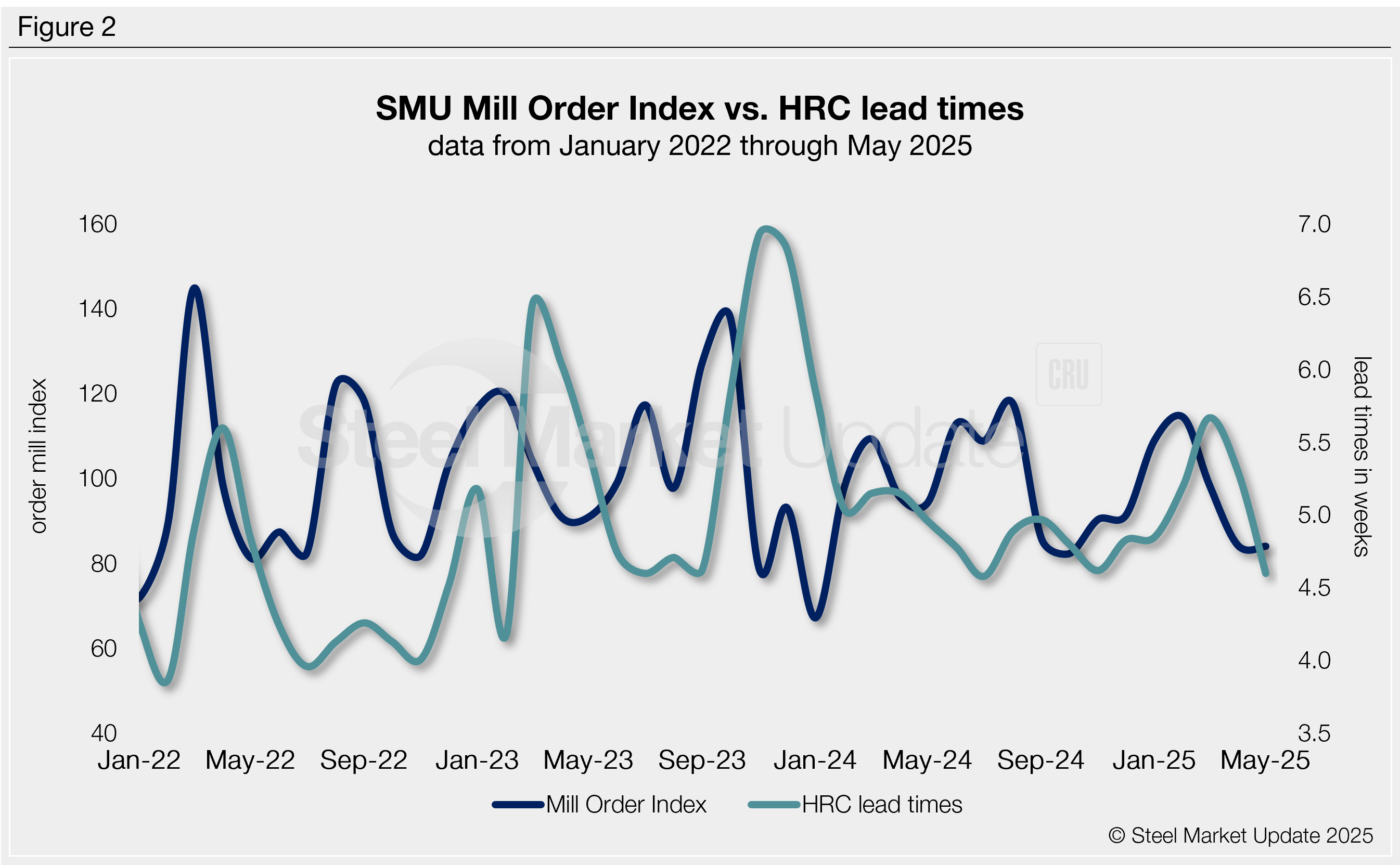

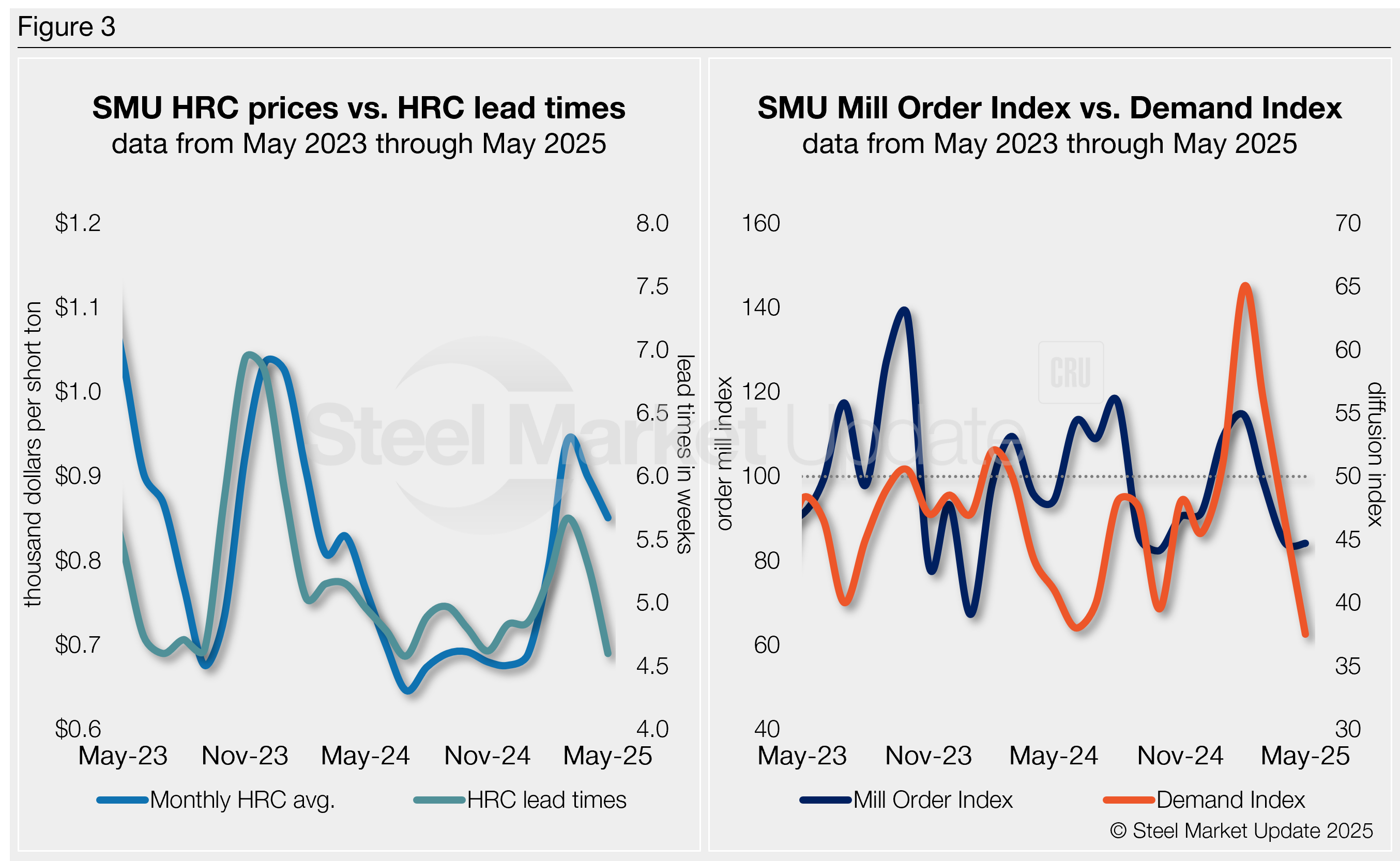

SMU’s MOI pairs well with—and has for the past five years proceeded—moves in mill lead times (Figure 2). And SMU’s lead times have also been a leading indicator of flat-rolled steel prices, particularly for HRC (see left-side chart in Figure 3).

Our MOI also pairs well with our Steel Demand Index (see right-side chart in Figure 3), which, for nearly a decade, has preceded moves in mill lead times.

Prices have turned and are now moving up again. However, this is in response to the Trump administration doubling Section 232 tariffs on imported steel to 50% on June 3.

The move stopped the recent price erosion, turning prices up $35 per short ton (st) in roughly two weeks. US hot band prices are currently $880/st, up $20/st week over week (w/w), according to our June 17 check of the market.

And lead times were out slightly again in our latest assessment on June 10. They are presently 4.6 weeks on average, up from 4.2 weeks in late May.

We clearly saw an inflection point in our most recent survey data with the announcement of doubled tariffs. And while uncertainty prevails, some early panic buying has been seen because of higher tariffs on steel.

Keep in mind, this is May service center data. While demand indications might still be pointing lower, there’s been an immediate shift. Not only are prices and lead times up, but mills stopped cutting deals. But it’s all against the backdrop of a much softer market than what we saw during a previous Section 232 buying frenzy in Q1.

With moderate demand expectations and ongoing pricing uncertainty in the domestic and import markets, service centers appear focused on cutting or maintaining inventory levels. This is especially true as the market moves closer to a historically slower summer period.

Service center shipments will need to improve, but if downstream inventories remain well stocked, a significant shift in demand will be necessary to maintain this current recovery.

Editor’s Note

Order entries, demand, lead times, and prices are based on the average data from manufacturers and steel service centers who participate in SMU’s monthly inventories and every other week market trends analysis surveys. Our demand and lead times do not predict prices but are leading indicators of overall market dynamics and potential pricing dynamics. Look to your mill rep for actual lead times and prices.

Whirlpool Corp. expects tariffs to bolster its business as it plans to invest in its US-based operations.

Whirlpool CEO Marc Bitzer, who has been vocal in supporting the tariffs, told Fox Business that the Michigan-based manufacturer stands to gain.

“We ultimately will be a net winner in the tariff environment,” Bitzer told Mornings with Maria.

Since 2020, Asian producers have exploited loopholes in 232 and 301 tariffs, the company said in its earnings guidance April 2023.

Now, Whirlpool expects “new tariff policies to level the playing field, better supporting American manufacturing,” the company said in April.

Bitzer said the company is doing a brand refresh, impacting 30% of its product line.

“With the tariffs come into place and our trust and confidence in the administration will hold firm, we will invest more in the US,” Bitzer told Fox Business. “Economically, the business case for products made in the us has become a lot more attractive.”

Bitzer said investments will be targeted at new products and at its US facilities “in automation and update of our factories, vertical integration is a big topic for us.”

However, consumers are a bit more reluctant to open their wallets amid higher inventories and lower sentiment.

In the company’s Q1’25 earnings call in April, Whirlpool said Asian appliances significantly increased ahead of tariffs, which will disrupt the market through the second quarter as competitors sell through inventory.

Bitzer told analysts on the April earnings call the company is focusing on what it can control.

“We’re not counting on a massive improvement of consumer behavior or consumer landscape. We guided earlier, in particular for North America, essentially pretty much for a flat market environment,” Bitzer said.

“So we’re not counting on dramatic improvement of macro-environment,” Bitzer said in April. “But what we are counting on is on the things which are in our control; the cost take out, the pricing actions which we’ve taken and the new product introduction.”

