Market Data

February 4, 2016

The Story Behind this Market: Steel Mill Lead Times

Written by John Packard

Many of you have read that hot rolled is the weakest product and that there is a significant spread between domestic hot rolled base prices and those of cold rolled and galvanized steel. Even with the energy markets being in the so-called “crapper” impacting the hot rolled order books, we are seeing stronger steel mill lead times than what we collected in early December as well as what we saw one year ago. It is our opinion the extended lead times are the result of less supply (both domestic and foreign) and a need by the manufacturers and service centers to begin to build back inventories.

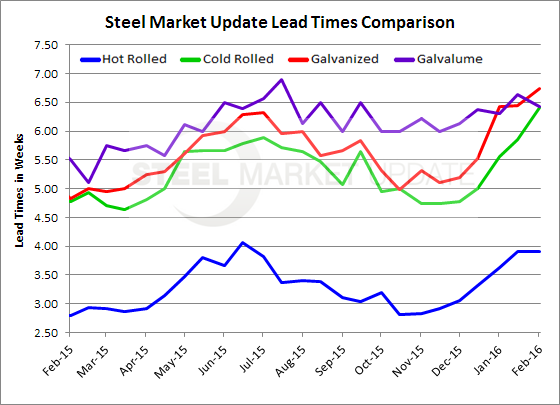

The following lead times on hot rolled, cold rolled, galvanized and Galvalume are from the data collected this week during our flat rolled market trends analysis. Do not confuse these lead times (which are averages of the total responses collected by product) with the published mill sheets or what you may receive from your mill supplier. We report on those lead times separately and did so in the last edition of Steel Market Update.

Hot rolled lead times are averaging 3.9 weeks (essentially four weeks) according to our respondents to this week’s questionnaire. This is the same as what we collected during the middle of January and is one week extended compared to November 2015 as well as the first week of February 2015.

Cold rolled lead times appear to be moving out faster than hot rolled and are now averaging 6.41 weeks according to this week’s respondents. This is one week longer than what we saw one month ago and almost two weeks longer than November 2015 and February 2015.

Galvanized lead times moved out again this week and are now averaging 6.74 weeks based on our respondents. This is 1.5 weeks longer than what we saw in November and essentially two weeks longer than what we measured one year ago.

Galvalume lead times did not move out and have remained relatively stable at 6.43 weeks since the beginning of December (there is seasonality which needs to be considered with AZ products). However, Galvalume lead times are one week longer than what we saw for an average one year ago.

To see an interactive history of our Steel Mill Lead Time data, visit our website here.