HR market looks for deals as prices increase

Sources say domestic mill lead times and consumer spot prices have increased this week.

Sources say domestic mill lead times and consumer spot prices have increased this week.

In the month since my last column, the tides have started to turn – and as usual it wasn’t the physical market that moved first.

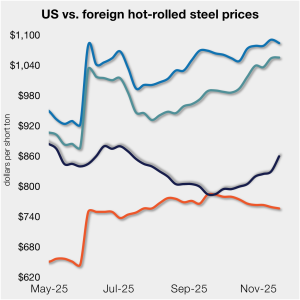

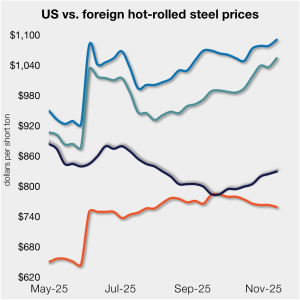

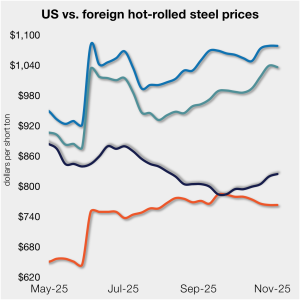

The price gap between stateside hot band and landed offshore product shrank week over week (w/w).

The SMU Steel Demand Index slackened from late October, remaining below expansion territory, according to SMU's mid-November indicators.

SMU’s price indices increased across the board this week, reaching new multi-month highs.

Algoma Steel plans to continue its transition to electric-arc furnace (EAF) steelmaking using the CA$500 million in loans from the Ontario provincial and Canadian federal governments.

SMU’s Mill Order Index (MOI) surged in October after a notable decline the month prior. The recovery came as service center on order inventory totals picked up, supported by a slight uptick in shipments, according to our latest service center inventories data.

US service centers’ flat-rolled steel supply edged lower for the third straight month, reaching 53.3 shipping days of supply on an adjusted basis at the end of October, according to SMU data.

Nucor has increased its consumer spot price (CSP) for hot-rolled (HR) coil for a fourth consecutive week. Now at $910 per short ton (st), up $15/st from last week.

US sheet market participants say demand for hot- and cold-rolled coils has not increased, leaving them confused by mill price increases and average lead times.

Steel mill lead times extended marginally this week on most sheet products but declined for plate, according to responses from SMU’s latest market survey.

Just over half of the steel buyers who responded to our market survey this week reported that domestic mills are willing to talk price on new spot orders. Mills have begun to hold a firmer stance on prices over our last two surveys.

The price gap between stateside hot band and landed offshore product has marginally widened week over week.

NLMK USA is aiming to increase base prices on all products, effective immediately.

The price spread between HRC and prime scrap has widened for a second month, based on SMU’s most recent pricing data.

SMU's sheet and plate steel prices moved higher in unison this week.

Nucor increased its weekly hot-rolled coil spot list price by $5 per short ton on Monday, Nov. 10.

Nippon Steel is making good on the big capex promises it made to secure its purchase of United States Steel Corp. This week, the Japanese company and American steelmaker together unveiled various capital investments they plan to make across U.S. Steel’s footprint.

The gap between US hot band prices and imports narrowed slightly. But with the 50% Section 232 tariffs, most imports remain more expensive than domestic material.

ArcelorMittal Dofasco and Stelco joined recent moves by US mills to push sheet prices higher.

Most sheet prices inched up again this week following mill efforts to set a floor under tags and to increase them from there.

Zekelman Industries said Canadians who report the use of foreign steel in active or future public construction projects are eligible for a CAD$1,000.00 (USD$711.62) payment.

Nucor increases HR spot price by $5/ton

Most steel buyers responding to our market survey this week reported that domestic mills are considerably less willing to talk price on sheet and plate products than they were in recent weeks.

Steel mill lead times marginally extended for both sheet and plate products this week, according to responses from SMU’s latest market survey.

Flack Global Metals (FGM) announced Thursday that it would expand into Texas by assuming the Houston operations of NSPS Metals.

Sheet steel indices increased across the board this week, while plate prices held steady. All five of SMU’s price indices are higher than they were two weeks ago, and all but one are above levels recorded four weeks ago.

President and CEO Eddie Lehner said Ryerson has faced market headwinds in the third quarter.

Nucor entered the fourth quarter with clear forward momentum: stronger-than-expected results, solid sheet and plate demand, and construction progress on a major new mill that should add capacity next year.

Participants on this month’s Heating Air-Conditioning & Refrigeration Distributors International (HARDI) Sheet Metal/Air Handling Council call expect galvanized steel base prices to firm up in the first quarter of 2026.