Analysis

May 5, 2026

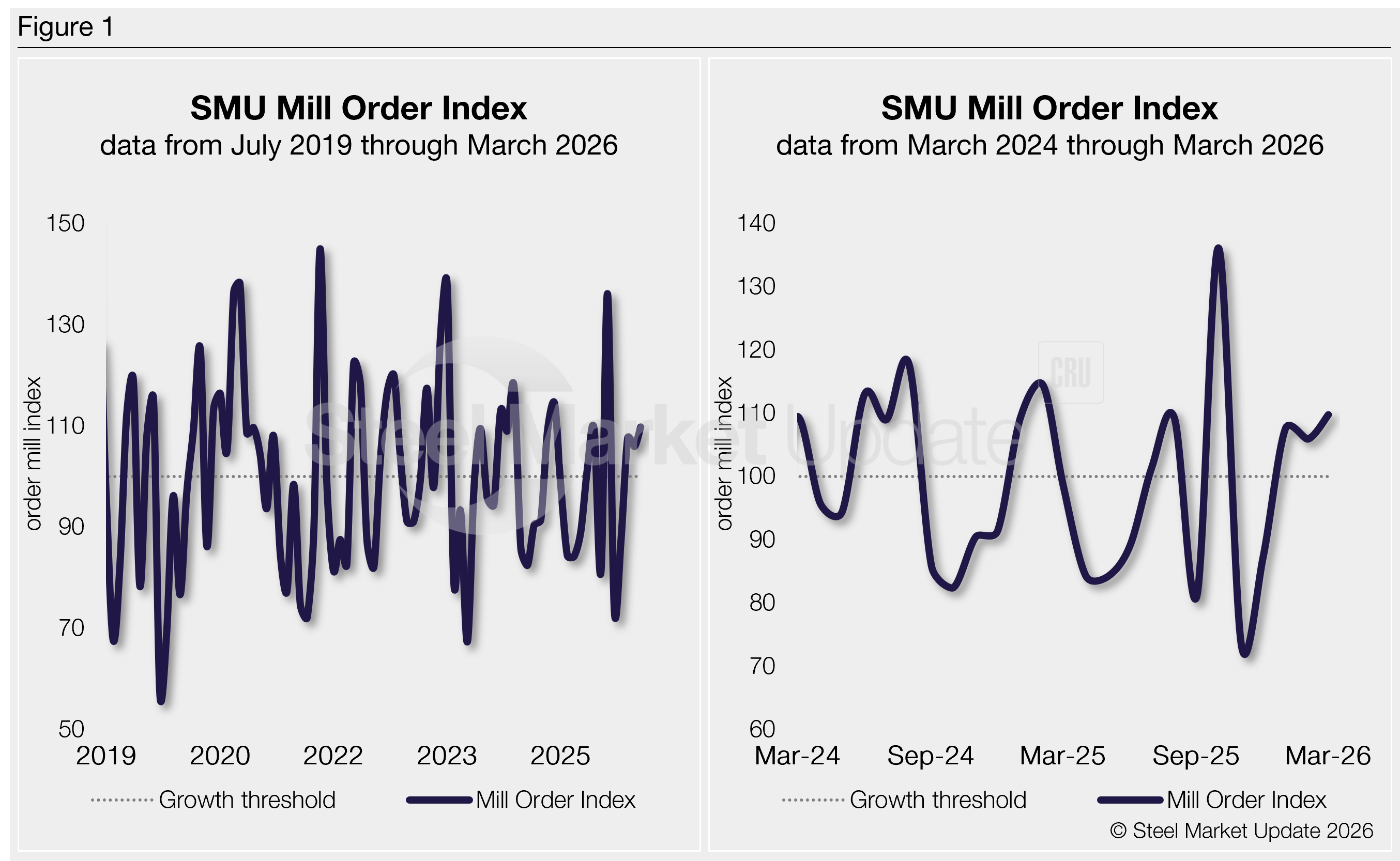

SMU's Mill Order Index improved in March

Written by David Schollaert

SMU’s Mill Order Index (MOI) recovered in March, gaining some momentum after a marginal decline in February. The result came as service center on-order volumes increased, supported by higher overall shipments, according to our latest service center inventories data.

