Market Data

January 4, 2016

Key Market Indicators - December 31 2015

Written by Peter Wright

An explanation of the Key Indicators concept is given at the end of this piece for those readers who are unfamiliar with it.

![]() The total number of indicators considered in this analysis is currently 36.

The total number of indicators considered in this analysis is currently 36.

We have made a change to our analysis this month by removing the capacity utilization of both the flat rolled and long product mills. We have replaced this row in the data sheet with shipments in both cases. We have done this because the calculation of capacity utilization is problematic and find shipment data to be much more factual.

Please refer to Table 1 for the view of the present situation and the quantitative measure of trends.

Readers should regard the color codes in the present situation column as a quick look at the current market condition. The “Trend” columns of Table 1, are also color coded to give a quick visual appreciation of the direction in which the market is headed. All data included in this table was released in December, the month or specific date to which the data refers is shown in the second column from the far right and all data is the latest available as of December 31st.

Present Situation

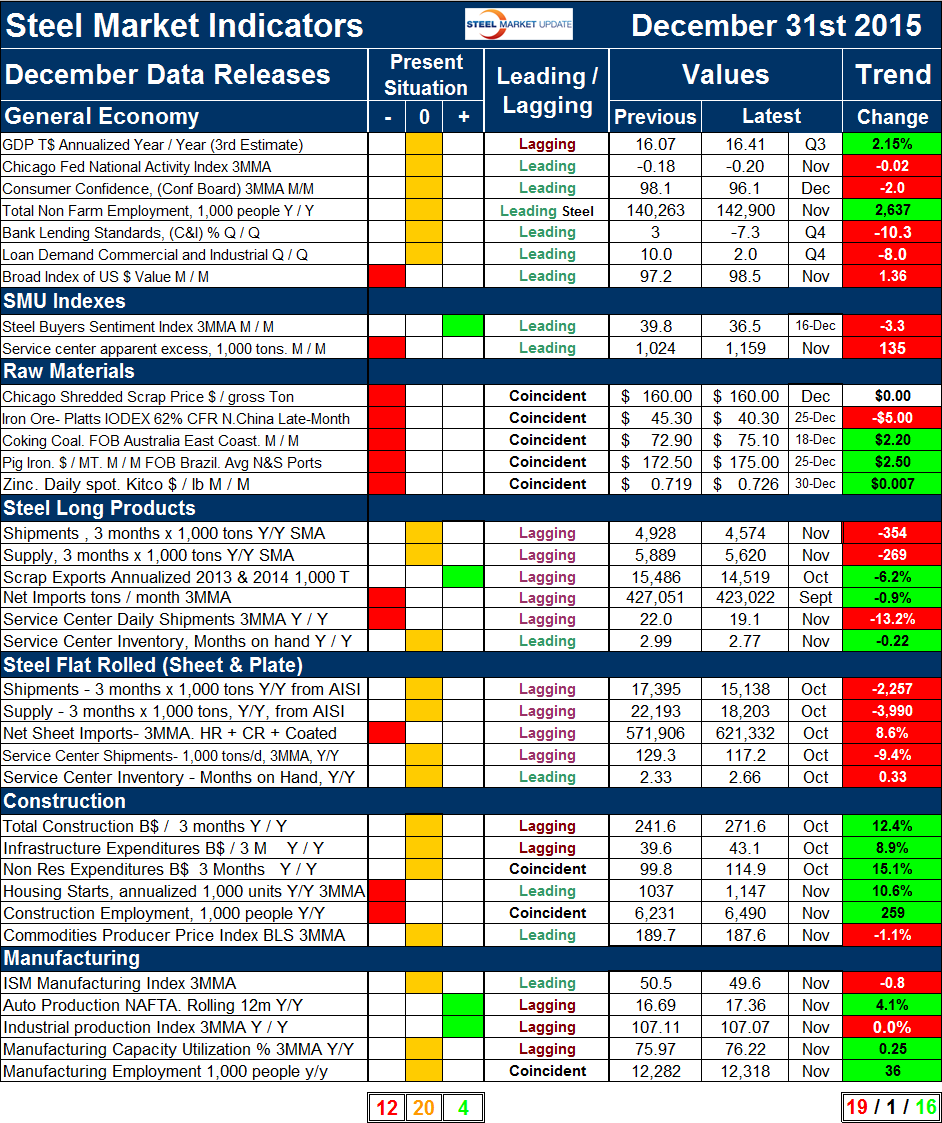

There was a decrease of two negative since we last published this review on November 30th. The number of neutral indicators increased by two. We currently regard 4 of the 36 indicators to be positive, 20 to be neutral and 12 to be negative on a historical basis. Changes in the last month were as follows; the decrease of two negatives resulted from the change in indicators we made from capacity utilization to shipments. We now have 6 years of this analysis and have graphed the changes in the present situation and trends over time. Figure 1 shows the change in our assessment of the present situation since January 2010 on a percentage basis.

