Analysis

June 2, 2014

Final Thoughts

Written by John Packard

For those of you who are paying attention to our website you might have noticed we added a new sub-menu under the Resources tab. The new menu is called “The Truth About Selling Steel” and we have attempted to split out those articles associated with sales from our Steel Buyers Basics series of articles many of which were written by Mario Briccetti over the past year and then myself going back in history. The articles are timeless in many ways as they broach subjects buyers and sellers of steel will deal with during their steel careers. I am all fired up to share my thoughts regarding sales as I organize my thoughts in order to present a custom training program on the subject.

Our Steel Summit Conference (September 3 & 4, 2014 – Atlanta, GA) will have a “Pre-Summit” program which will be on the challenges associated with light-weighting and how to deal with thinner (and stronger) steels. The one hour program which we believe will begin at approximately 9:30 AM on September 3rd, will be hosted by Ronald Krupitzer, Vice President Automotive Applications of the Steel Market Development Institute. The Institute has performed a program to large manufacturing companies previously explaining how steels which are being developed for automotive applications can be used in other non-automotive areas. We think that many manufacturing companies as well as service centers who are not yet well versed on the subject will gain valuable insights into the light-weighting process which can then be shared internally within your company or you can work with your steel suppliers to see what opportunities exist for your company. Mr. Krupitzer will remain at the conference to discuss the subject with those who wish to learn more on a one-on-one basis. We encourage you and others from your company to attend our Steel Summit Conferece and join us at the Georgia International Convention Center next to Atlanta’s international airport.

A reminder to all of our member companies – as always each of our programs comes with a discount for SMU member companies. For our Steel Summit Conference the discount off the full package price of $1000 per person is $100 per person and if your company sends 2 or more people there is an additional $100 per person discount which can be applied. The conference is a two day affair and includes lunch, breaks and a cocktail/networking party on Day 1 and a full breakfast, lunch and breaks on Day 2. We anticipate closing the conference around 4 PM ET on Day 2. The Atlanta airport is literally 5-10 minutes away by rail which runs at no charge from the convention center/hotel directly into the airport. You will be able to make a 5:30 PM flight home if you don’t want to stay an extra day in Atlanta to do some business or enjoy the city.

Sponsorships are available and you can learn more about becoming a sponsor, having a product display/sponsor table at the convention center or sponsoring any of the lunches, breakfast, breaks or cocktail party by contacting me at: 800-432-3475 or John@SteelMarketUpdate.com.

To our Premium Level members, you should have received a Premium Newsletter this afternoon with CPIP (Construction Put in Place) and the SMU Key Market Indicators.

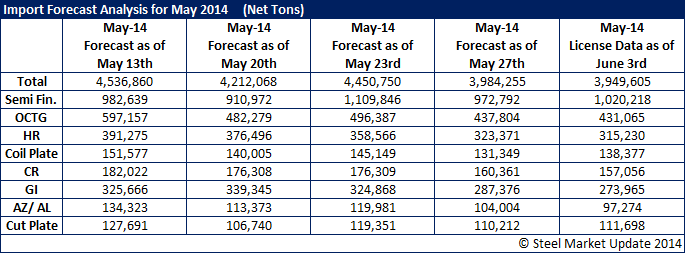

I didn’t get the data crunched until after 5 PM today so I decided to stick the information in my Final Thoughts rather than add a new article. Based on license data through June 3rd (today) May steel imports are projected to be approximately 3.9 million net tons (+/-200,000 tons). April preliminary census data had that month’s imports at 3.7 million net tons. Here is how the license data is breaking out the various products:

Note that semi-finished (slabs) exceeded 1 million net tons. One of our sources who was active in the trading business for many years pointed at AK Steel and told SMU if some of that material went to AK they would most likely put it into commodity products and not automotive. We understand they have caught up on the HR and CR order book…

There has been a lot of talk about more dumping suits against foreign steel. Everyone expects cold rolled and coated to be hit. No one knows when. The countries being bantered about by traders and customers are: China, Taiwan, South Korea and possibly India… When we speak to domestic mills they are mum on the subject or state that they are too small to take that kind of leadership role. Look to US Steel, ArcelorMittal and Nucor to take the lead (if a lead is going to be taken). We are checking on domestic prices in Asia right now to see what we can find out regarding their domestic market prices vs. export prices.

If you have anything on your mind and would like to chat I can be reached at 800-432-3475 or by email at: John@SteelMarketUpdate.com. I will also be in New York City during Steel Success Strategies and I have been invited to the AMM rewards dinner by Andre Marshall of Crunchrisk LLC who was nominated for an award. If you would like to meet with me while in New York shoot me an email: John@SteelMarketUpdate.com to see if our schedules work.

As always your business is truly appreciated by all of us here at Steel Market Update.

John Packard, Publisher

See you in Atlanta in early September?