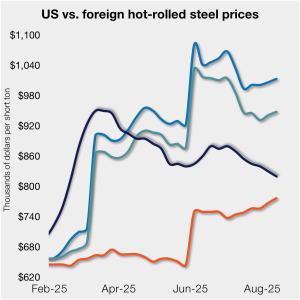

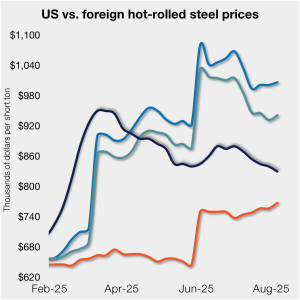

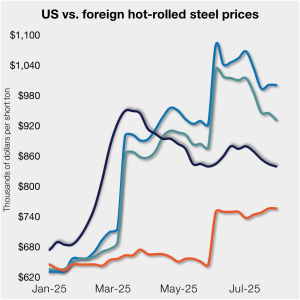

S232 widens the spread between US HRC and imports

Hot-rolled (HR) coil prices in the US declined again last week, while offshore prices ticked higher again week over week (w/w).

Hot-rolled (HR) coil prices in the US declined again last week, while offshore prices ticked higher again week over week (w/w).

Canada has launched an investigation into the alleged dumping of imports of oil country tubular goods (OCTG) by five countries – Korea, the Philippines, Turkey, Mexico, and the United States.

All five of SMU's steel sheet and plate price indices declined this week, falling to lows last seen in February.

Sources in the carbon and alloy steel plate market said they are less discouraged by market uncertainty resulting from tariffs or foreign relations, but are instead, eager to see disruption to the flat pricing environment.

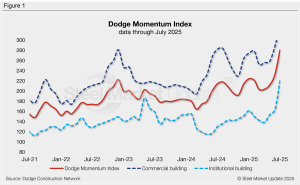

The Dodge Momentum Index (DMI) jumped 20.8% in July and is now up 27% year-to-date, according to the latest data released by Dodge Construction Network.

What are our scrap survey participants saying about the market?

The administration continues to negotiate deals with US trading partners, and the reciprocal tariff program appears poised for further modification. This week, we focus on other important developments that may have received less media attention.

Hot-rolled (HR) coil prices in the US declined again last week, while offshore prices increased week over week (w/w).

Oil and gas drilling in the US slowed for a third consecutive week, while activity in Canada hovered just shy of the 19-week high reached two weeks prior.

This week’s SMU survey reveals that a growing number of steel market participants are weary of tariffs and are awaiting evidence of progress reshoring. At the start of 2025, now-second-term President, Donald Trump, pronounced that his plan to implement tariffs would result in increased revenue for the US.

Both SMU Sentiment Indices continue to show that buyers remain optimistic for their company’s chances of success, though far less confident than they felt earlier in the year.

The volume of steel shipped outside of the country in June fell 3% from the prior month to 618,000 short tons (st), according to recently released data from the US Department of Commerce.

What the word "sideways" means can depend on where you sit on the procurement spectrum.

Since the last writing of this article, CME hot-rolled coil (HRC) futures have been largely steady and lifeless, though there’s been some brief bouts of intraday volatility.

Following January’s pre-tariff surge, imports have remained low since February compared to post-pandemic volumes

SMU’s Monthly Review provides a summary of our key steel market metrics for the previous month, with the latest data updated through July 31.

Mill production times for sheet products are holding just above multi-year lows, while plate lead times remain elevated.

Most steel buyers continue to report that mills are open to negotiating spot prices. Negotiation rates have remained high for most of the past three months.

Current and future scrap sentiment indices declined this month, according to SMU’s latest ferrous scrap survey data.

Sheet and plate prices were either flat or modestly lower this week on softer demand and increasing domestic capacity.

A recent conversation with Tanners shows that many of us in this industry often end up here by accident but end up staying.

The ferrous scrap market for August appears to be settling sideways as the threats posed to the market in July have not materialized.

Truchas works in Lazaro Cadenas, Michoacan, western Mexico. Repairs may take up to six months.

We’re in the dog days of summer, and the question is whether the market will improve as lead times stretch into September. Your answer to that question might depend on where you are in the supply chain. And producers, it seems to me, are a lot more optimistic than consumers at the moment.

Prices for four of the seven steelmaking raw materials we track were unchanged from late June through the end of July, while two increased and one declined. Collectively, these material prices rose 1% month over month (m/m), but are down 3% compared to three months ago.

Drilling activity slowed in the US and Canada last week, according to the latest oil and gas rig count data released by Baker Hughes.

The ferrous scrap export market off the US East Coat and Gulf Coast has remained basically sideways over the last month. This mirrors the lack of movement in the US domestic market.

US manufacturing activity slowed again in July to a 10-month low

Several EU member states have published a ‘non-paper’ that puts forward proposals for a post-safeguard trade measure.

Hot-rolled (HR) coil prices in the US edged lower again this week, while offshore price were little changed. Stateside prices continue to trail imports from Europe, supported by Section 232 steel tariffs.