The number of indicators classified as positive peaked at 17 in October last year and has steadily declined to the present value of 4 which is 11.1 percent. There has been little or no change in the number of indicators that we consider to be historically negative in the course of 2015, what has happened is that the decline in the positive indicators has occurred as a shift to neutral. The present situation of the general economy with the exception of the value of the US $ is OK. Not great and not unsatisfactory by historical standards. We still regard the proprietary SMU steel buyer’s index as positive though the situation is deteriorating. All the raw materials prices currently have a negative present situation. The present situation of the long products market is marginally worse than for flat rolled, the decider is service center shipments which are historically low for longs but in the normal range for flat rolled. In our analysis here, shipments and supply are based on SMA data for long products and AISI for flat products. SMA gets their data out faster than AISI and longs data is for November and flats for October. There were no changes in our perception of the present situation of the construction or manufacturing industries. IN summary a quick visual appraisal of the present situation shows that the general economy is basically neutral. Steelmaking raw materials are historically weak through December’s data. Both steel sectors are neutral to weak. Construction continues to be weak to neutral and manufacturing continues to be neutral to strong. No indicators are currently rated positive in the construction category. None of the manufacturing indicators on a present situation basis are currently negative.

Trends

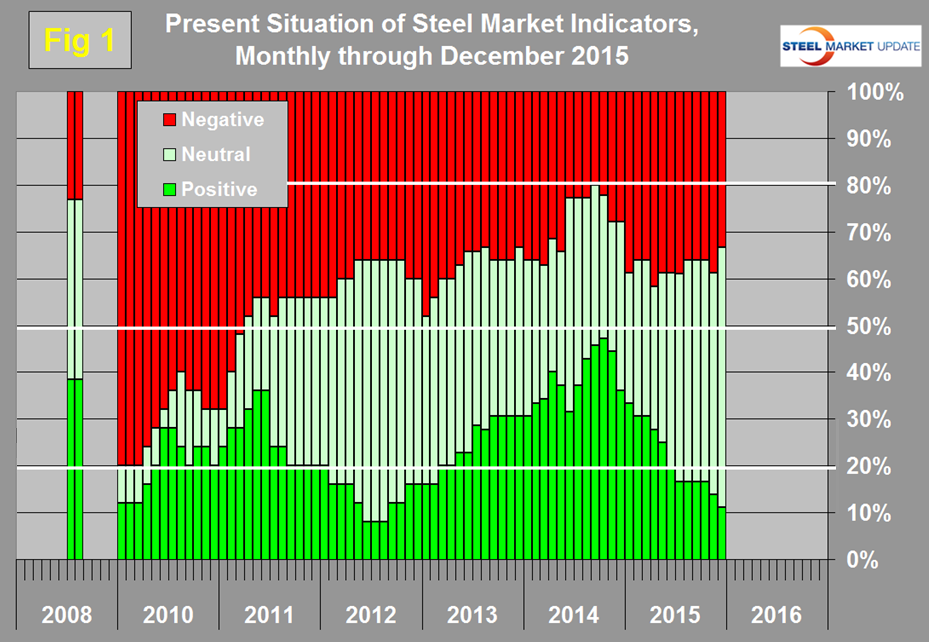

The number of indicators trending positive through December 31st was 16 with 19 trending negative and one unchanged. This was a decrease in one positive and an increase of one unchanged from our November 30th update. Figure 2 shows the trend of the trends.

