SDI earnings slip in Q2 as trade volatility hits customer orders

SDI profits slipped in second quarter amid trade policy volatility.

SDI profits slipped in second quarter amid trade policy volatility.

Cleveland-Cliffs lost more than $400 million for the third consecutive quarter but predicted results would improve in the second half of the year. And shares of the Cleveland-based steelmaker surged after company executives said during its Q2 earnings call on Monday that they could make billions by courting foreign investors or selling assets.

What to look out for regarding ferrous scrap ahead of Steel Summit.

Drilling activity increased in both the US and Canada for the week ended July 18, according to the latest data from Baker Hughes.

The Chinese government has threatened countermeasures on Canada following the Canadian government's announcement on curbing steel imports, according to media reports.

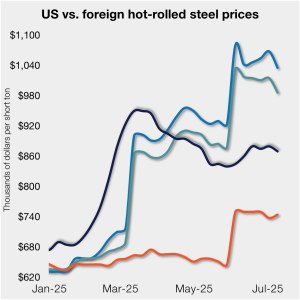

Cold-rolled (CR) coil prices continued to tick lower in the US this week, with a similar trend seen in offshore markets.

Chinese steel export prices are expected to rise and support prices across most of Asia in the coming month. In Europe, buyers are likely to frontload import orders ahead of CBAM imposition, while new trade agreements are likely to emerge in the US. Steel prices in the APAC are expected to rise, except in India […]

Not much to report on from the sleepy HRC futures market in the thick of the summer doldrums with trading volume nearly grinding to a halt.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market events.

Canadian Prime Minister Mark Carney has announced new measures to limit steel imports into the country.

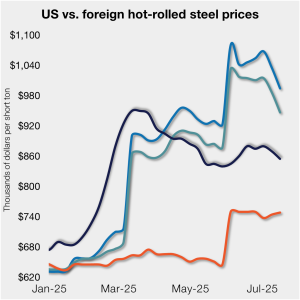

Stateside prices continue to trail imports from Europe, supported by Section 232 steel tariffs that were doubled in early June.

The Canada Border Services Agency has terminated a self-initiated dumping investigation of corrosion-resistant steel sheet (CORE) from Turkey.

Evraz NA and Welded Tube of Canada have lodged an unfair trade complaint against imports of OCTG, including those from USMCA trading partners Mexico and the US.

US sheet and plate prices were flat or lower as reduced import volumes were offset by so-so demand.

US steel exports rose 10% from April to May but remained low compared to recent years. This came just one month after exports fell to the lowest level recorded in nearly five years.

President Trump's threatened tariffs on Brazil, USMCA partners, and Europe could shake up the scrap and pig iron markets in August.

The volume of raw steel produced by US mills inched higher last week, according to the American Iron and Steel Institute (AISI). After steadily increasing in April and May, domestic mill output stabilized in early June and has remained historically strong since.

Trade issues do not seem poised to leave the headlines anytime soon. And as recent developments show, the administration’s tariff policy remains ever-changing.

CRU Principal Analyst Shankhadeep Mukherjee expects a restocking cycle for steel sheet products in most parts of the world due to either low inventories or seasonally stronger demand.

US oil and gas drilling activity continued to decline for the 11th consecutive week, while Canadian counts climbed for the sixth week in a row, according to the latest data from Baker Hughes.

SMU’s Steel Buyers’ Sentiment Indices moved in opposite directions this week. After rebounding from a near five-year low in late June, Current Sentiment slipped again. At the same time, Future Sentiment climbed to a four-month high. Both indices continue to show optimism among buyers about their company’s chances for success, but suggest there is less confidence in that optimism than earlier in the year.

The difference: The spat with Turkey was a big deal for steel. This time, the 50% reciprocal tariff for Brazil – if it goes into effect as threatened on Aug.1 – hits everything from coffee and to pig iron. It seems almost custom-built to inflict as much pain as possible on Brazil.

Mill lead times for sheet products were steady to slightly longer this week compared to our late June market check, while plate lead times contracted, according to steel buyers responding to this week’s market survey.

Coming out of the holiday market and long weekend, it seems the HRC futures market has caught some post-vacation blues.

Hot-rolled (HR) coil prices in the US ticked down this week but have fluctuated little over the past month. Stateside tags continue to trail imports from Europe, supported by Section 232 steel tariffs that were doubled in early June.

Domestic mills are more open to talk price on new orders than they were in June, according to most steel buyers responding to our market survey this week. Negotiation rates have recovered from the early-June lull and are now just a few percentage points shy of the high levels seen late last year.

The announcement of 50% tariffs on Brazilian imports, including pig iron, could have a dramatic effect on steelmaking raw materials.

Ferrous scrap prices are flat in the US for a second consecutive month, but tariffs on imports of Brazilian pig iron could change the game in August.

With steel prices drifting and trade flows shifting, CRU analysts provided a grounded look at what's really happening — and what's not — across the metallics supply chain during Wednesday's SMU Community Chat.

President Donald Trump on Wednesday said he would increase the “reciprocal” tariff on imports from Brazil to 50% effective Aug. 1. That could have big implications for pig iron.