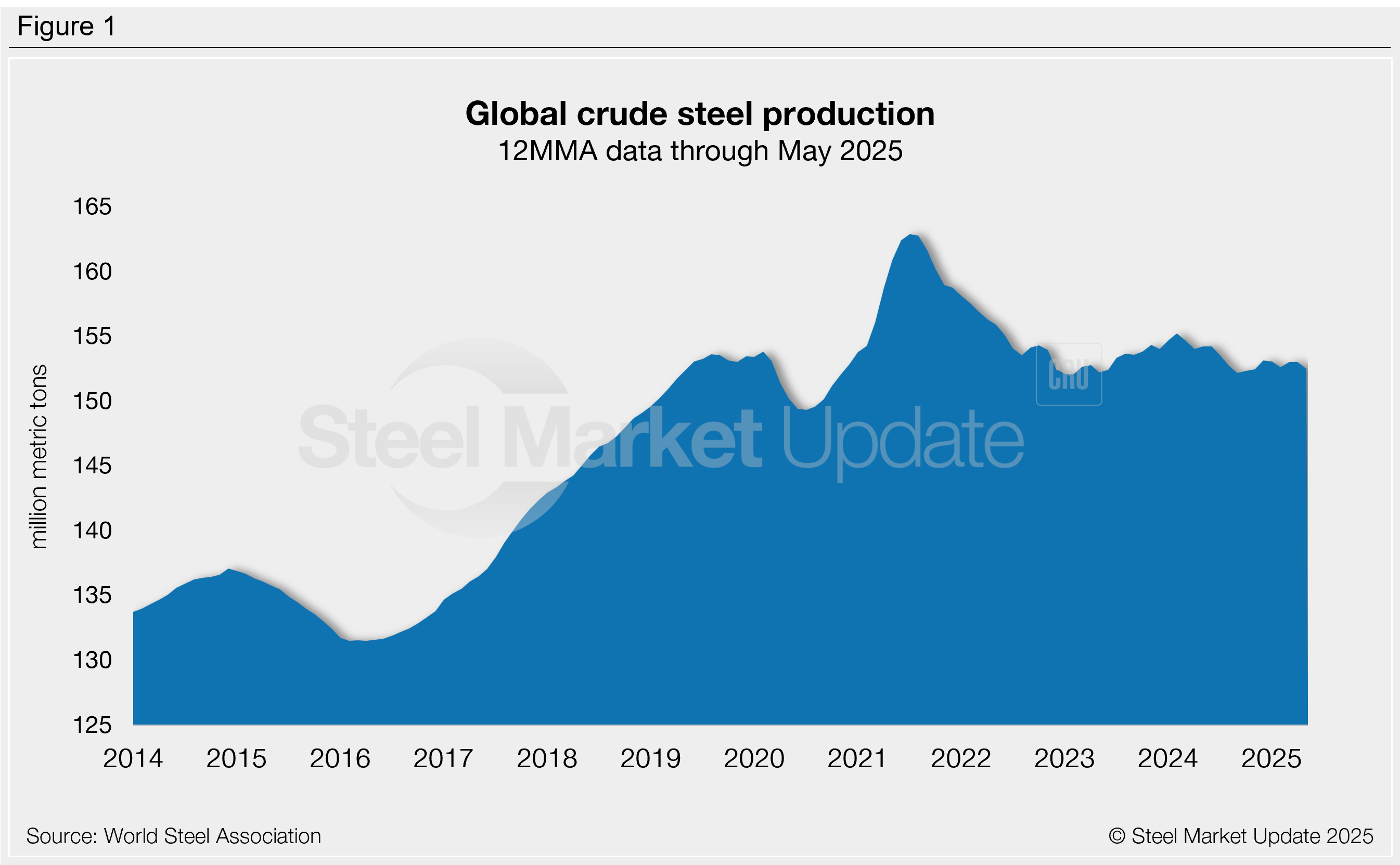

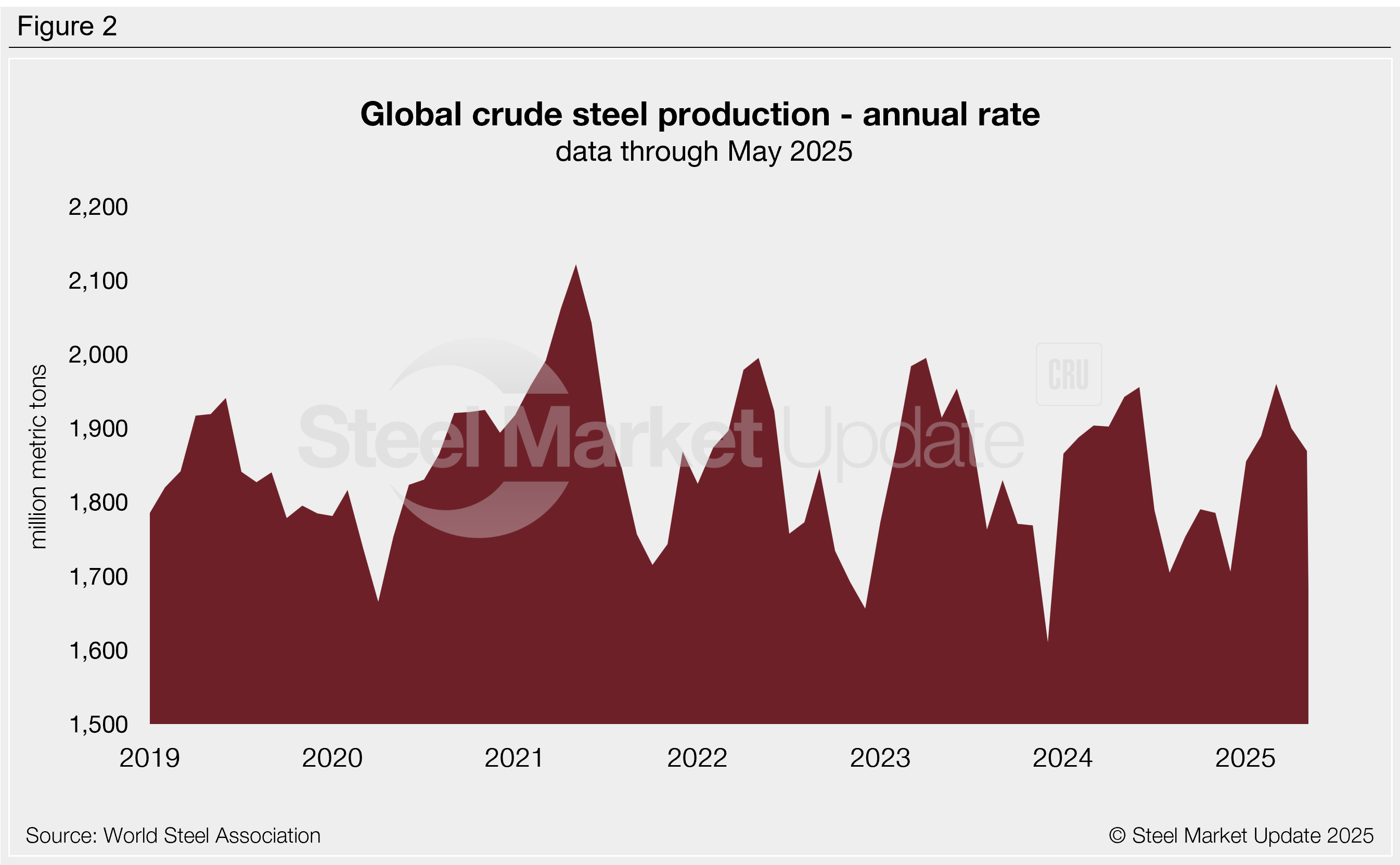

Global raw steel production rose 2% from April to May, slightly above average production levels seen in recent months, according to data recently released by the World Steel Association (worldsteel).

Worldwide steel output reached an estimated 158.8 million metric tons (mt) in May. While modestly higher than the previous month, production was 5% lower than March’s (adjusted) two-year high of 166.5 million mt and 4% lower than year-ago levels.

On a 12-month moving average (12MMA) basis, global production has averaged 152.5 million mt per month over the past year (Figure 1). May output was 4% above this rate. Annual mill output has generally remained in the range of 152 million mt to 154 million mt for nearly three years now, similar to pre-pandemic levels.

Steel mill production worldwide averaged 5.12 million mt per day in May, down 2% month over month (m/m) and 4% below the same period last year. In 2024, daily production peaked at 5.35 million mt in June and bottomed out at 4.67 million mt in August. So far in 2025, daily output has ranged from 5.08 million mt to 5.37 million mt. At May’s pace, annualized global production would total approximately 1.87 billion mt (Figure 2).

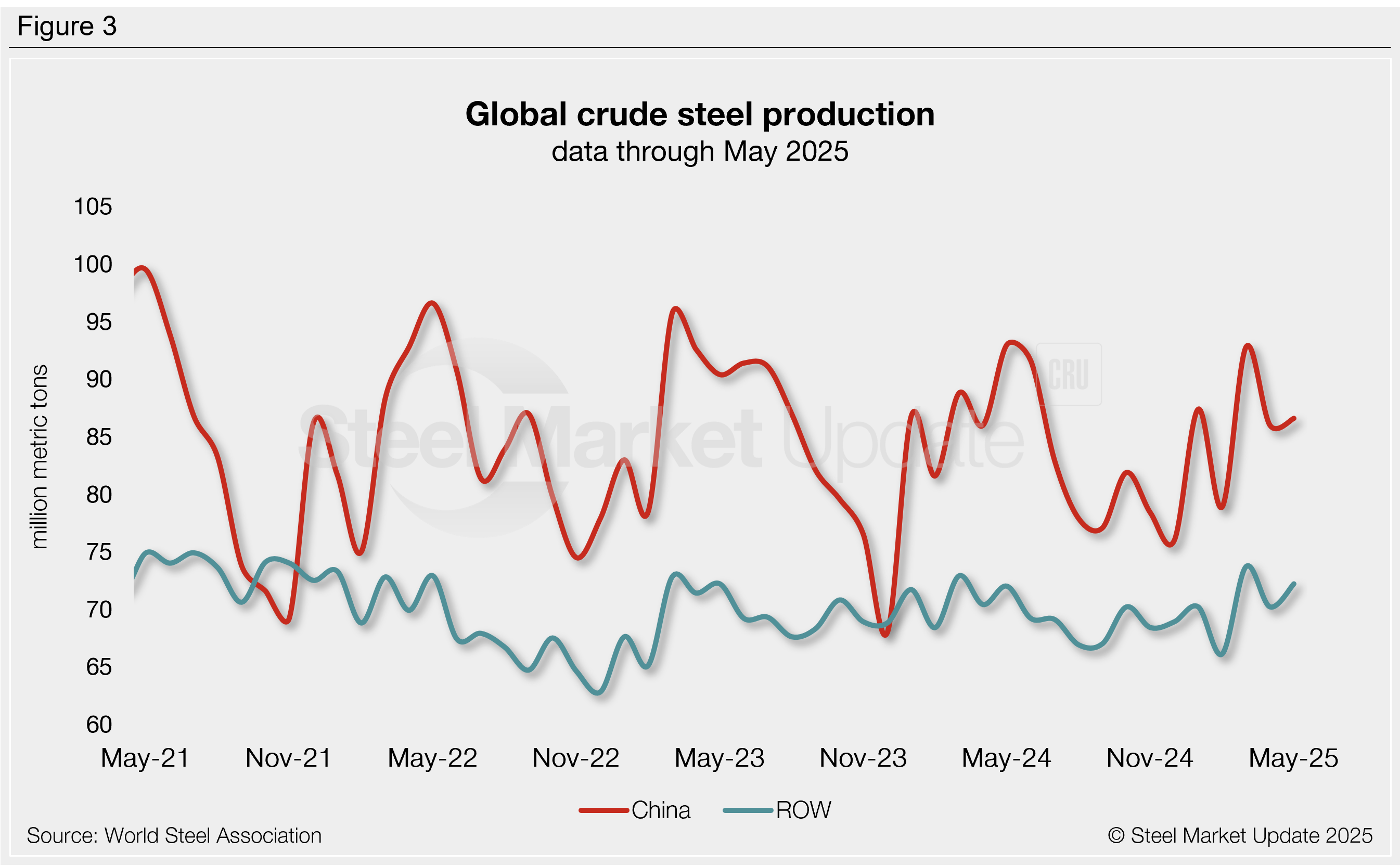

Regional breakdown

China is the world’s leading steel producer, accounting for 55% of the global output in May (Figure 3). Chinese production increased 1% m/m in May to 86.6 million mt but was down 7% from a year earlier. In 2024, mill output in China averaged 83.5 million mt per month, peaking in May at 93.0 million mt. Over the past three years, Chinese mills have consistently accounted for 50-57% of total global production.

Steel output from the rest of the world (ROW) totaled 72.2 million mt in May, up 3% from the previous month and in line with May 2024 volumes. ROW production averaged 69.6 million mt per month throughout 2024, peaking in March at 72.9 million mt.

Top producing countries

Looking at production by country, India retained its position as the second-largest steel producer in May, producing 13.5 million mt or 9% of the global total. Next up was the United States (7.0 million mt or 4%), followed by Japan (6.8 million mt or 4%), Russia (estimated at 5.8 million mt or 4%), South Korea (5.1 million mt or 3%), Iran (3.4 million mt or 2%), Turkey (3.1 million mt or 2%), Germany (3.0 million mt or 2%), and Brazil (2.7 million mt or 2%).

Comparing year-to-date (YTD) output for each of these countries to the same period of last year shows some modest shifts in market share. German mills produced 11% less steel in the first five months of 2025 than they did in the same time period in 2024. Production in India increased by 8% during the same period. Other notable shifts in YTD production were evident in Iran (-5%), Japan (-5%), and Russia (-5%).

Nucor has given an update on the cybersecurity attack that took place in May, noting it has had no “material impact” on the company.

Recall that last month the Charlotte, N.C.-based steelmaker reported a breach of its IT systems. Operations were halted at some facilities, though the company did not specify which facilities were affected.

“We are reviewing and evaluating the impacted data and will carry out any appropriate notifications to potentially affected parties and to regulatory agencies as required by applicable law,” a Nucor spokesperson told SMU on Monday.

“The cybersecurity incident has not had a material impact and is not reasonably likely to have a material impact, on our business operations or financial condition or results of operations,” the spokesperson added.

This was also detailed in a Form 8-K/A with the US Securities and Exchange Commission filed on June 20.

Update

As an update, Nucor said in the filing the “affected production operations, and access to necessary affected information technology applications, have been restored.”

Also, the company believes the “threat actor” no longer has access to its information technology systems.

Nucor has worked with outside cybersecurity experts “to further reinforce its information technology systems and to prevent future unauthorized access.”

The spokesperson told SMU: “We want to thank our customers, partners, and teammates for their continued support, cooperation, and patience as we resolved this matter.”

Background

In the filing, Nucor said its investigation revealed a “a threat actor illegally accessed the company’s information technology systems.”

The company again noted it “temporarily and proactively halted certain production operations at various locations,” though no further information was given on location.

Nucor added that the threat actor “exfiltrated limited data from the company’s information technology systems.”

Following the incident, Nucor said it activated its incident response plan.

This included “proactively taking potentially affected systems offline, restoring affected data from backup systems, and implementing other containment, remediation, and recovery measures.”

Cheap steel produced in the Association of Southeast Asian Nations (ASEAN) and China continues to flood Latin America (LATAM), threatening its steelmakers, according to a new study.

A collaborative study conducted by the Organization for Economic Co-operation and Development (OECD), the Latin American Steel Association (Alacero), and the National Chamber of the Iron and Steel Industry of Mexico (Canacero) warns the region that protective measures are critical to the livelihood of its producers.

Subsidies and overcapacity

Global overcapacity threatens small and mid-sized LATAM steel producers, the report warned. By 2027, the projected amount of steel overcapacity is expected to reach 721 million metric tons (mt).

In the next two years, it’s projected that China will add 47.3 million mt, India will add 30.4 million mt, and ASEAN will contribute 14.8 million mt.

The report highlights the role that direct and indirect government subsidies play in amping up China and ASEAN steel production: Through subsidized loans, land grants, state-directed mergers and acquisitions, below-market-priced raw materials and utilities, and tax relief for recruiting employees, the Chinese government supports market-distorting steel production. China’s domestic market demand doesn’t match its production levels, the report said.

Since 2021, Chinese investments in ASEAN steelmaking created ~10 million mt of steel capacity. Ninety-six percent of the capacity added to the ASEAN market comes from subsidies. Thailand added 2 million mt capacity, Malaysia’s capacity has also increased 2 million mt, and Indonesia’s capacity tripled to 6 million mt.

Protecting LATAM’s steel producers

Steel advocates say that the region must swiftly implement efforts to protect itself. The recommendation is that the countries in the region align strategically to thwart trade threats from China and ASEAN nations. The report unequivocally calls for implementing industrial policies across the region, promoting regional value chains, and strengthening its trade defense tools.

Finished and semi-finished steel imports to LATAM from China swelled by 233% from 2010 to 2024, the report stated. And in 2024, 39% of the steel consumed in LATAM was imported. The region’s manufacturing GDP declined by four percentage points over 25 years, with Chile, Brazil, and Argentina most affected.

CMC

Third quarter ended May 31

2025

2024

Change

Net sales

$2,020.0

$2,078.5

-2.8%

Net income (loss)

$83.1

$119.4

-30.4%

Per diluted share

$0.73

$1.02

-28.4%

Full year ended Aug. 31

Net sales

$5,684.0

$5,929.8

-4.1%

Net income (loss)

$(67.1)

$381.6

-118%

Per diluted share

$(0.59)

$3.25

-118%

(in millions of dollars except per share)

CMC entered the back half of its fiscal year with improving steel margins, steady rebar demand, and confidence in long-term construction fundamentals. Executives said infrastructure activity and downstream momentum are helping to offset macroeconomic uncertainty as the company pushes forward on multiple growth projects.

For its fiscal third quarter ended May 31, the Irving, Texas-based longs producer and metal recycler reported net earnings of $83.1 million on sales that exceeded $2 billion. While the quarterly results were below those of last year (see chart above), they showed significant improvement from a weak second-quarter performance.

“We believe that the second quarter of fiscal 2025 marked a trough, and expect business conditions for each segment will continue to improve from those levels,” CEO Peter Matt said on the company’s earnings call Monday morning.

He highlighted the margin improvement on steel products throughout the quarter, as average selling prices rose $45/short ton (st), outpacing the $22/st increase in scrap costs. Steel product metal margins exited the quarter at $518/st, $19 above the quarterly average.

“We see improving volume and margin conditions ahead as we move through the 2025 construction season,” added CFO Paul Lawrence.

Market and tariff uncertainty

Matt addressed the current uncertainty in the markets.

“There’s little doubt that the impact of economic uncertainty and elevated interest rates are hanging over our markets,” he commented on the call. “But I would note two things. One, tariffs are just the latest flavor of uncertainty that the industry has had to manage through. And two, we have been living in a high interest rate environment for more than two and a half years.”

On the supply side, he said CMC is benefiting from the tariffs: The elimination of Section 232 exemptions and the hiking of the levy to 50% have reduced import levels. “While we do not know how long these policies will remain in effect, they should support steel pricing for their duration,” he noted.

As for demand, he acknowledged the near-term uncertainty the tariffs are causing. But he believes they have the longer-term potential to be “a single component of a broader program that includes changes to tax, regulatory, energy, and trade policy aimed at stimulating domestic investment, which could meaningfully benefit construction activity.”

“We expect powerful tailwinds from long-term secular trends that will drive construction investment for years to come,” he said, mentioning “infrastructure investment, reshoring, artificial intelligence, energy transition and generation growth, and the need to address our nation’s housing shortage.”

North America results

CMC’s North America Steel Group posted adjusted EBITDA of $186 million in fiscal Q3, down 24% from last year but up 44% from the prior quarter.

“Despite concerns regarding tariffs and related economic uncertainty, we experienced an encouraging degree of stability across each of our key internal leading indicators,” including project bids, new awards, and backlog volumes, Matt said.

CMC’s rebar shipments in North America increased 6.2% sequentially and 2.7% year over year to 534,000 st.

Merchant bar (MBQ) shipments of 264,000 st rose 8.2% from a year earlier, as the Arizona 2 micro mill has enhanced CMC’s ability to serve customers on the West Coast, the company said.

Raw material shipments to external customers improved 23.4% sequentially and 6.9% year over year (y/y).

Matt said the company faced some challenges from mill outages late in the quarter that resulted in lower-than-expected production.

West Virginia micro mill update

CMC confirmed it expects to begin hot commissioning the melt shop at its West Virginia micro mill in early 2026.

