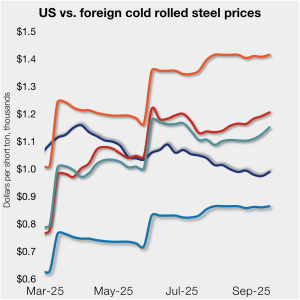

Klöckner sharpens US focus as Americas segment delivers strong Q3

North America continues to anchor Klöckner & Co.’s performance in 2025. The Kloeckner Metals Americas segment delivered robust earnings in the third quarter despite softer steel prices.