Prices

January 26, 2016

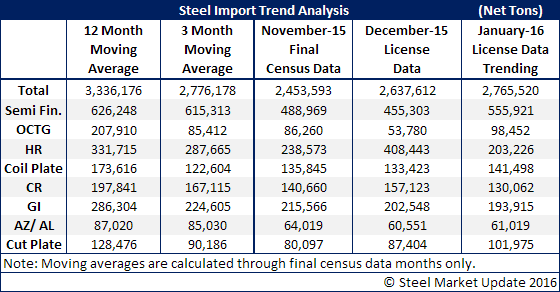

January Imports Trending Toward 2.7 Million Tons

Written by John Packard

The U.S. Department of Commerce released foreign steel import license data through the 26th of the month late this afternoon. Based on the data to date, January imports are trending toward a 2.5 to 2.7 million net ton level. This would be slightly higher than December’s 2.6 million tons and above November’s 2.4 million tons.

As you can see by the table below, January should come in close to the 3-month moving average but well below the 12 month moving average.

As we look at the four main carbon sheet groups: hot rolled, cold rolled, galvanized and Galvalume (other metallic), each group is trending below both the 3MMA and 12MMA for their product. Hot rolled is down significantly as is cold rolled. Galvanized appears to be making a bottom (going as low as it is going to for awhile).

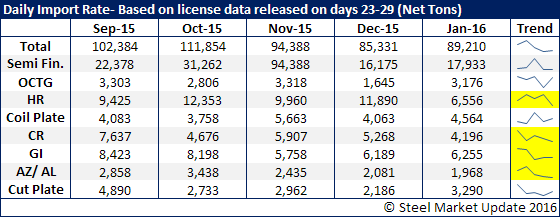

We can better see the trend for each product by reviewing the daily shipment analysis that we do on a weekly basis (not always published).

On Thursday we will look a little deeper into the various countries to see if the trade suits are making a difference (and who is taking their place).