An anticipated $80-million tax credit under the Inflation Reduction Act (IRA) contributed to a pause in construction while contract compliance was reviewed.

“It was worth waiting for this,” Matt commented. “It reduces the net capital that we put into the project and therefore helps us drive higher returns.”

Europe returns to profitability

“Market conditions for the Europe Steel Group continued to improve in the third quarter, supported by solid Polish economic conditions and reduced import flows that helped establish a better balance of supply and demand,” CMC said.

The segment posted adjusted EBITDA of $3.6 million, up from a loss of $4.2 million in the same quarter last year. Stronger pricing, improved shipment volumes, and ongoing cost controls helped to boost the results.

“The picture in Europe does appear to be getting better,” Matt commented. “There are reasons for optimism.”

Expansion on the horizon

CMC said the company’s strategic focus remains on both organic expansion and targeted acquisitions to continue growing the business.

On the organic side, Matt highlighted investments in downstream capacity, automation, and efficiency. This includes continuing to scale up the Arizona 2 mill, which reached 70-75% capacity utilization during the quarter.

As for inorganic growth, CMC is targeting opportunities in adjacent construction markets that also have geographical overlap with its existing operations. The ideal transaction size is $500 million to $750 million.

“We’re very disciplined,” Matt added. “We look for bolt-on deals that enhance our capabilities in our core markets or help us enter adjacent markets that align with our business model.”

CMC is currently evaluating several potential opportunities, primarily in the early-stage construction market. However, market uncertainty is slowing some processes, the company said.

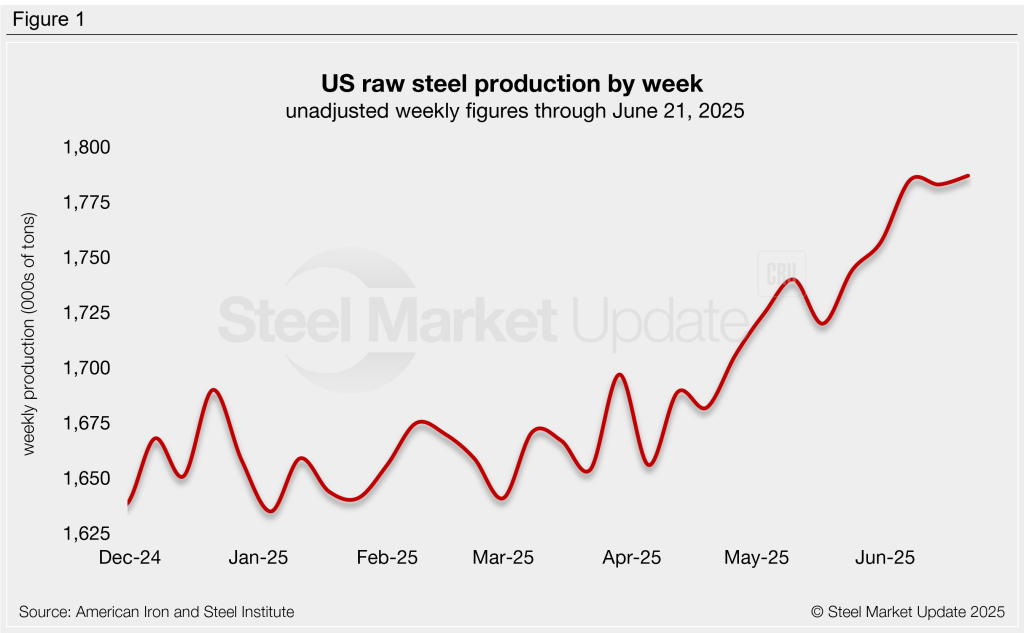

Following a minor dip in mid-June, raw steel production rose last week to a new multi-year high, according to the latest data released by the American Iron and Steel Institute (AISI). US mills have ramped up production since April, with weekly output steadily increasing in nearly every week since.

Domestic steel mills produced an estimated 1,787,000 short tons (st) of raw steel through the week ending June 21 (Figure 1). Output grew by 4,000 tons, or 0.2%, compared to the prior week, now at the highest unadjusted weekly figure recorded since May 2022.

Last week’s production was 5.5% above the year-to-date (YTD) average of 1,694,000 st per week and 4.9% higher than the same week the previous year.

The mill capability utilization rate was 79.6% last week, up from both the prior week (79.4%) and one year ago (76.7%).

YTD production now stands at 41,642,000 st with a capability utilization rate of 75.8%. Mills have produced 0.2% more steel this year than the same period of 2024. Before June, steel output in 2025 had been running behind 2024 levels.

Raw production increased week over week (w/w) in three of the five AISI-defined regions:

Northeast – 120,000 st (down 9,000 st w/w)

Great Lakes – 564,000 st (up 8,000 st)

Midwest – 248,000 st (down 5,000 st)

South – 786,000 st (up 6,000 st)

West – 69,000 st (up 4,000 st)

Editor’s note: The raw steel production tonnage provided in this report is estimated and should be used primarily to assess production trends. The graphic included in this report shows unadjusted weekly data. The monthly AISI “AIS 7” report is available by subscription and provides a more detailed summary of domestic steel production.

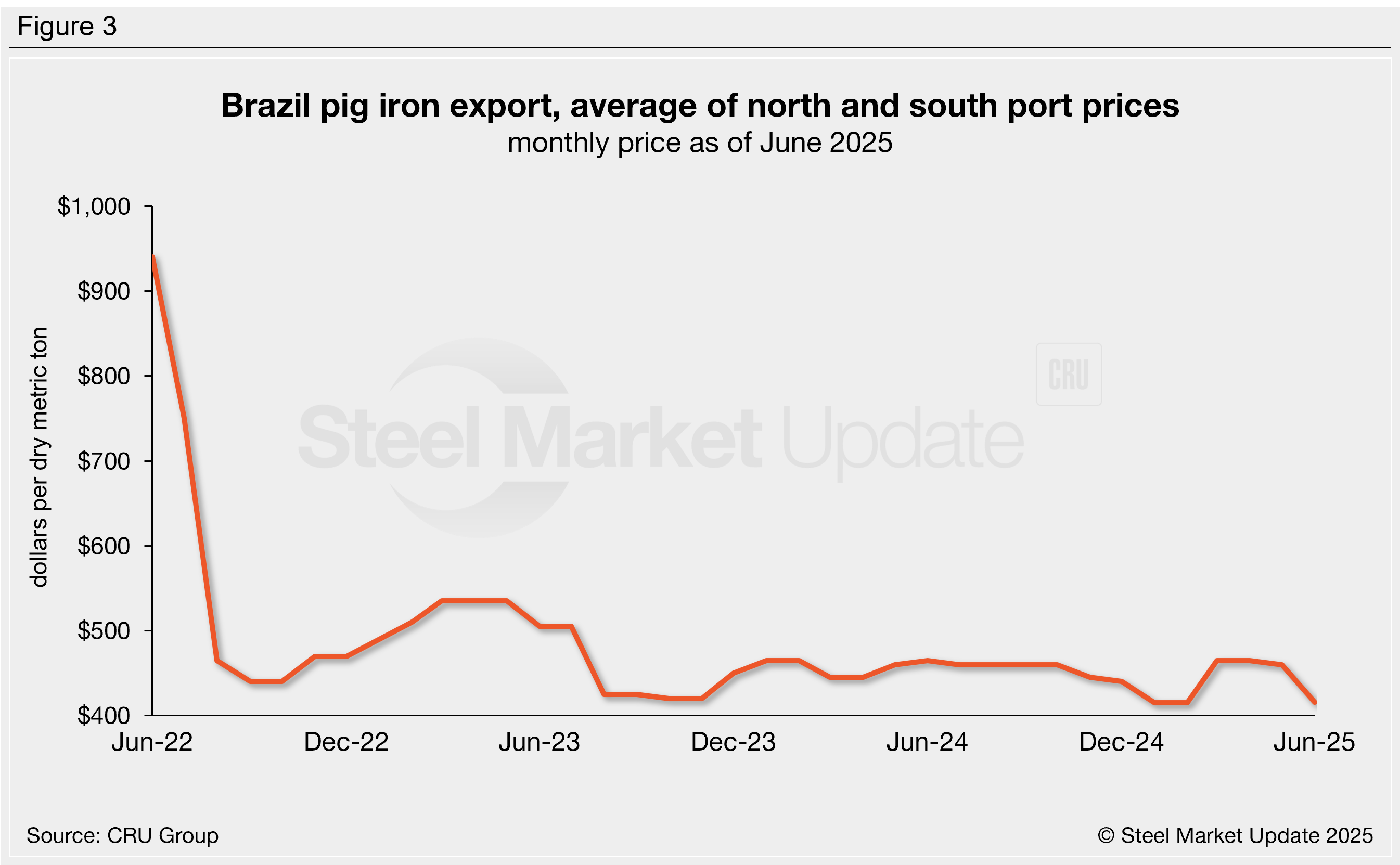

The resistance Brazilian pig iron sellers had shown to accepting lower prices has proved short-lived, sources told SMU.

Earlier this month, we reported a sale of pig iron was concluded from south Brazil at a price of $401 per metric ton (mt) FOB ($430/mt CFR US port). We also heard from a source in Brazil several other potential sellers had reservations about accepting this lower price level.

Our recent information is indicating this resistance didn’t last long. A large channel did sell a cargo to an American consumer two weeks at a price of $396/mt FOB, which was still lower than the previous sale. Both of these transactions were higher Phos (P .15% max) material.

SMU has learned there has been a cargo sold to the US from northern Brazil at an unconfirmed price of $450/mt CFR. The northern Brazilian cargo was a lower Phos (P .10% max) cargo. This is theoretically a $10/mt increase.

So, what is the feeling on the part of Brazilian producers as we head into July for shipment in August?

SMU contacted two sources in Brazil to get a glimpse of their expectations. One executive for a large seller said the market has been quiet in south Brazil for the last two weeks. He is expecting the next round of sales to the US will be higher. They should start negotiations soon.

The second source said the producers are hoping the US scrap market will improve. This would result in a higher price for August pig iron sales. However, a rise in the US scrap market in July a quite speculative at this point.

The US has been receiving pig iron from Ukraine on a regular basis in 2025. This is all lower Phos (P .10% max) material. As previously reported by SMU, April export records show 115,000 mt of pig iron were sent to the US. This brought Ukrainian pig iron exports to the US to 476,000 mt in January through April.

The May and June statistics have not been released, but it is a safe assumption that shipments to the US have been ongoing. SMU will publish the quantities once they are available.

Nucor kept its weekly list price for hot-rolled (HR) coil flat this week following two consecutive increases.

This leaves the Charlotte, N.C.-based steelmaker’s consumer spot price (CSP) for HR coil at $900 per short ton (st) as of Monday.

The price at the company’s West Coast joint venture, California Steel Industries (CSI), will also remain the same at $960/st.

The steelmaker last held prices flat on June 2, when the CSP for HR stood at $870/st, before raising it over the last two weeks.

Nucor said lead times for all spot orders will be offered between 3-5 weeks.

Recall that Cleveland-Cliffs last week raised its monthly HR price by $40/st and is now seeking $950/st.

Note Cliffs publishes its listed HR prices on a monthly basis, whereas Nucor updates them on a weekly basis.

SMU’s average HR price was $880/st FOB mill, east of the Rockies, as of June 17. That was up $20/st week over week.

We will next update prices on Tuesday evening.

We’ve gotten used to weekend surprises from the Trump administration. And the latest one, which had nothing to do with tariffs, is the biggest yet – US forces bombing Iran.

It is above my paygrade to guess what comes next. Folks far more knowledgeable than me about geopolitics and oil markets are already speculating about what’s in store.

What matters to SMU is what it means for the North American steel market, ferrous supply chains, and flat-rolled steel prices.

Feldstein’s crystal ball

David Feldstein, president of Rock Trading Advisors, pointed out in a column on Thursday that oil, diesel, and gasoline futures had already seen a sudden spike on the widening Israel-Iran conflict. Futures for agricultural commodities had also rallied.

That all happened before the US strike on Iran’s nuclear facilities over the weekend. Basically, Feldstein’s column turned out to be prescient. It’s linked here and worth a read if you haven’t read it yet.

There is an old saying in steel that oil, coil, and scrap trend together. As of last week, steel prices continued to tick higher on Section 232 tariffs doubling to 50%. And ferrous scrap appeared headed for a “strong sideways” settlement in July.

Those developments had little to do with the Middle East. But one indicator was already flashing red: freight rates were moving higher in part because of higher fuel costs stemming from the fighting between Israel and Iran.

Steel didn’t see this coming

As best as I could tell from our survey data and from speaking to some of you, not many people in the North American steel market had direct US involvement in a Middle East conflict on their bingo card. Most of the talk was about so-so demand and the summer doldrums limiting the upside on prices. Sure, Section 232 tariffs doubling to 50% had made their mark. But the potential trade deals with traditional US allies such as Canada and Mexico had blunted their impact.

Yes, prices were going up. Albeit not as quickly as people expected after Trump first announced the 50% tariffs in late May. Sure, lead times had stretched out on some increased buying and as some import volumes shifted to domestic mills. But increased domestic capacity and uneven demand would keep a lid on prices and lead times – unless something unexpected happened.

What if oil hits $100/barrel?

That unexpected something has now happened. And there is talk of oil hitting $100 per barrel. The last time that happened was when Russia launched its full-scale invasion of Ukraine in February 2022. We all know what happened then. Steel prices had been falling in early 2022 after supply overshot demand in late 2021. But the market abruptly shifted higher on Russia’s invasion.

Case in point: Hot-rolled coil prices stood at $1,020 per short ton on average on Feb. 22, just two days before Russia’s invasion. HR prices then spiked to $1,480/st by mid/late April. HR lead times, which averaged 3.8 weeks at the beginning of 2022, stretched out to nearly six weeks by late March. (Editor’s note: SMU’s interactive pricing tool allows you to visualize HR prices, scrap prices, and HR lead times in the same chart.)

For steel, there were fears that EAF mills would not be able to get enough pig iron. That fear stemmed from Brazil, Ukraine, and Russia each accounting for approximately one-third of global pig iron supplies. And two-thirds of that volume had suddenly been called into question. Price doesn’t matter as much as securing material in times of real or perceived scarcity.

Over time, mills found ways to stretch their scrap supplies. Brazil was able to fill much of the void left by Russia. And the panic buying across the ferrous supply chain in February and March 2022 led to a 2H glut. (I remember visiting some mills that were still sitting on mountains of pig iron into Q4 2022.)

I’m not highlighting the Russia-Ukraine war because I think we’re going to see a repeat of 2022. It’s too early to say whether or not the Iran conflict and its impact will remain “contained” within the region. I note it because it’s arguably the most recent precedent we have. And, as American author Mark Twain said (or might have said), “History never repeats itself, but if does often rhyme.”

One thing is certain: more uncertainty

Let’s assume oil goes significantly higher and the rig count, which has been drifting lower, suddenly whipsaws higher. That would increase demand for oil country tubular goods (OCTG) and for the coil used to make them.

Maybe higher agriculture prices could spur demand in a US ag market that relies heavily on exports and that to date has been hurt by tariffs? And perhaps steel consumers who have been buying hand-to-mouth might finally stock up on the prospect of a sustained period of higher steel prices?

But there are also some factors that could keep prices in check. The domestic steel market has been grappling with tariff-related uncertainty since “Liberation Day” in early April. That uncertainty has kept many buyers on the sidelines. Now there is war/geopolitical uncertainty on top of trade-policy uncertainty. Why would that give steel consumers more confidence to go out and buy?

If there is a saving grace, it’s that the US has a vibrant domestic oil and gas industry. We’ve been a net annual energy exporter since 2019 and exported the most on record in 2023, according to the US Energy Information Administration. That sure helps to hedge against any oil-market shocks stemming from events abroad. (Europe, which relies heavily on imported energy, has not been so lucky. But I digress.)