Mill new order entries in March ticked up, supported by efforts at the service center level to keep backfill inventories in line with demand. The dynamic remains complicated as the market continues to experience a supply-side squeeze.

This trend was further highlighted by last month’s decline in intake. March intake was down 5.7% month on month (m/m) due to a nearly 10% increase in shipments. New order entries were up just 3.6% in March vs. February, and concern for the supply pipeline is still a theme with longer lead times.

Service centers’ daily shipping rates—down 0.4% from February—were nearly flat, but additional shipping days boosted overall shipments last month. Average shipping days last month were 22, up from 20 in February.

Key highlights

Recent efforts to maintain leaner inventories have shifted slightly as steel availability is squeezed. This is reflected in a jump in the percentage of inventory on order, which rose nearly 15% m/m.

While service centers continue to balance inventory with demand, the proposition has become more challenging. Spot tons are not readily available, and relying exclusively on contract tons may lag demand. When comparing year-ago levels, inventories are down more than 16%, while shipments are nearly even (+0.2%).

The MOI now stands at 109.7, up 3.6% from 105.9 in February. The rate was in line with typical seasonal readings, but up more than 11% y/y. Results continue to suggest service centers are still closely monitoring inventories, but market dynamics have improved since the initial shock of the new tariff regime last spring.

Methodology

SMU derives its MOI—a relative index that evaluates the latest change in service center mill order entries—from our monthly service center inventory data. This index is a good indicator of current service center buying patterns, displaying perceived demand and lead times. This stands out because lead times typically signal upcoming moves in steel prices.

The MOI uses a base period, presently 2022-24, to establish a reference point for measuring service centers’ mill orders over time. This base period is assigned an index value of 100. Subsequent MOI values are then calculated relative to this base.

An index score above 100 indicates an increase in buying, and a score below 100 indicates a decrease.

Figure 1 shows the nearly six-year history of the index on the left and provides a closer look at the MOI readings of the past two years on the right (100 = 2022-2024 average).

Background

Market conditions in 2025 saw brief price spikes, but overall activity remained mostly steady and at times sluggish. It was held back by weak end‑use demand (as shown in the right‑side chart of Figure 1).

Intake volumes rose through much of Q1 as downstream buyers pulled purchases forward in anticipation of tariff‑driven price increases. That surge in service center orders pushed mill prices up quickly, even though underlying demand didn’t improve.

After peaking a year earlier, intake volumes began a gradual decline. Service centers ultimately caught the market low point in October and held their positions through the end of 2025.

The lowdown

It’s no surprise to see intake volumes generally improve in Q1, driven by seasonal gains. But gains remain subdued and behind year-ago levels. Downstream customers continue to tightly manage inventories, prioritizing contract fulfillment, even as service‑center shipments showed some marginal lift.

