Market Data

January 21, 2016

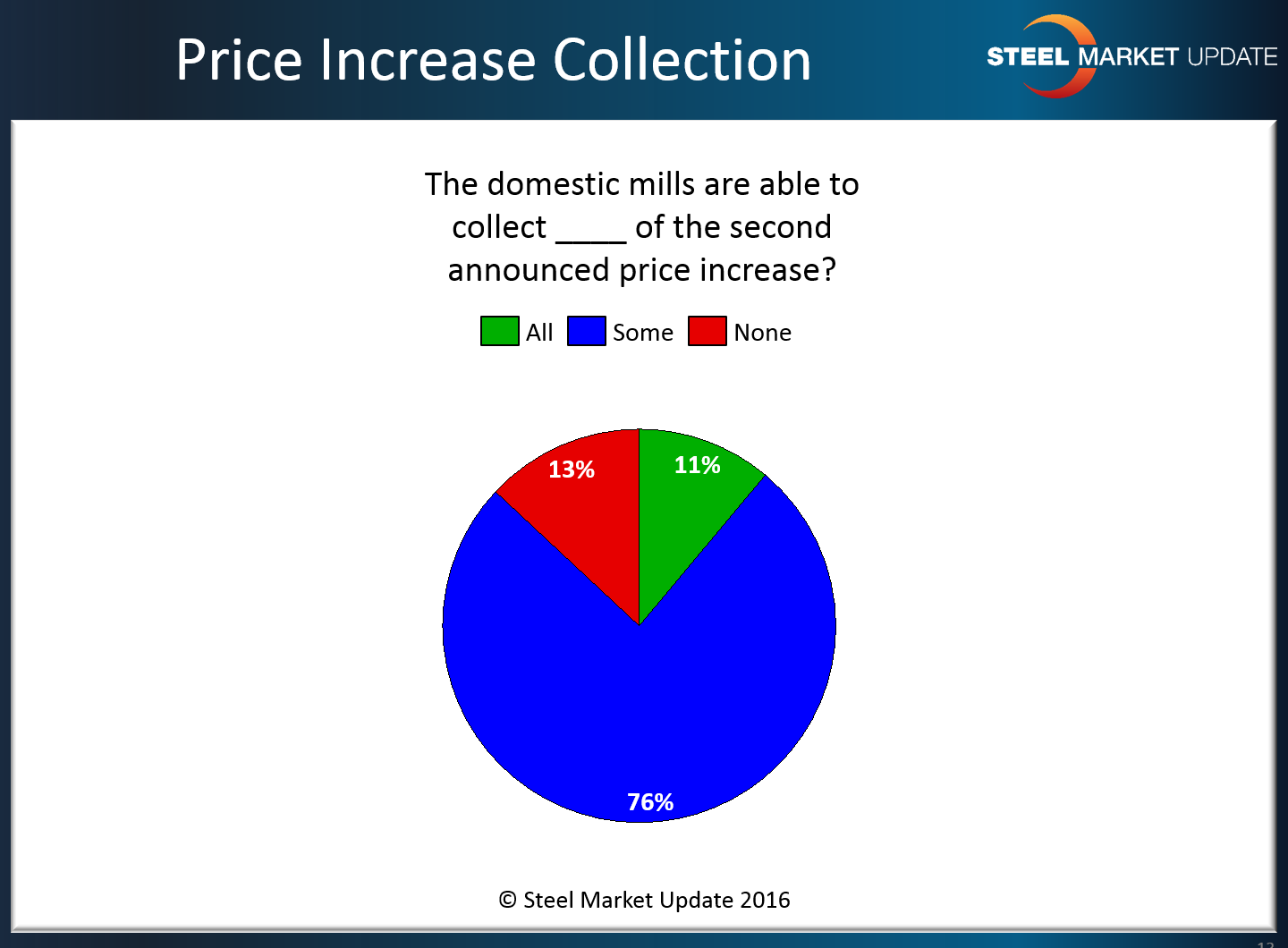

SMU Survey: How Much of 2nd Price Increase Will Stick?

Written by John Packard

The vast majority of the respondents to our latest flat rolled steel market analysis believe that the domestic steel mills will be able to collect “some” of the latest round of price increases which range from $20 to $30 per ton.

In our latest assessment of the flat rolled market, we asked whether the domestic mills will be able to collect all, some or none of the January price increase. Seventy-six percent of respondents said that the mills would be able to collect some of the increase, 11 percent thought all of the increase would be collected, and 13 percent thought none of it would be collected.

What Our Respondents had to Say

“ArcelorMittal explained their price increase as follows: “These increases are necessary in order to restore some level of profitability to our business. We have experienced an increase in order entry of products due to a reduction in inventories and the continued strength of the consumer driven industries, automotive and appliances”. That strikes me as a lame reason. And combine that with: the big gap between domestic and foreign, rising imports, and still low capacity leaves me questioning whether the fundamentals are there for this 2nd increase.” Wholesaler

“All or most on crc/galv not so confident about hrc.” Service center

“They will announce a 3rd increase late Jan or Early Feb and that will give them the ability to collect the 2nd increase.” Trading company

“Too much too fast will push customers back to imports &/or drive competition for available tons between domestic producers… either way deflating likelihood of sustained price increases.” Manufacturing company

“Doesn’t appear to be much will be collected but prices are slowly solidifying.” Service center

“The mills need to be very careful here. They are pricing in the effect of preliminary AD/CVD which totaled between $60 and $80/ton. All the domestics are doing here is allowing the foreign V domestic spread to remain constant and are giving away all of their advantage. In short, if they aren’t careful, they will encourage domestic customers to continue buying foreign steel.” Manufacturing company

“I continue to hear from other Purchasing personnel that their business is picking up and they ran their inventories down too much. I have been selling coils to some to supply their needs which is very uncommon.” Manufacturing company

“If mills issues continue to sprout up, then they will get closer to all.” Service center

“$20 out of the $70 announced in the last month.” Manufacturing company

“I don’t believe they collected the first increase yet.” Manufacturing company