A lot depends on what happens in the days ahead. I wish I could fast-forward to a week or a month from now and tell you what comes next. For now we’re just going to have to brace for yet more volatility.

Aluminum Market Update

Steel Market Update has been closely following tariff developments and what they mean for the steel market. And we’ll keep you apprised of what rapidly escalating tensions in the Middle East might mean for your business.

Our new sister publication, Aluminum Market Update (AMU), will do the same for aluminum and nonferrous scrap. AMU has plenty of insightful articles on everything from tariffs and trade to the rise of AI and what it means for energy – and for energy-intensive businesses like primary aluminum.

Check out the latest by signing up for a free 30-day trial here. And if you like what you see, please consider a subscription.

Until next time, thanks to all of you for your continued business. We really do appreciate it.

Ken Simonson, chief economist for The Associated General Contractors of America (AGC), will be the featured speaker on the next SMU Community Chat webinar on Wednesday, June 25, at 11 a.m. ET.

The live webinar is free. A recording will be available free to SMU members. You can register here.

We’ll have a lot to talk about because construction is at the intersection of so many of today’s hot-button issues. The main question: Will construction thrive or dive in the rest of ’25? (Nothing wrong with a rhyme, even in serious times.)

To answer that, Simonson will discuss the effect of tariffs on costs for steel and other building materials. He’ll also explore the impact of the Trump administration’s immigration crackdown on a construction workforce that relies heavily on immigrant labor. (Did you know that more than 60% of drywall installers and more than 50% of roofers were born abroad?)

Then there is the matter of interest rates. Builders might want to see the Federal Reserve lower rates before they unleash new projects. But the Fed, leery of potential tariff-related inflation, might not have much leeway to cut rates. What gives?

We’ll analyze it all through the lens of the latest data. Among the highlights: changes in construction spending by category, construction employment nationally and by state, and materials costs.

Why should you listen?

Because the construction sector matters to your business. And because AGC is the leading association for the US construction industry, with more than 27,000 member firms across a range of markets. Also, Simonson has been chief economist at AGC since 2001, so he has seen more than a few construction cycles.

As always, we’ll keep it to about 45 minutes. You can drop in, learn something – and then get on with your day. We’ll take your questions too. So remember to think of some good ones for the Q&A.

Editor’s note

If you’d like to see past Community Chat webinars, you can find those here. I suggest checking out a couple of good ones that we’ve recorded over the last month with two of our most popular guest speakers: Barry Zekelman, CEO and executive chairman of Zekelman Industries, and Timna Tanners, managing director at Wolfe Research.

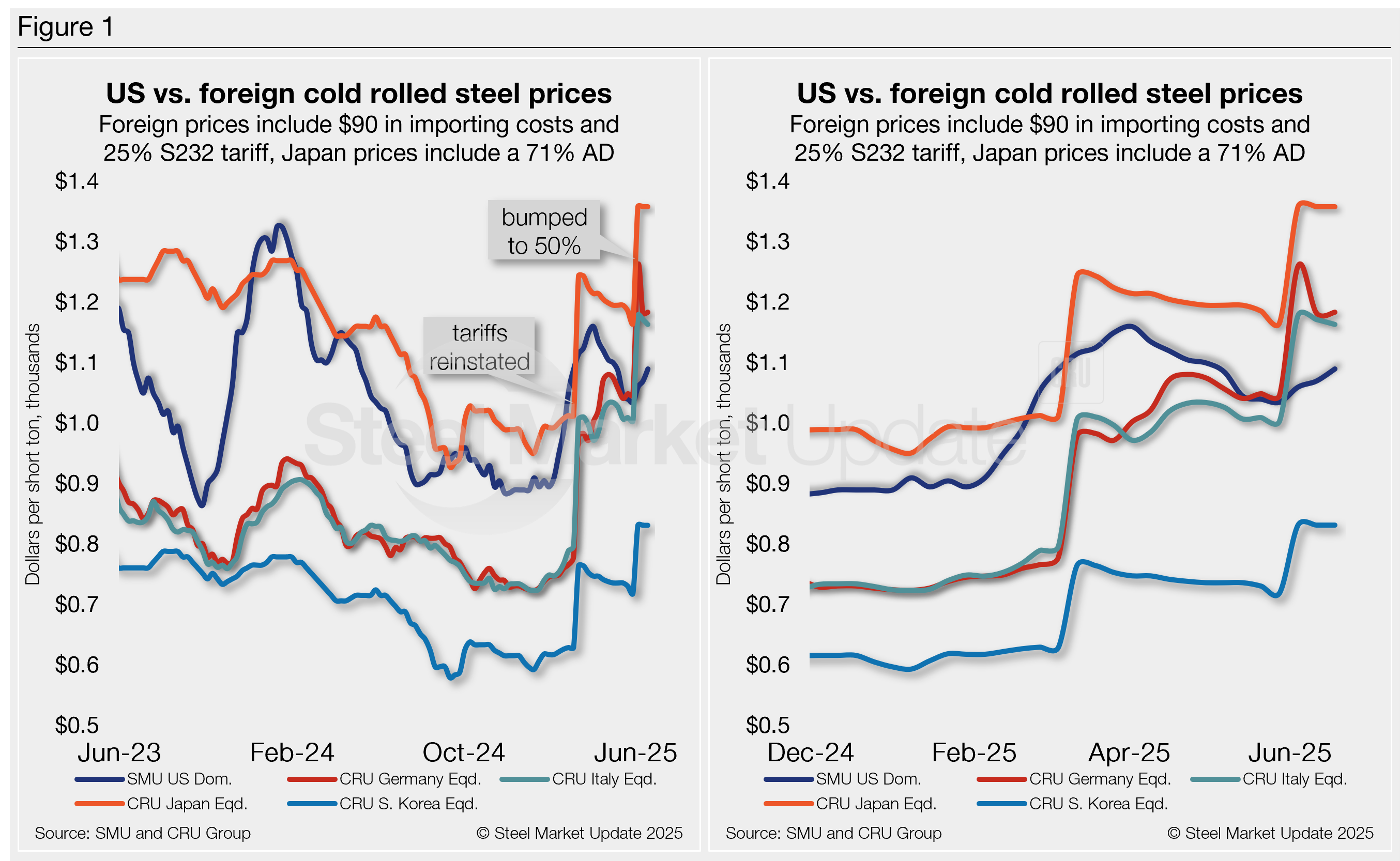

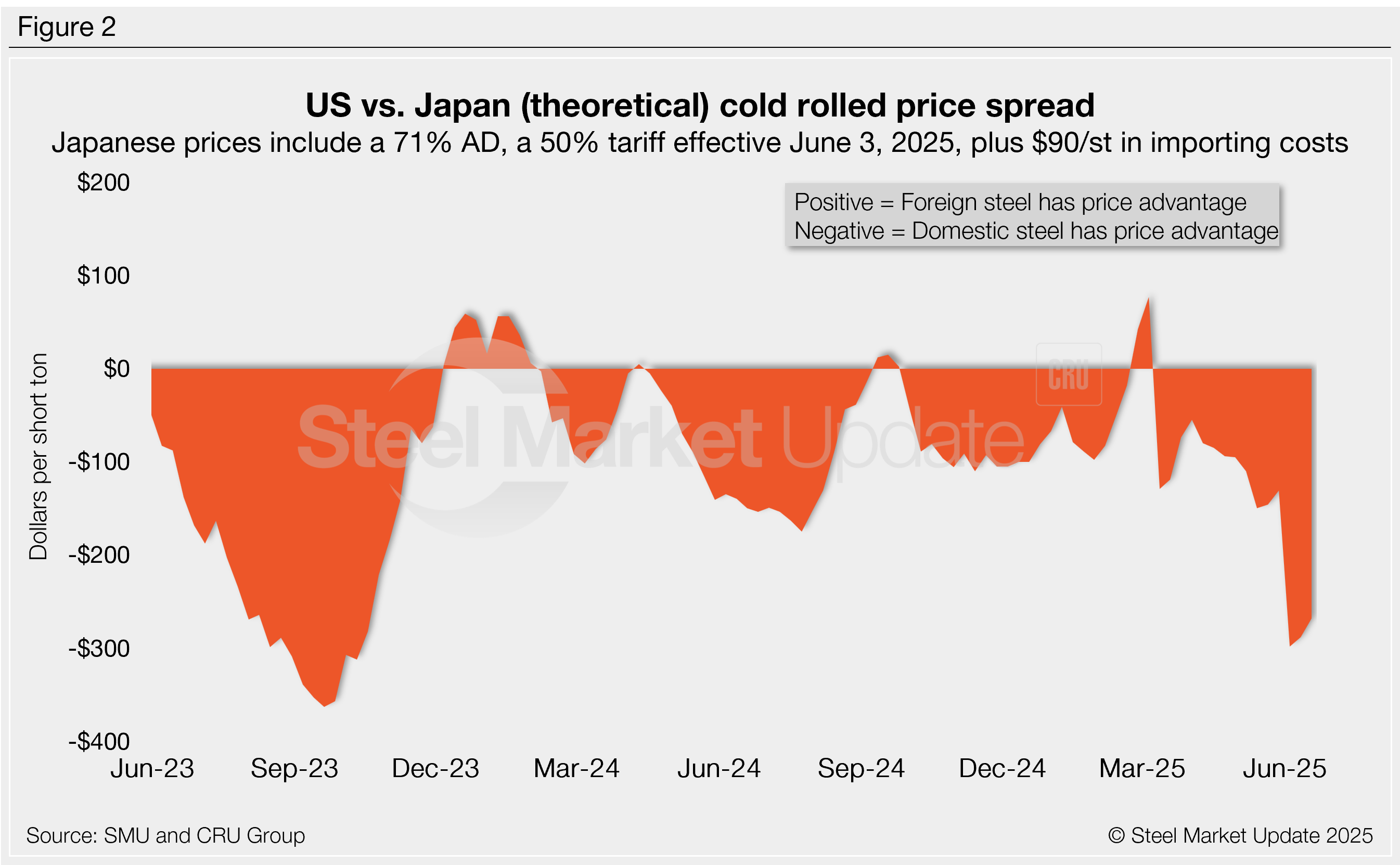

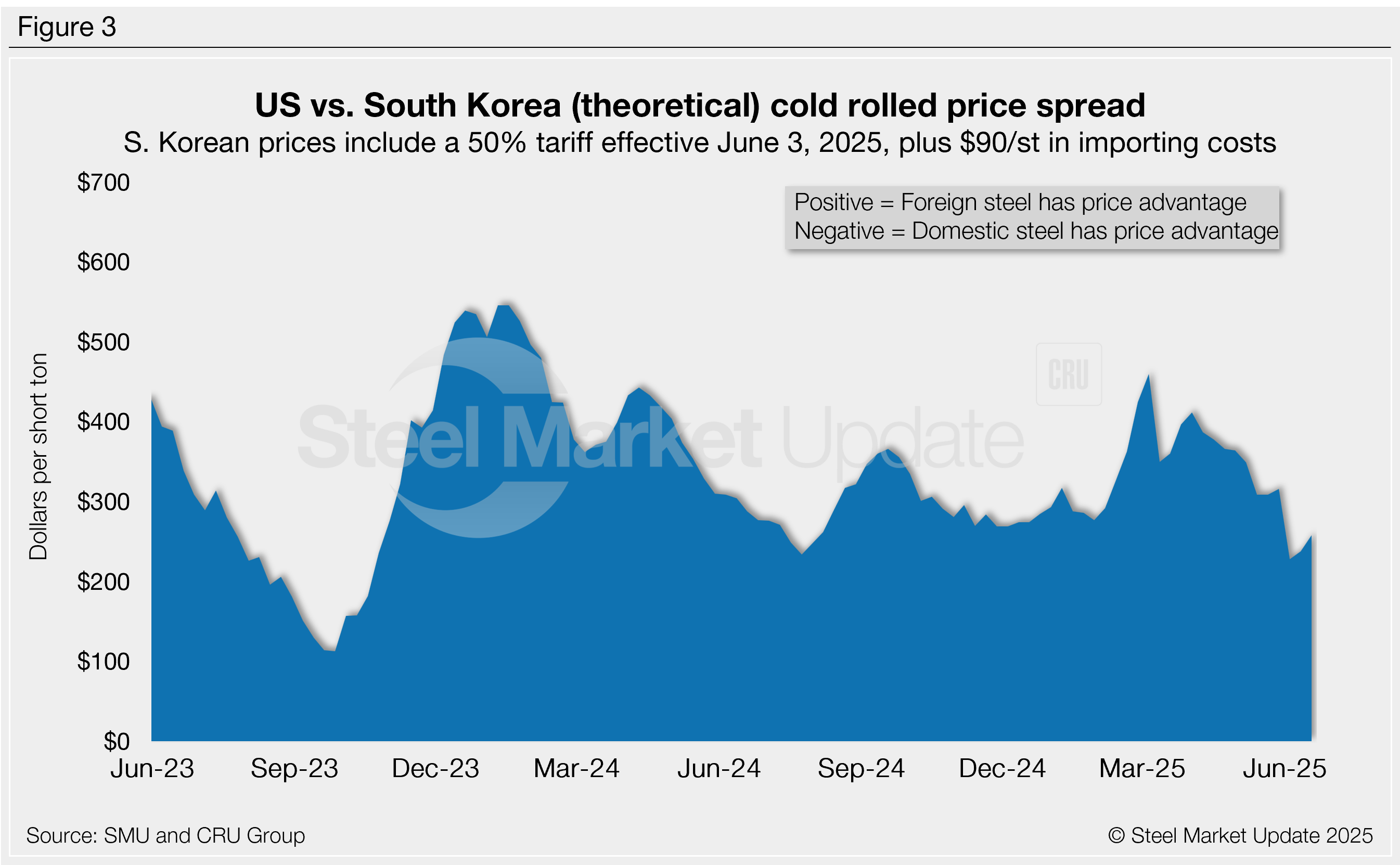

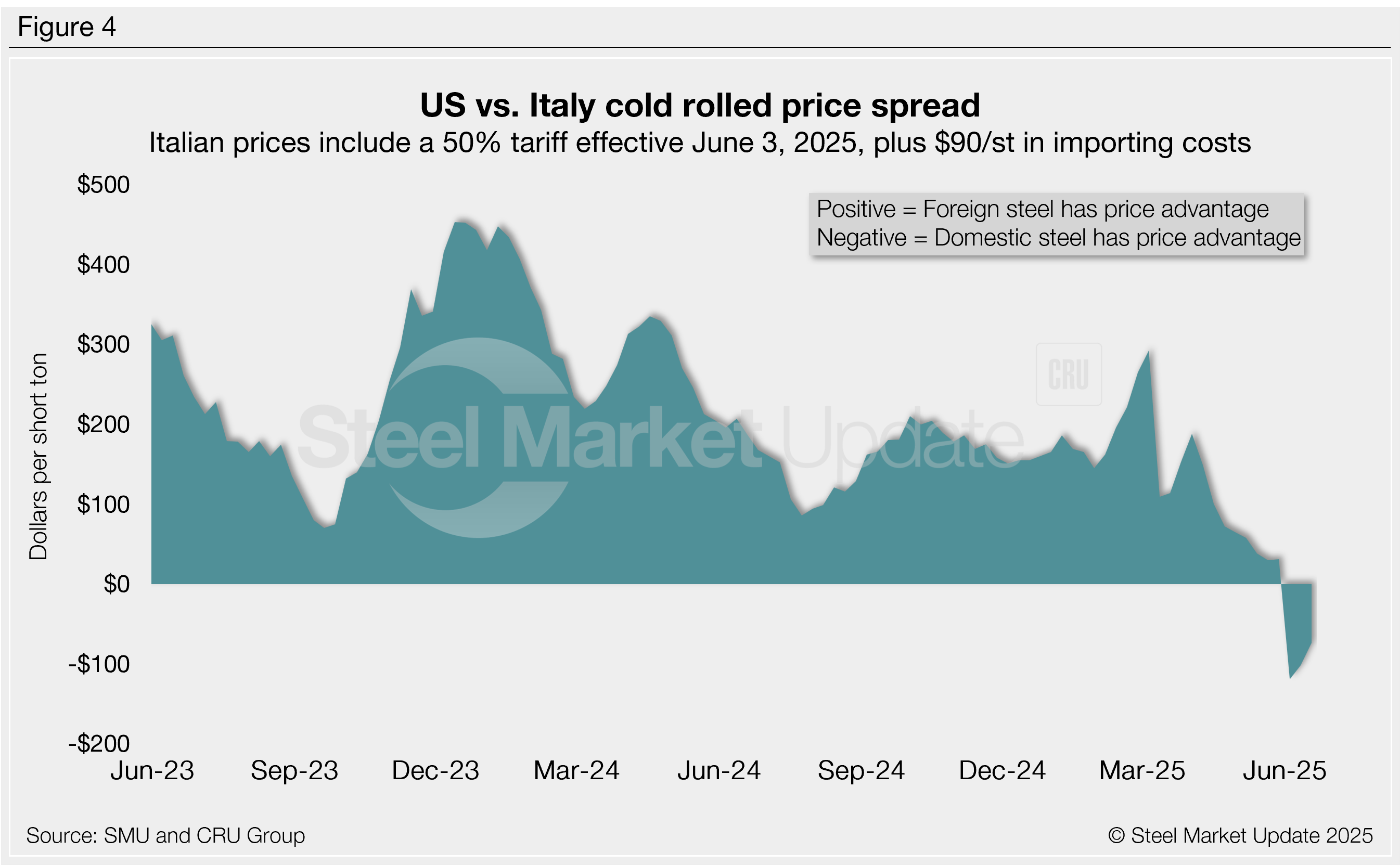

US cold-rolled (CR) coil prices continued to tick higher this week, while offshore markets were mixed.