There has been a steady deterioration since the middle of last year and in the latest two months data the proportion trending positive fell below 50 percent for the first time since March and April 2013. In October last year the proportion trending positive was 80.6 percent which coincided with the highest month of total steel supply since the recession. Figure 2 shows the pre-recession situation at the far left of the chart. In August 2008 over 2/3 (69.2 percent) of our indicators were trending negative and the steel market crashed in September of that year.

Changes in the individual sectors are described below. (Please note in most cases this is not December data but data that was released in December for previous months.)

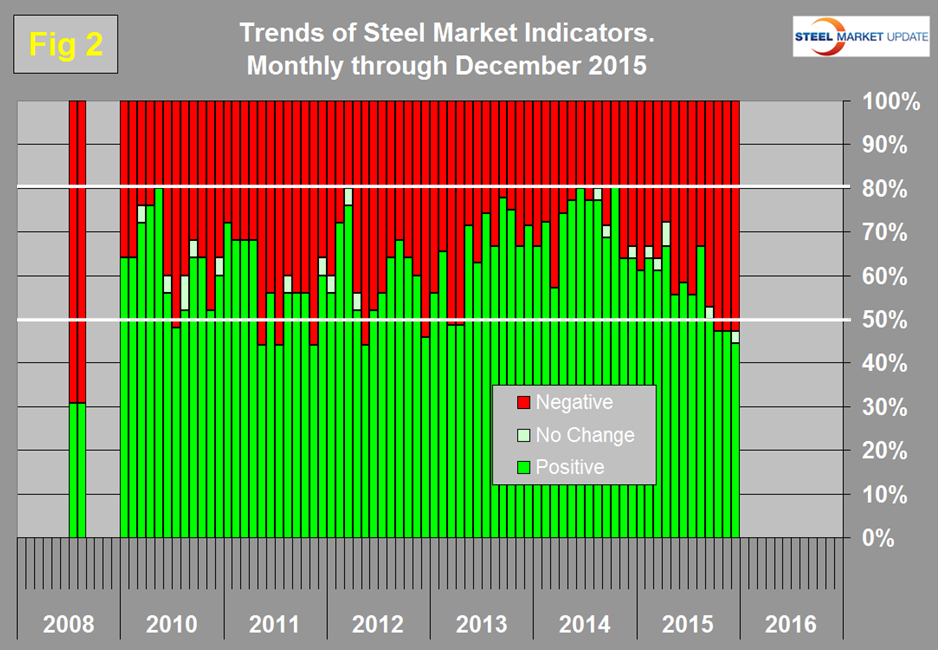

There was one change to the direction of trends in the general economy. The value of the US $ declined (positive change) in October but increased in November as the long term trend re-established itself. We regard a weakening dollar as positive because of its effect on net imports. The trend of the Steel Market Update buyer’s sentiment index continued to be negative with a three month moving average of 36.5 on December 17th but as shown in Figure 3 is still at a historical good level.