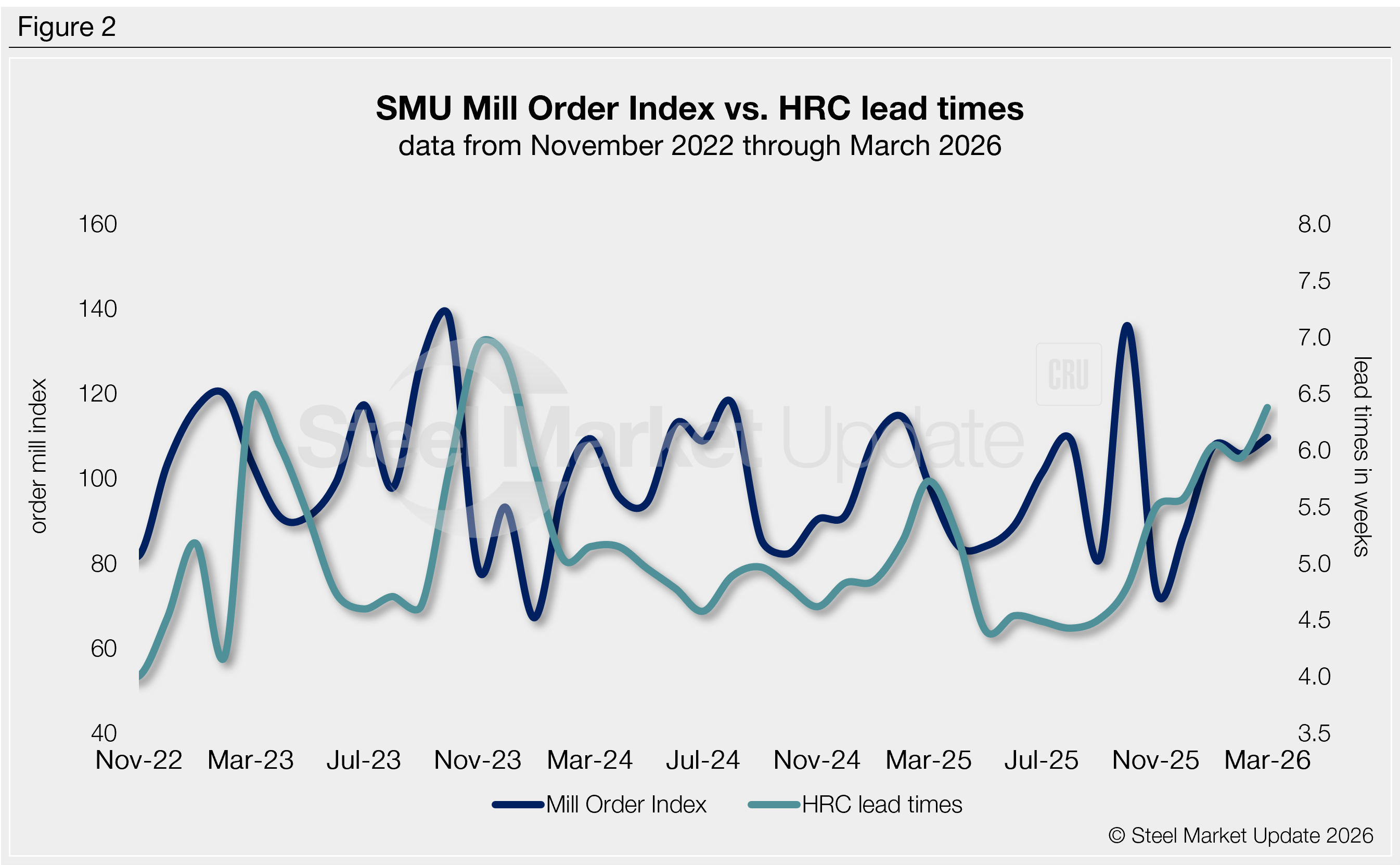

While new order entries saw a notable increase in October—reaching a two-year high—they quickly declined by more than 30% in November and have since been relatively stable.

The data would indicate the improvement and subsequent leveling observed in the first three months of 2026 are in line with seasonal patterns. Mills, meanwhile, are pushing prices up, keeping production in check, driving a supply-side squeeze amid some growing demand.

SMU’s MOI will likely fluctuate somewhat further in April and through Q2. The general expectation is that inventories, while tight, could be impacted even more as new order entries rise, and lead times remain extended. Production delays and planned outages in Q2 will likely keep lead times longer, impacting the supply pipeline.