The trend narrowed the gap between US prices vs. imports even in the face of higher Section 232 tariffs, which doubled to 50% on June 3. While higher tariffs resulted in import prices soaring higher than US prices on a landed basis, recent stateside gains have narrowed the gap.

In our market check on Tuesday, June 17, US CR coil prices averaged $1,090 per short ton (st), up $20/st from the previous week.

By the numbers

Domestic CR prices are now, theoretically, 2.2% below imports on a landed basis, down from nearly a 5% gap the week prior. Before the tariff increase earlier this month, US prices were at a nearly 10% premium.

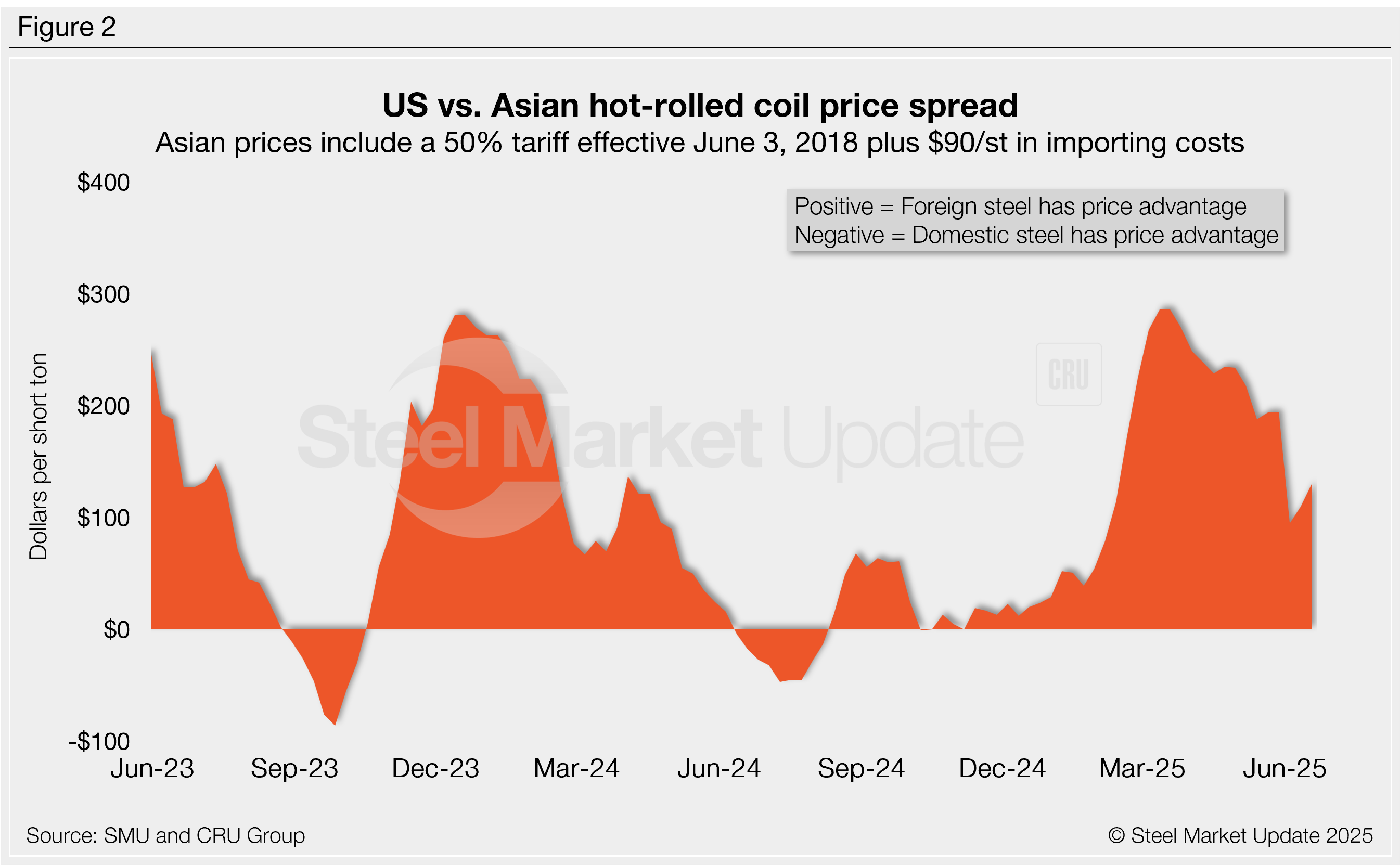

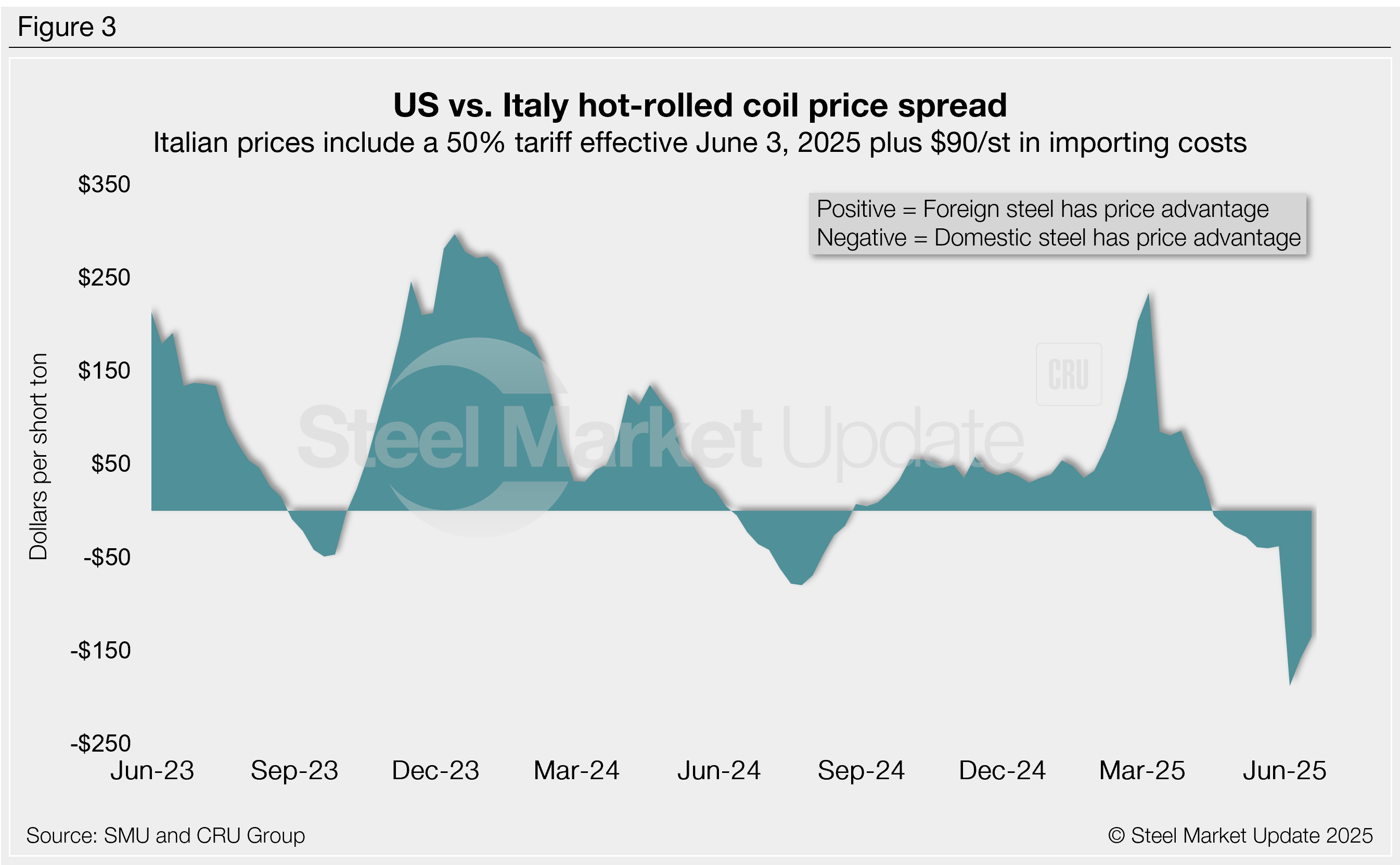

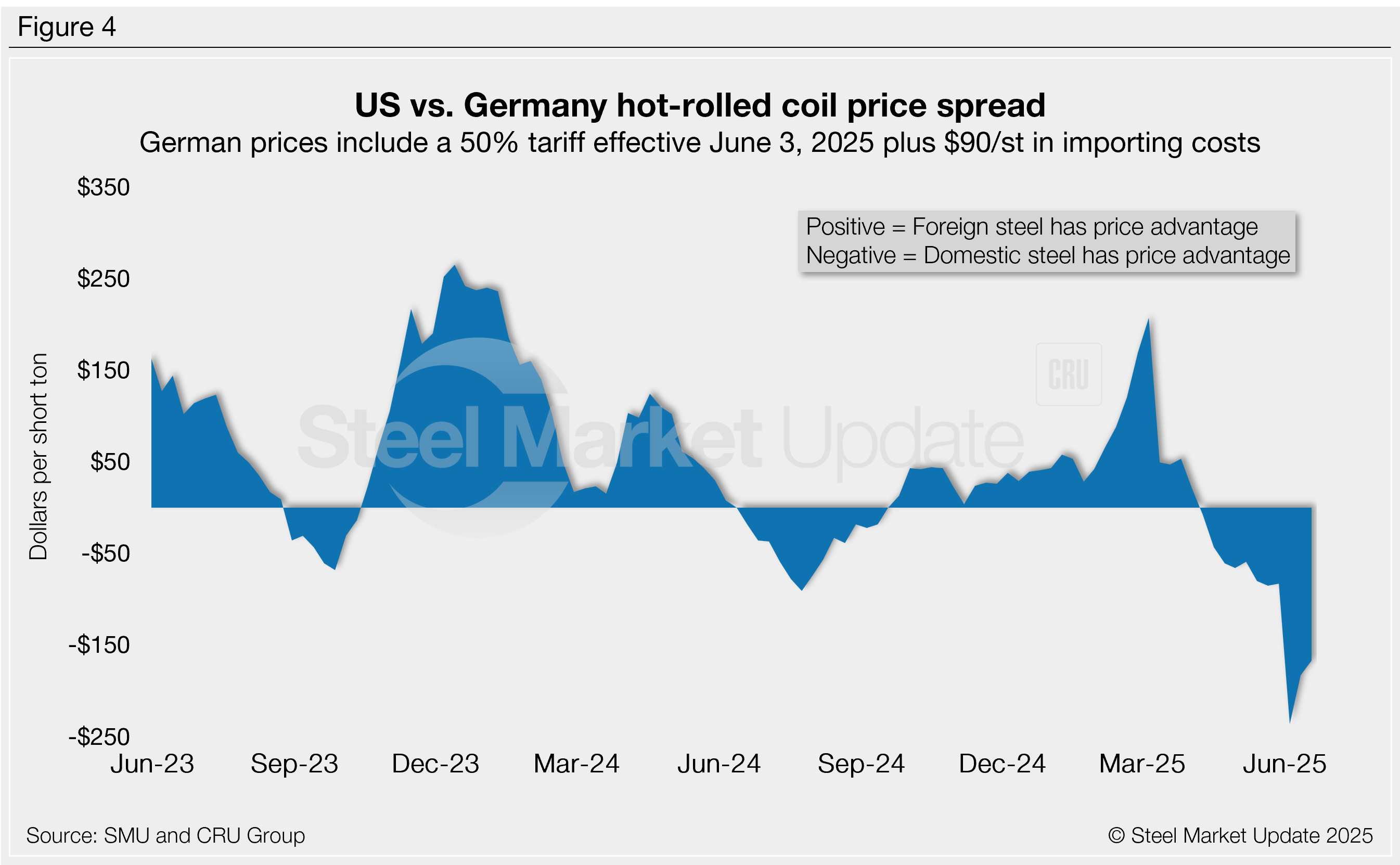

In dollar-per-ton terms, US CR is, on average, $45 per st cheaper than offshore product (see Figure 1). If South Korean CR prices weren’t at such a discount to US prices, stateside product would be roughly 13% cheaper than imports. German, Italian, and Japanese CR are at a significant premium to US cold rolled on a landed basis.

The charts below compare CR coil prices in the US, Germany, Italy, South Korea, and Japan. The left side shows prices over the last two years, and the right side zooms in to highlight more recent trends.

Methodology

SMU calculates the theoretical price difference between domestic and imported cold-rolled (CR) steel by comparing our US CR price (FOB domestic mills) with CRU’s indices (DDP US ports) for Germany, Italy, and East Asia (Japan and South Korea). This is an estimate, and actual import costs vary.

To approximate the cost of foreign steel delivered to US ports, SMU adds $90/st to foreign prices to cover freight, handling, and trader margins. This benchmark can be adjusted based on individual shipping costs. (If you import steel and have insights on these costs, you can contact the author at david@steelmarketupdate.com.)

East Asian CR coil

As of Thursday, June 19, the CRU Asian CR price stood at $494/st, flat w/w. Factoring in a 71% anti-dumping duty (Japan, theoretical), a 50% S232 tariff, and $90/st in estimated import costs, the delivered price to the US is $1,358/st. The theoretical landed price of South Korean CR exported to the US is $832/st.

With the latest SMU CR price up $20/st to an average of $1,090/st, US-produced CR is now theoretically $268/st below Japanese imports but still $258/st above South Korean imports.

Italian CR coil

Italian CR prices were $5/st lower this week to $716/st. After adding import costs and a 50% tariff, the price of Italian CR delivered to the US is, in theory, $1,164/st. That means domestic CR is theoretically $74/st cheaper than CR coil imported from Italy.

German CR coil

CRU’s German CR price was up just $1/st vs. the previous week. After adding import costs and a 50% tariff, the delivered price of German CR is, in theory, $1,184/st. The result: Domestic CR is theoretically $94/st cheaper than CR imported from Germany.