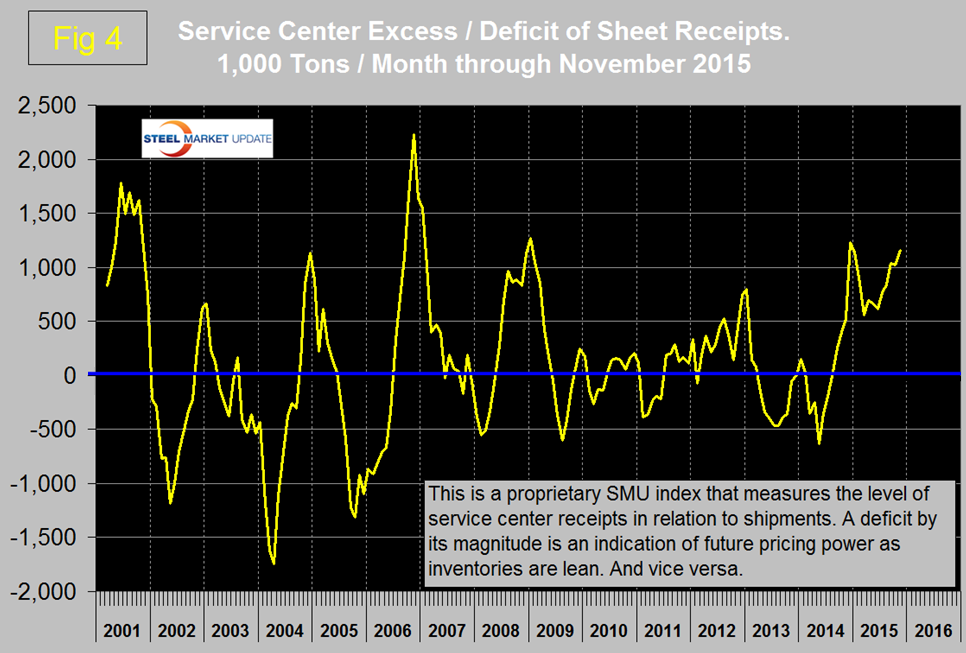

The calculation of service center excess inventory of sheet products which had trended positive in the October data trended negative in November. We regard this inventory level as a leading indicator of weak pricing power (Figure 4).

There were improvements in the trends of raw materials prices in December. The price of Chicago shredded which had declined in November was unchanged in December. Coking coal and zinc both had small price increases which were trend reversals. The price of iron ore continued to decline. In the long product section, service center inventory which had been trending negative in October reversed course in November. All five indicators of the flat rolled sector trended negative in the latest data which was an increase of one. In our last report, net imports had been trending positive. There was no change in direction of trends of the construction sector. Manufacturing had an increase of one negative trend. This was in the industrial production index which contracted by 0.04 percent year over year. It has been obvious for most of this year that manufacturing was slowing but this was the first time that the IP index had had negative year over year growth since February 2010.

We believe a continued examination of both the present situation and direction is a valuable tool for corporate business planning.

Explanation: The point of this analysis is to give both a quick visual appreciation of the market situation and a detailed description for those who want to dig deeper. It describes where we are now and the direction in which the market is headed and is designed to give a snapshot of the market on a specific date. The chart is stacked vertically to separate the primary indicators of the general economy, of proprietary Steel Market Update indices, of raw material prices, of both flat rolled and long product market indicators and finally of construction and manufacturing indicators. The indicators are classified as leading, coincident or lagging as shown in the third column.

Columns in the chart are designed to differentiate between where the market is today and the direction in which it is headed. Our evaluation of the present situation is subjectively based on our opinion of the historical value of each indicator. There is nothing subjective about the trends section which provides the latest facts available on the date of publication. It is quite possible for the present situation to be predominantly red and trends to be predominantly green and vice versa depending on the overall situation and direction of the market. The present situation is sub-divided into, below the historical norm (-) (OK), and above the historical norm (+). The “Values” section of the chart is a quantitative definition of the market’s direction. In most cases values are three month moving averages to eliminate noise. In cases where seasonality is an issue, the evaluation of market direction is made on a year over year comparison to eliminate this effect. Where seasonality is not an issue concurrent periods are compared. The date of the latest data is identified in the third values column. Values will always be current as of the date of publication. Finally the far right column quantifies the trend as a percentage or numerical change with color code classification to indicate positive or negative direction.