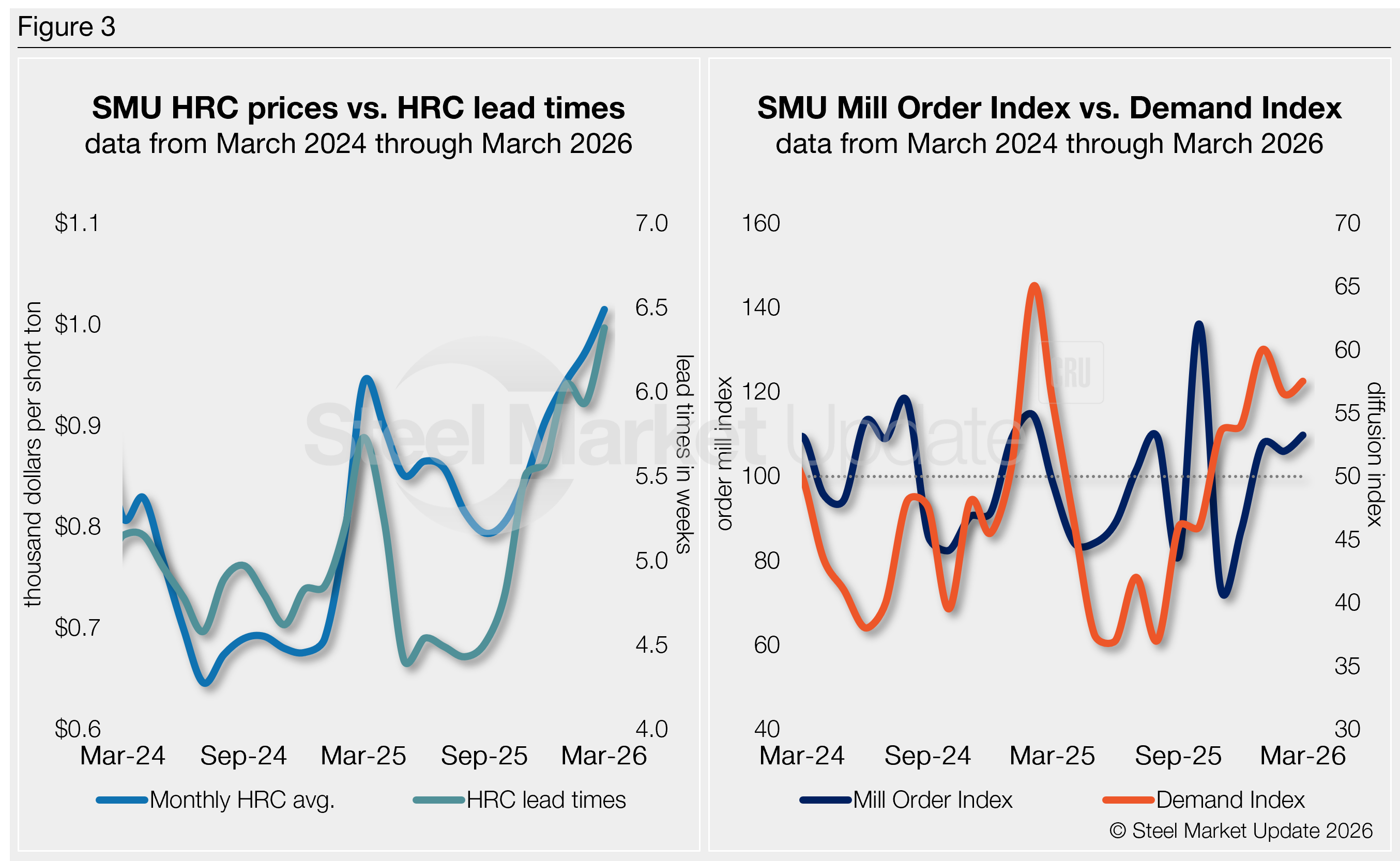

SMU’s MOI pairs well with—and for the past five years has preceded—moves in mill lead times (Figure 2), though the latest results would indicate a divergence. And SMU’s lead times have also been a leading indicator of flat-rolled steel prices, particularly for HRC (see left-side chart in Figure 3).

Our MOI also pairs well with our Steel Demand Index (see right-side chart in Figure 3), which, for nearly a decade, has preceded moves in mill lead times. But, again, the latest data denotes a disagreement.

How will things settle?

HRC prices have been on the rise, now up $285 per short ton (st) since late September. And lead times have been steadily stretching out, now at 6.7 weeks on average in our latest assessment, up from 6.5 in early April.

The trend points to a downstream supply chain that’s balanced but lean. Many still see March inventories as aligned with demand, while others worry this tight setup is contributing to rising prices.

If lead times keep stretching, additional spot buying might tip the balance and drive prices higher in the near term.

That tension likely explains why the Mill Order Index remains firm, and our Demand Index continues to expand.

We’ll be watching closely for any shifts as we move deeper into Q2.