Editor’s note

We reference domestic prices as FOB the producing mill, while foreign prices are CIF the port (Houston, NOLA, Savannah, Los Angeles, Camden, etc.). Inland freight from either a domestic mill or a port is important to keep in mind when deciding where to source from. It’s also important to factor in lead times. In most market cycles, domestic steel will deliver more quickly than foreign steel. Note also that, on March 12, 2025, undiluted Section 232 tariffs were reinstated on steel imports. Section 232 tariffs were then doubled to 50% on June 3, 2025. Therefore, the price comparisons for Japan, South Korea, Germany, and Italy in this analysis now include a 50% tariff.

At the beginning of a steel conference last week in New York, Cleveland-Cliffs Chairman, President, and CEO Lourenco Goncalves referred to the newly acquired U.S. Steel by a completely new name: Nippon Steel USA.

At the end of the same conference, David Burritt proudly claimed that U.S. Steel was a partnership. So, which is it: a partnership or a takeover branded as a partnership? We now have enough information to let everyone reach their own conclusion.

Nippon Steel says in its own documents that U.S. Steel will be a “wholly owned subsidiary”. (Editor’s note: See slide 10 in the presentation here.)

The document makes clear that Nippon Steel, through Nippon Steel America, will have “100% ownership of [the] common stock.” (See slide 4 here.) So if you want to own an interest in U.S. Steel’s future success, you will need to buy shares in Nippon Steel on the Nikkei stock exchange. It certainly will not be in your domestic S&P 500 ETF.

The term “partnership” might be bandied about. But by any legal definition, this is not a partnership because there is only one single owner: Nippon.

True, the “Golden Share” and a national security agreement give the US government the certain rights. Those rights are below:

To appoint and remove one independent director

Consent rights on specific matters such as changing U.S. Steel’s name and headquarters or redomiciling U.S. Steel outside the United States

Transferring production or jobs outside the United States

Material acquisitions of competitors

Certain closure and idling decisions for existing facilities (except temporary idling)

Actions on trade, labor, and sourcing outside the United States

The government has no other voting rights, no right to receive dividends, and it can’t transfer the share. Other provisions about having U.S. citizens in key management roles and certain board positions are little more than window dressing. In the end, Nippon controls the board and management regardless of citizenship, subject to certain important, but limited, U.S. government veto rights.

This raises a few interesting questions

First, with the collective bargaining agreement expiring just before the midterm elections, is the President Trump prepared to be leveraged in labor negotiations? We doubt that the president intends to be involved. But what about the United Steelworkers (USW) union leadership, which has opposed the deal? One can only assume they intend to work every angle.

Second, and perhaps more critically for the steel industry’s overall health, the US industry has shown great resilience because the government has allowed old capacity to exit and new capacity to enter. If an administration blocks rational market behavior by Nippon in the United States, it may just force another domestic company to permanently shut plants if we have excess capacity. This can only be avoided by reducing import supply further.

There are other interesting details in Nippon’s presentation on the acquisition. To start, the business plan assumes a 10 million metric ton increase in domestic industry production at the expense of imports. That’s great if it happens. But are Japanese, Korean, and European steelmakers, among many others, willing to give up their exports as part of any Trump tariff negotiations? We are not holding our breath.

Just about every foreign government wants to be exempt from tariffs or quotas. Will Japan voluntarily step up first and agree to terminate its exports? And, if Nippon has the resources to buy U.S. Steel and invest at least $11 billion in new plants and equipment at U.S. Steel, will Nippon also renounce Japanese government subsidies to build a standard EAF in Japan? Given the U.S. Steel acquisition and declining Japanese and export demand, Nippon should be downsizing Japanese production ASAP.

Separately, Nippon calculates far more indirect steel imports into the United States than other industry sources. This implying that we have a much greater scrap reservoir domestically (and implicitly in Europe) than various third-party estimates assume. If this is true, there is a much larger scrap reservoir to be harvested.

Wider scrap availability should also lead to wholesale changes in all decarbonization calculations for the Europeans and others. (Sorry, EUROFER and Responsible Steel.) In the same vein, Nippon will be installing a DRI facility in Arkansas. A new Hyundai DRI facility is also coming online. So it makes no sense to us that the federal government should spend money and scarce government resources relining or replacing blast furnaces or building DRI modules to keep making virgin iron units with Bidenesque subsidies. The market is building new, efficient natural gas-based DRI facilities to meet these needs.

Nippon is also rebuilding and modernizing a blast furnace in Gary, Ind., on its own dime. This is a sharp contrast to primary aluminum, rare earths, and many other critical materials that require government support to re-shore capacity.

In the end, Nippon is paying a 148% premium to take over U.S. Steel. The senior management certainly earned their bonuses to get the deal through. The deal has enriched U.S. Steel Corporation shareholders. And, if the investment plans work, both the U.S. Steel employees and Nippon Steel shareholders should benefit as profits are repatriated to Japan. So, answer the question yourself: Is it Nippon Steel America, DBA United States Steel, or is it a partnership?

Editor’s note

This is an opinion column. The views in this article are those of experienced trade attorneys on issues of relevance to the current steel market. They do not necessarily reflect those of SMU. We welcome you to share your thoughts as well at info@steelmarketupdate.com.

Cleveland-Cliffs announced the commissioning of its Vertical Stainless Bright Anneal Line at its Coshocton Works facility in Coshocton, Ohio.

The $150 million capital investment has been completed. Cliffs said the line will supply premium stainless steel for high-end automotive and critical appliance applications.

Details

The annealing line utilizes a 100% hydrogen atmosphere instead of conventional acid-based processing. It also includes a hydrogen recovery unit to recycle hydrogen and uses a 50/50 mix of new and used hydrogen.

The Cleveland-based steelmaker said a ribbon cutting ceremony will be held on Wed., July 2, at Coshocton Works.

Goncalves lauds hydrogen

“Since acquiring AK Steel in 2020, our stainless steel business has been the most consistent profit-generating unit for Cleveland-Cliffs,” Lourenco Goncalves, Cliffs’ chairman, president, and CEO, said in a statement on Friday.

“By using hydrogen and advanced automation, we’re dramatically improving the quality and productivity of this critical product that our customers rely upon Cleveland-Cliffs for,” he added.

With so much happening in the news cycle, we want to make it easier for you to keep track of it all. Here are highlights of what’s happened this past week and a few upcoming things to keep an eye on.

Let’s kick off this review with this week’s landmark moment in the long-running drama starring U.S. Steel, Nippon Steel, and the US government. The two companies finalized their “partnership,” which includes the unusual “Golden Share” provision for the feds. It took nearly two years, a couple of presidents, several lawsuits, and a lot of heated rhetoric. And U.S. Steel will remain in its hometown of Pittsburgh. You can check out the terms of the deal, as well as a timeline of the saga.

Tariffs and trade

Tensions are still high between the US and its traditional trading partners under President Trump’s tariff regime. But talks are continuing with Canada and Mexico.

“We will take the time we need to negotiate the best deal for Canada, but no longer,” Canadian Prime Minister Mark Carney said in a statement. “In parallel, we are ensuring that workers and industries are protected from the unjust US tariffs.”

South of the border, Mexico suspended export programs for LAU Industries of Mexico, a US-based steel importer, after alleging the manufacturer took advantage of a government program to promote trade. The move was made while the country negotiates with Washington for an exemption to the 50% tariff on steel imports into the US.

Across the pond, we’re still digging for details on the trade deal between the US and UK. For the automotive industry, an executive order signed by Trump last week establishes an import quota of 100,000 vehicles built in the UK subject to a 10% tariff. For steel and aluminum, the order suggests tariff-rate quotas will be created once the UK meets US requirements on supply chain security and ownership transparency. But the specifics remain murky.

In the meantime, more appliances have been added to the downstream Section 232 tariff list. We have that list here.

Over the last month, bulk scrap sales from the US to Turkey have not materialized. Part of the reason, besides comparatively low pricing in Turkey vs. US domestic levels, may be the swift increase in bulk freight rates from eastern ports in North America. However, several other factors have played a role. SMU’s Stephen Miller has the story.

Prices and surveys

Nucor stepped up its list price for hot-rolled coil (HRC) by $10 per short ton (st) on Monday, the second week of increases after lowering its consumer spot price throughout May. It’s seeking $900 per st.

Cleveland-Cliffs also plans to increase prices for HRC to $950/st with the opening of its July spot order book. That’s up $40/st from its June list price.

Several steel market sources say they were blindsided by the price hikes. “The reason sources found the mill increases so off-putting? From coast-to-coast, steel insiders say that end-market demand remains at a trickle. All sources agree that steel supplies remain ample, and that lead times continue to remain standard,” SMU’s Kristen DiLandro reports.

But the increases may not be sticking. Steel prices inched higher across most of the sheet and plate products tracked by SMU, but market participants have noted that prices aren’t rising as much as announced increases might suggest.

Overall, SMU’s average domestic HRC price gained $20 to reach $880/st. That may be an increase, but it still trails imports from Europe. It’s supported by Section 232 steel tariffs that were doubled to 50% earlier this month.

Economic highlights

The NATO Summit will be taking place in The Hague, June 24-25. Though the meeting of world leaders won’t address tariffs and trade specifically, it’s one of the geopolitical undercurrents flowing as relationships between the US and its allies are strained.

Monday, June 23: Existing home sales (10 a.m.)

Tuesday, June 24: Federal Reserve Chair Jerome Powell testifies to House Financial Service Committee (10 a.m.); Consumer confidence (10 a.m.)

Wednesday, June 25: New home sales (10 a.m.)

Thursday, June 26: Durable goods (8:30 a.m.); GDP, second revision (8:30 a.m.); Pending home sales (10 a.m.)

Friday: June 27: Consumer sentiment (8:30 a.m.)

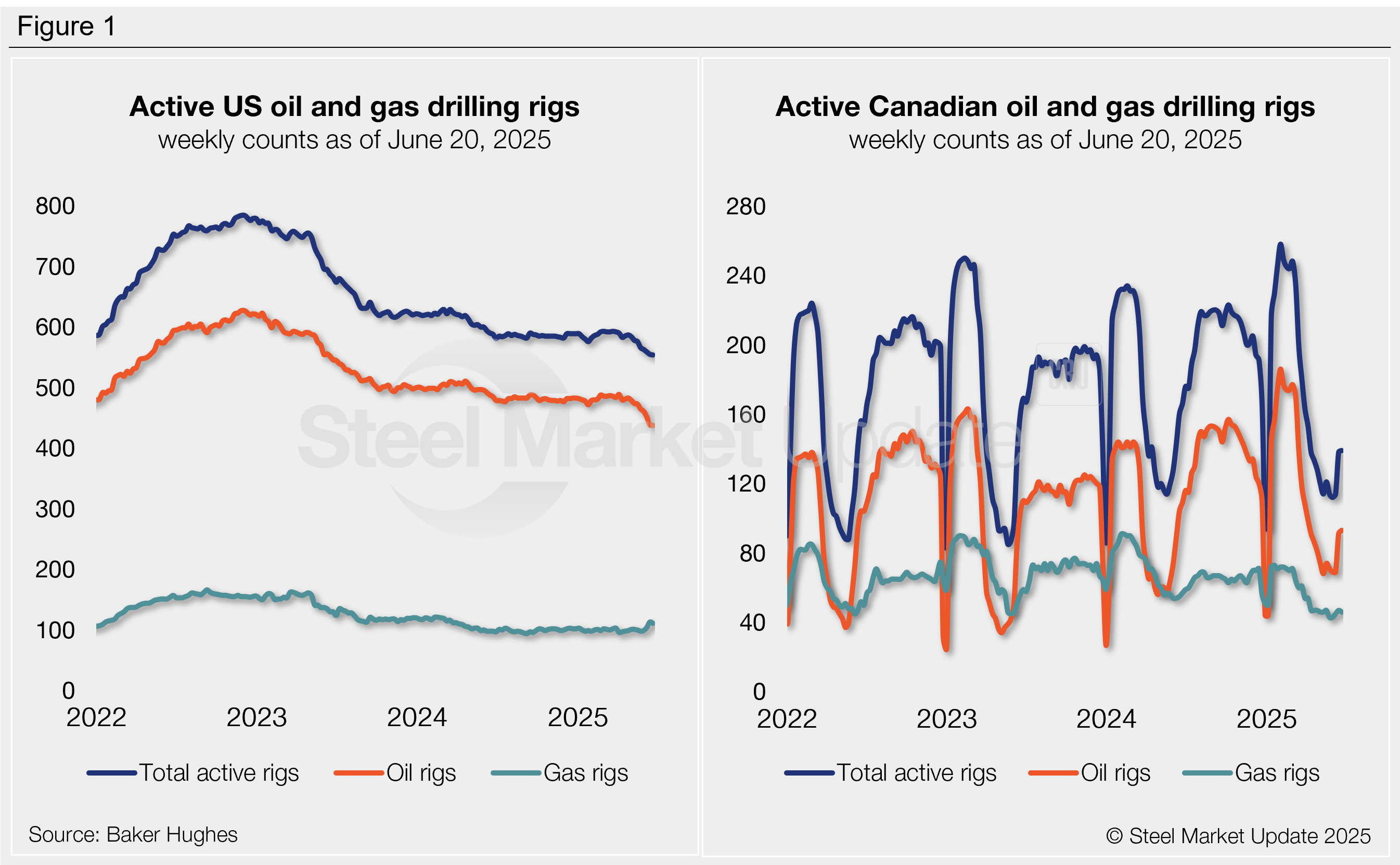

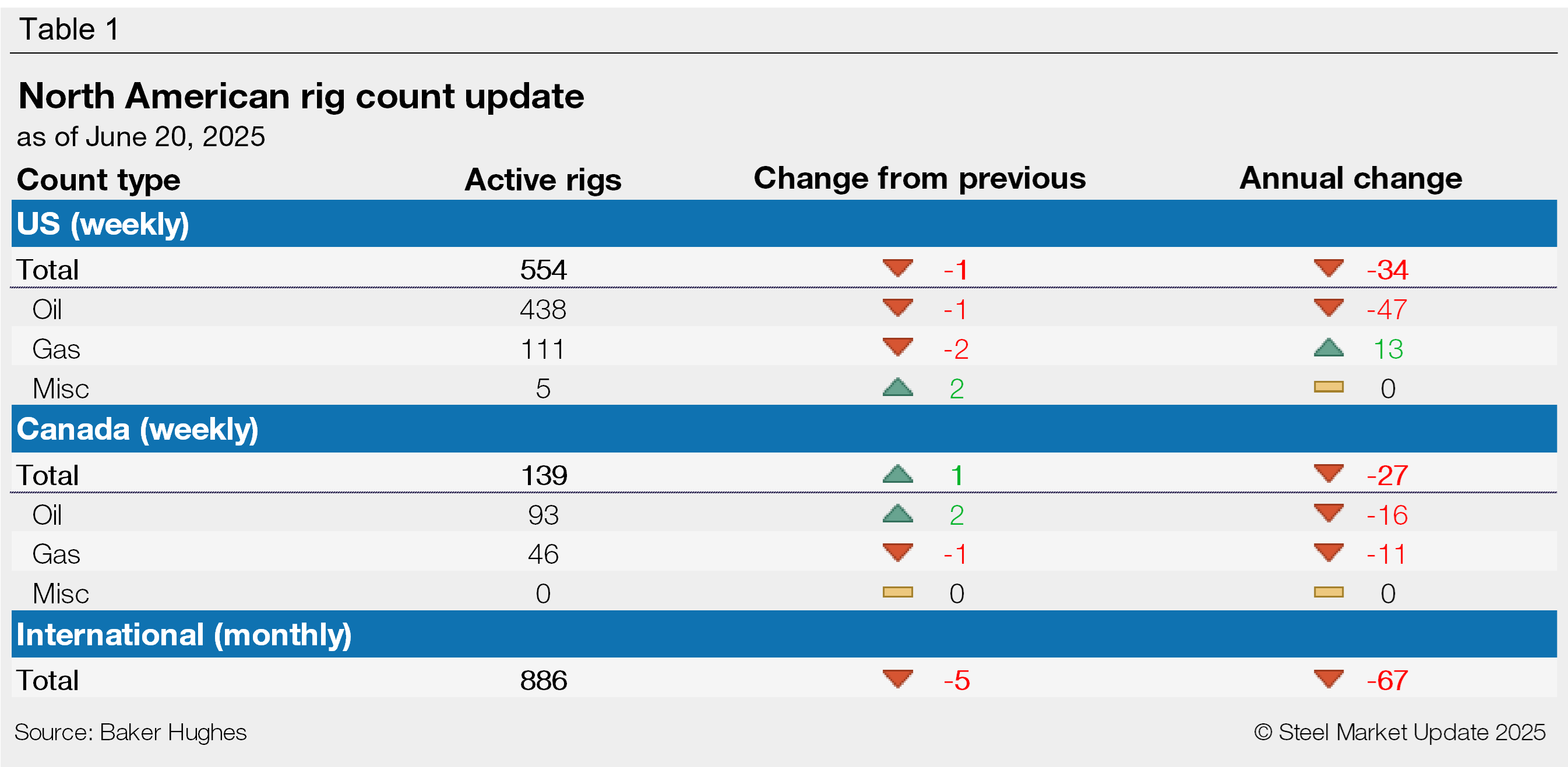

Oil and gas drilling activity declined in the US again this week, while the Canadian rig count improved, according to Baker Hughes.

The US rig count declined by one this week to 554, the eighth-consecutive weekly decline and the lowest rate seen since November 2021. Compared to the same week last year, 34 fewer rigs are in operation today.

The Canadian rig count increased by one rig this week to 139, 27 fewer than the same week of 2024. Canadian activity slows each spring as thawing ground conditions limit access to drilling sites. It then recovers across June and July.

The international rig count is reported monthly at the beginning of each month. The May count was 886 rigs, down five from April and 67 fewer than one year ago.

The Baker Hughes rig count is significant for the steel industry because it is a leading indicator of demand for oil country tubular goods (OCTG), a key end market for steel sheet.

For a history of the US and Canadian rig counts, visit the rig count page on our website.

Chinese steel export prices declined month over month (m/m) amid seasonally sluggish domestic demand. Competitive import offers continued to enter the European market, while in the US doubled Section 232 tariffs reversed domestic sheet prices’ downward trend.

Chinese steel export prices fall amid seasonally weak demand

Chinese steel export prices declined in the past month as the summer lull arrives in the country amid sluggish domestic demand conditions. Tax-evading shipments at lower price levels were still available in the market and added downward pressure on the overall price level.

In parallel, inquiries from Vietnam reduced amid anticipations that the Vietnamese government would add wider hot-rolled (HR) coils from China to the list of products subject to anti-dumping duties.

In Southeast Asia, steel prices in key import markets declined by $14 per mt (mt) m/m on average, as regional demand remained weak.

In Japan, sheet export prices remained stable, while plate export prices declined $80/mt m/m, adjusting downwards after the spike in May amid weak demand in key destination markets.

Indian HR coil export prices fell by $15/mt over the past month. Despite the decline, Indian HR coil was outpriced by offers from other Asian suppliers as competition increased both in the APAC region and in key destination markets. As a result, export volumes from India decreased in the past month, while steel import volumes into the country increased despite the 12% safeguard duty introduced in April.

Competitive import offers continue to enter the European market

In Europe, domestic steel prices declined further over the past month amid weak regional demand and increased interest in competitive import offers. HR coil offers from Indonesia at €470 (USD$542)/mt CIF South Europe continued to gain ground across the European market.

In parallel, Turkey supplied to the European market more than 500,000 mt of HR coil to date under the Q2 safeguard quota (see here CRU’s safeguard quota data tracker). Turkish HR coils delivered to Southern Europe were assessed this week at a discount of $75/mt, duties included, to the locally supplied sheet (please see CRU’s GSTS pdf for more information on landed import prices).

Another factor driving import bookings in Europe is Carbon Border Adjustment Mechanism’s (CBAM’s) implementation from Q1’26. Some buyers are increasing import volumes now in anticipation of possible disruptions or additional costs under the new regime.

In the meantime, Turkish export activity reduced over the past weeks amid low demand in key export markets, while the recent conflict between Israel and Iran has put market players in a wait-and-see mode.

US Section 232 tariffs doubled from 25% to 50%

On June 4, Section 232 tariffs on steel imports increased from 25% to 50% (see related Insight here), reversing the downward trend in the US domestic sheet prices as buyers largely returned to the market.

Rebar import volumes into the US trended lower m/m as import prices reached near parity with domestic prices. In parallel, the Rebar Trade Action Coalition and its individual members filed for an anti-dumping case against Algeria, Bulgaria, Egypt, and Vietnam.

This piece was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

Editor’s note: Steel Market Update is pleased to share this Premium content with Executive members. For information on how to upgrade to a Premium-level subscription, contact Luis Corona at luis.corona@crugroup.com.

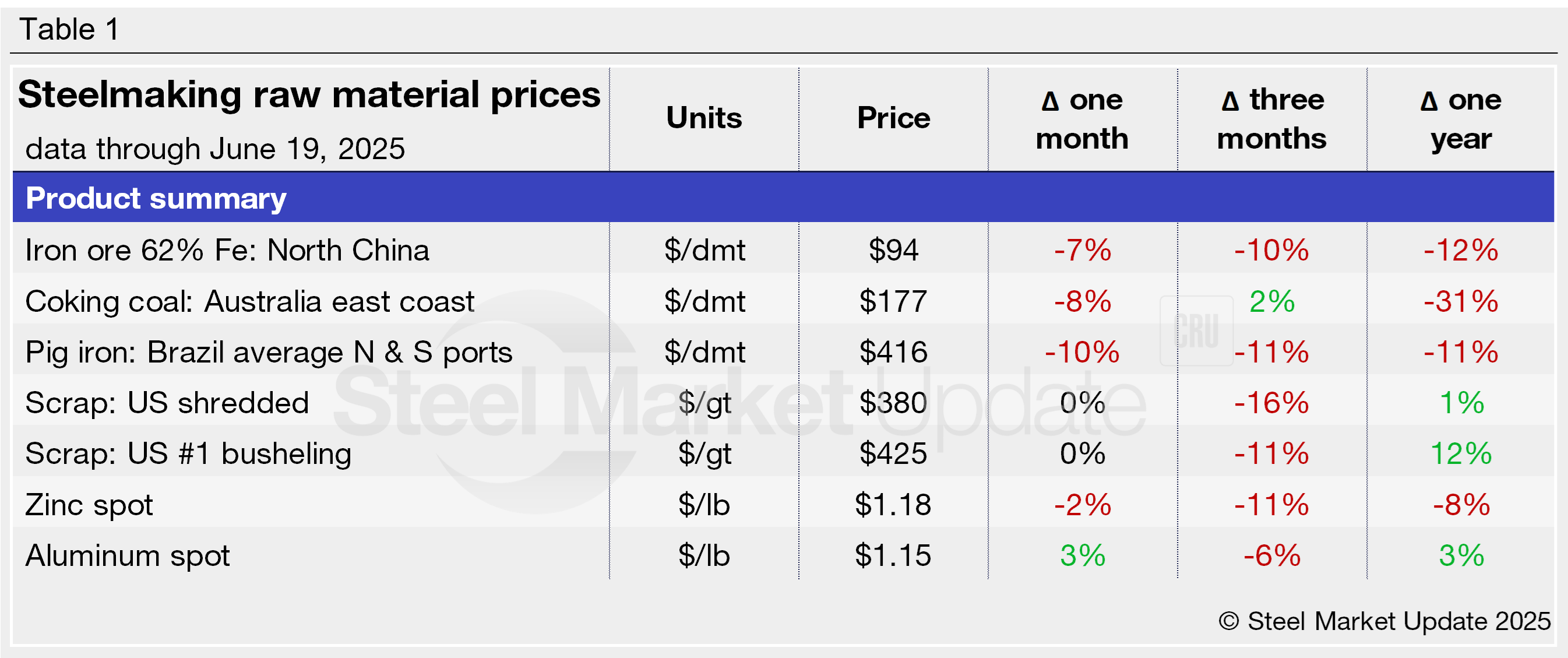

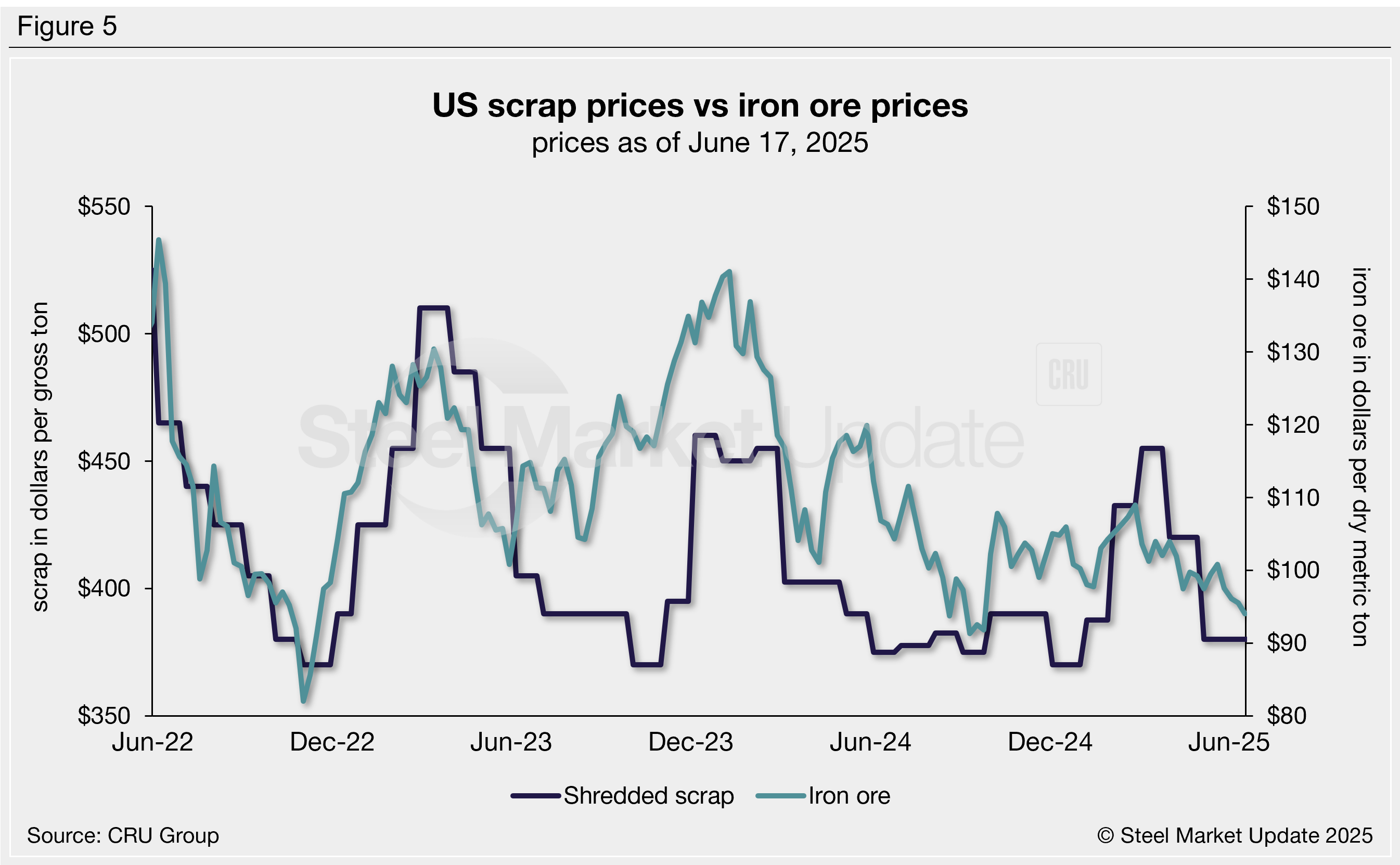

Prices for four of the seven steelmaking raw materials we track declined from May to June, according to our latest analysis. Collectively, these materials declined 3% month over month (m/m) and are down 9% compared to three months ago.

Pig iron, coking coal, iron ore, and zinc all saw m/m price declines in June, while busheling and shredded scrap held steady, and aluminum increased. Six of the seven materials are priced lower than they were three months ago, while prices are mixed compared to the same time last year.

Table 1 shows the latest prices for each product and their changes from recent months.

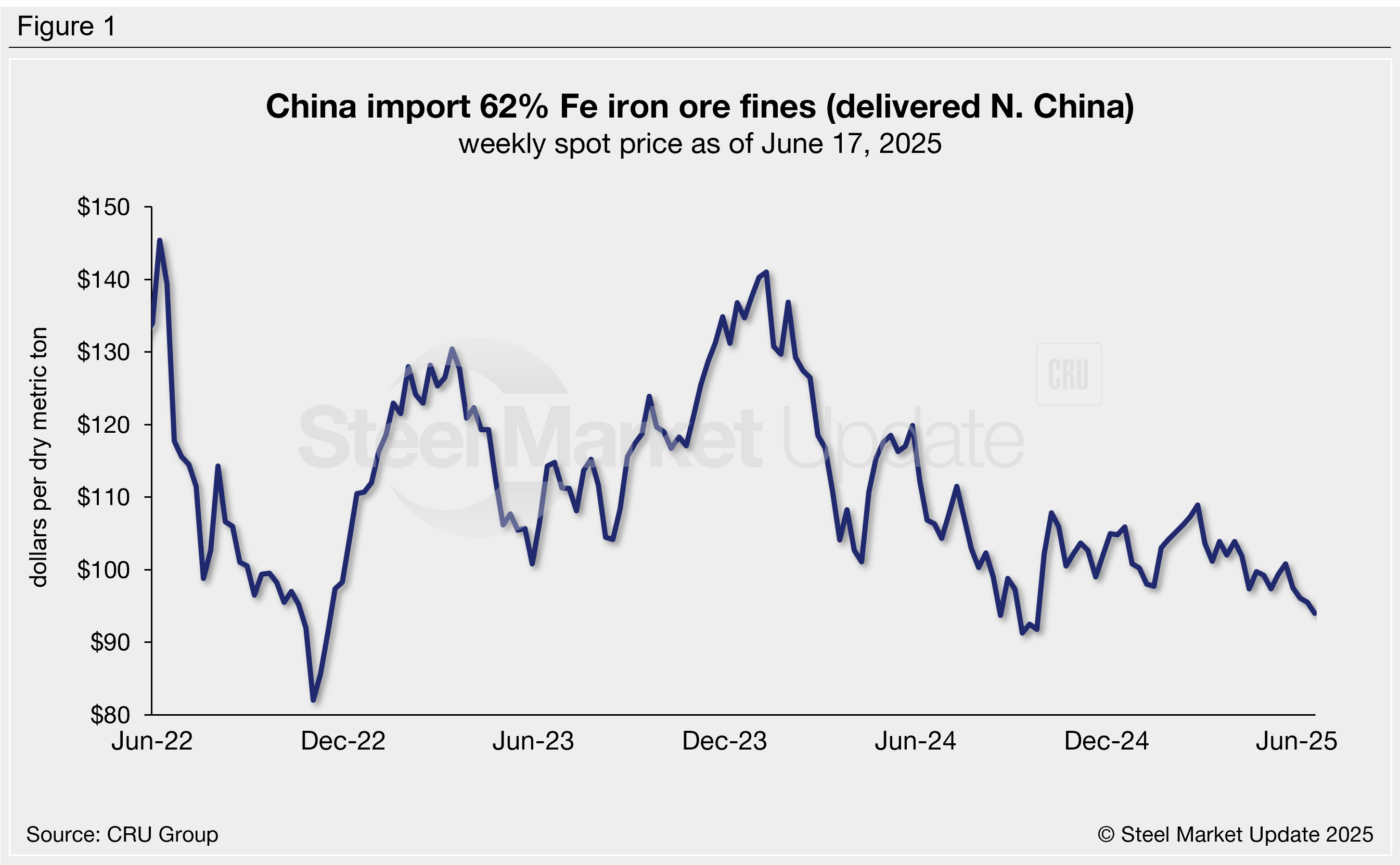

Iron ore

The import price of 62% Fe Chinese iron ore fines has trended lower since February, falling 7% across the past month. As of June 17, prices are down to an eight-month low of $94 per dry metric ton (dmt) delivered North China. Prior to June, iron ore had generally hovered between $97-109/dmt since October (Figure 1). Prices are 10% less expensive than they were three months ago and 12% lower than this time last year.

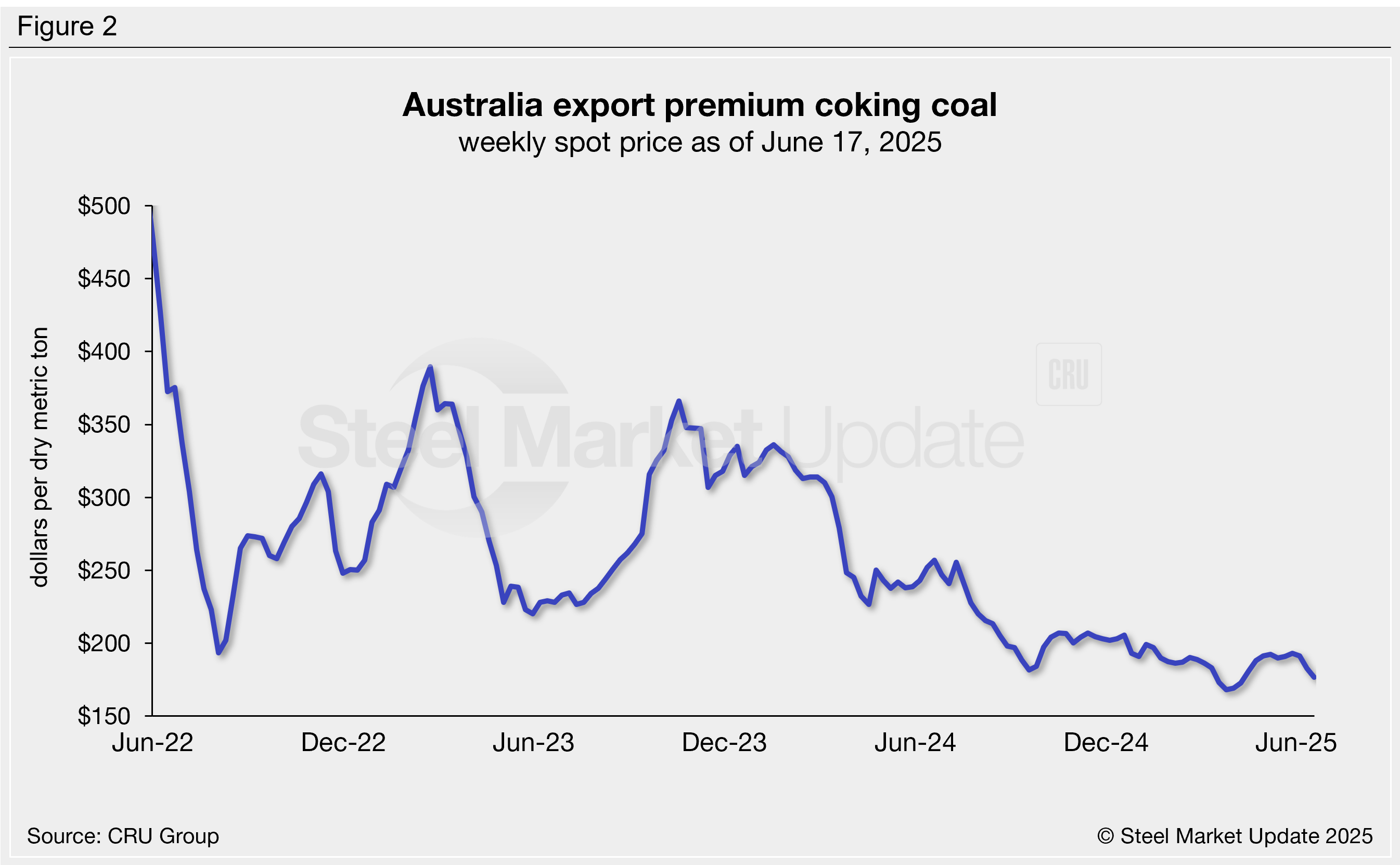

Coking coal

Premium hard coking coal prices have trended lower for over a year and a half, recently reaching a near four-year low of $168/dmt in late March. Prices marginally ticked higher through the end of May but have since eased 8%, down to $177/dmt this week (Figure 2). Coking coal is 2% more expensive than it was three months ago, but 31% cheaper than one year ago.

Pig iron

After falling to a four-year low of $415/dmt earlier this year, pig iron prices rebounded in March to $465/dmt and held steady through May. This recovery was completely erased in June, with prices falling 10% m/m to $416/dmt (Figure 3). Pig iron is 11% cheaper than it was both three months ago and in June 2024.

Recall that pig iron prices soared to a historic high of $975/dmt in May 2022 following the invasion of Ukraine. Most of the pig iron imported to the US was imported from Russia, Ukraine, and Brazil. This report uses Brazilian prices (now the primary source of US pig iron imports) and averages prices from the country’s northern and southern ports.

Scrap

Like pig iron, steel scrap prices have trended lower since peaking in March, slipping 7-10% from April to May and holding steady in June. SMU’s latest shredded scrap price was $380 per gross ton (gt) through June and busheling scrap was $425/gt, down 11-16% compared to three months prior (Figure 4). Compared to this time last year, busheling scrap prices are 12% higher today, while shredded scrap is up just 1%.

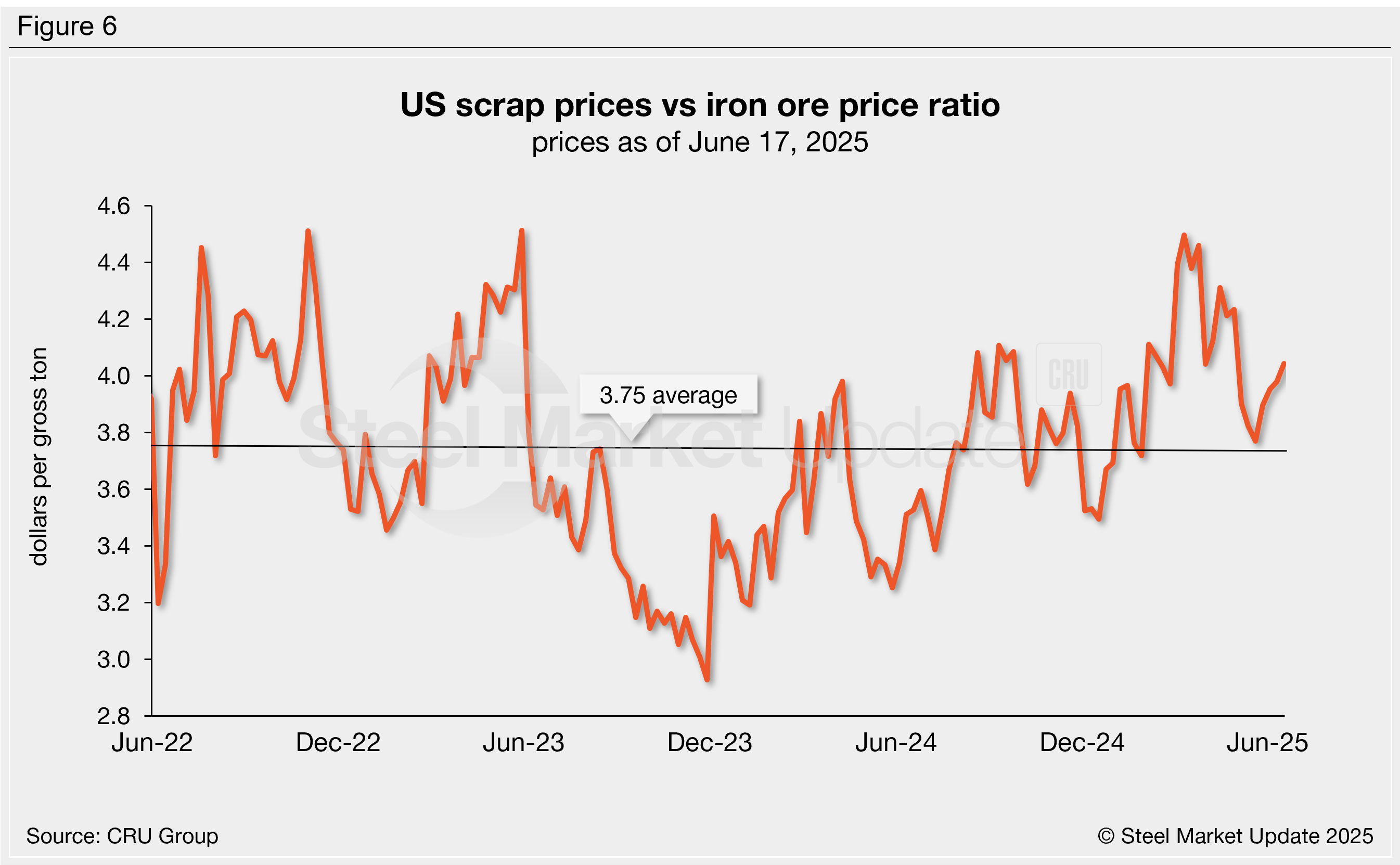

Fluctuations in scrap and iron ore prices provide insight into the competitiveness of integrated (blast furnace) mills, whose primary feedstock is iron ore, vs. mini-mills (electric-arc furnace), whose primary feedstock is scrap. Figure 5 compares the prices of these two mill raw materials.

To compare these two mill feedstocks, SMU divides the shredded scrap price by the iron ore price to calculate a ratio. A higher ratio favors the integrated mills, a lower ratio favors the mini-mill producers.

Integrated mills generally held the cost advantage from late 2021 through mid-2023, then it briefly shifted to mini-mill producers in the second half of 2023 through the first few months of 2024 (Figure 6). After bouncing around, the ratio has slightly favored integrated mills since early 2025. It has trended lower since March’s near-two-year high of 4.50, standing at 4.04 as of June 17.

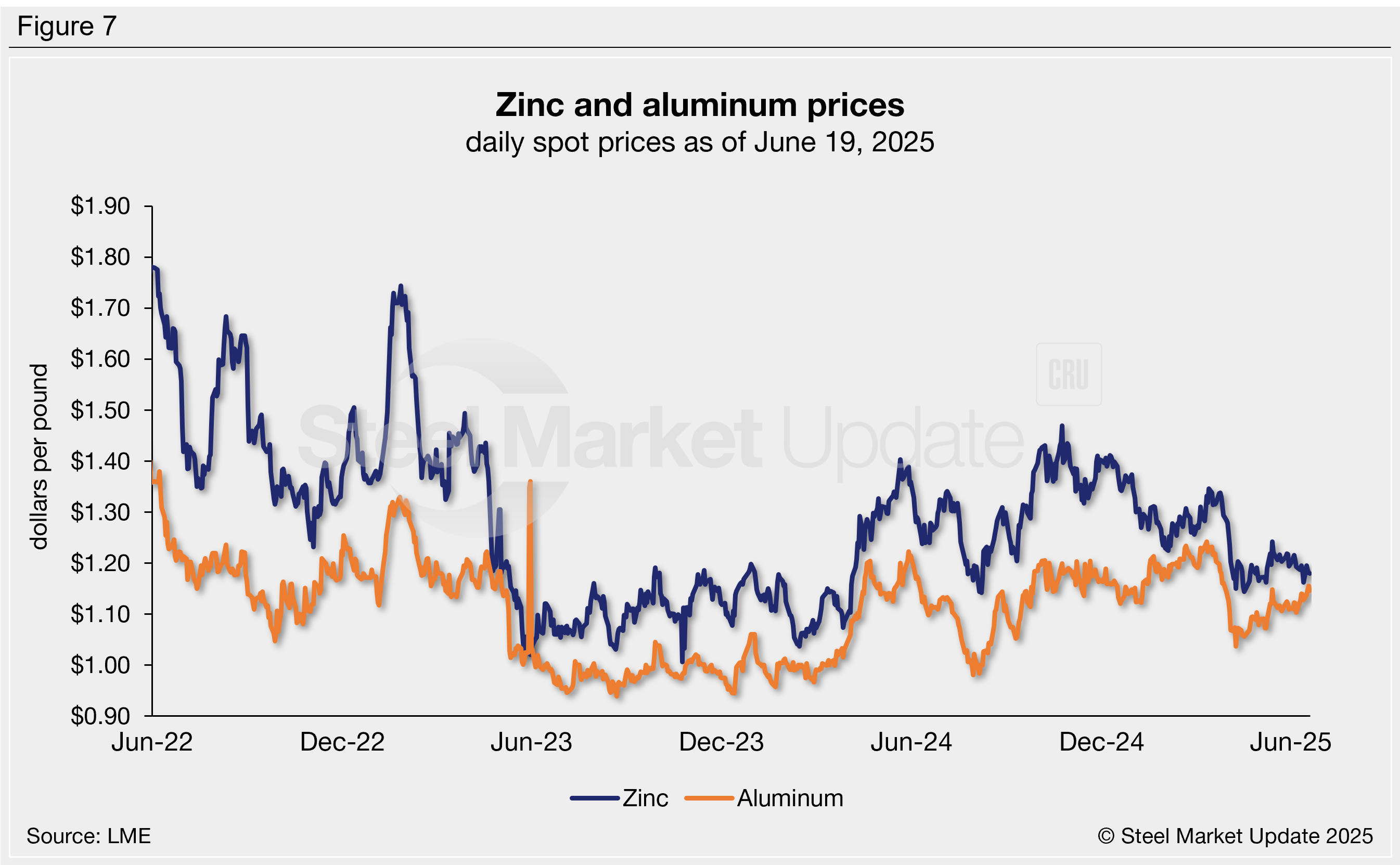

Zinc and aluminum

Zinc and aluminum are used in some coated steel products. Fluctuations in spot prices can prompt steel mills to adjust their galvanized and Galvalume coating extras.

Zinc prices have remained relatively stable since May, easing 2% across the past month and holding near some of the lowest levels recorded in the last nine months. The latest LME zinc cash price is $1.18 per pound as of June 19, 11% lower than three months ago and 8% cheaper than prices seen one year ago (Figure 7).

Aluminum price movements had mostly followed zinc for the first five months of the year but have trended higher in the past two weeks. The latest LME cash price is $1.15/lb, up 3% m/m. Aluminum prices are 6% lower than they were three months ago, but 3% higher than June 2024 levels. Note that aluminum spot prices can be volatile at times, though sharp swings typically correct within a few days, as seen once in Figure 7.

The Canadian Steel Producers Association (CSPA) and the United Steelworkers (USW) union in Canada have said they were disappointed by the country’s Prime Minister Mark Carney’s remarks regarding steel and aluminum tariffs on Thursday.

“Our initial reaction to the Government of Canada’s plan … is that it falls short of what our industry needs at this most challenging time,” the two groups said in a joint statement.

The groups said they will continue to review the details of the measures and “work constructively with the federal government to get a plan that works for Canadian steel producers and the thousands of workers that make up our sector.”

The letter was written by Catherine Cobden, CSPA president and CEO, and Marty Warren, the USW’s national director for Canada.

As SMU reported on Thursday, Carney laid out plans for stricter controls on imported steel and aluminum, including the roll-out of tariff-rate quota, or soft quota, system, among other things.

Canada is ramping up its economic counteroffensive against the US’ decision to double tariffs on Canadian aluminum to 50%, unveiling a sweeping series of policy changes aimed at protecting domestic producers and asserting trade sovereignty through its own protectionist measures.

The moves include reciprocal procurement restrictions, import quotas, a strategic financing facility for large firms, and the formation of stakeholder task forces for aluminum industries.

‘Country of smelt and cast‘