Prices

February 11, 2016

Hot Rolled Futures: Pit in Your Stomach

Written by Andre Marshall

The following article on the hot rolled coil (HRC), busheling scrap (BUS), and financial futures markets was written by Andre Marshall, CEO of Crunch Risk LLC and our Managing Price Risk I & II instructor. Assisting Andre with tonight’s article is Jack Marshall also associated with CrunchRisk. Here is how Andre and Jack saw trading over the past week:

Financial Markets

The S&P 500 is in midst of retesting recent lows and has broken them by a smidge today, essentially testing the 1800 zone, the low on the March future was 1802.5 and the low on the S&P index was 1810 zone – the most recent last low was 1814 as reference. As I have mentioned, we are likely headed for that 20% correction area of 1700-1750, and maybe lower, however, the next move may be back up to 1900 area, basis the March future price, with first resistance at 1840.

We’re more or less about the halfway point on this current downward larger correction, and so now is not really a good time to lighten up if you haven’t already. At the correction point, 20% or 25% or 30 %, we will then rally hard again looking to retest the old highs at X number of weeks or months forward. Where-ever we may be “when?” we fail to test those old highs, is the best moment to lighten up – you just have to remember the “pit in your stomach” feeling you have right now to lighten up when it’s sounding all bullish again then, haha! – good luck with that.

In 2013 Ray Dalio, founder of Bridgewater Capital, at one time the largest hedge fund in the World, published a 30 minute video on You Tube called “How the Economic Machine Works: A Template for What is Happening Now”. In this video is a very simple and clear description of how our economy works. Although animated and basic, it is eerily prescient for today’s environment, and, in a very 30K foot kinda way, possibly showing us what that “pit in stomach” feeling is all about. Here’s the link. Definitely worth the time if you haven’t seen it.

In Copper, you might remember we were hovering just above $2.00/pound. Back in mid-Jan we tested the support at $2/lb., breached it briefly and then rallied from there to recent highs at $2.1335/lb. zone to only retrace back down to, you guessed it, right above $2/lb. At the last we are trading either side of $2.01/lb. In Crude, ok everyone hold their breath, we have broken $30/bbl. back on the 9th, and are hovering around $27.30/bbl. last after recent low point of $26.05 bbl. on the March future.

Finally, just some thoughts on the current situation, where the media and professionals alike, all appear ready to jump off a bridge. I agree the world looks precarious, but I’d point out it has done so for over a year now if you’ve been paying attention, or reading my dittys. Usually when the media hypes an idea the idea is close to finished. Hopefully this is true this time again, and we round the bend on some of these global issues soon. No argument that China, BRIC countries and others look weak, and our manufacturing companies feed into those economies. However, I would point out that stock prices would be affected more by this than the U.S. economy itself for manufacturing is already a sub 20% contributor to our GDP, and that which is exported is even less.

Further, with decent job growth here and early stages growth in construction, we may still have some legs here in the U.S. Further still, manufacturing in the U.S. has suffered in the last 20 years for the high costs in critical components like plastics, and labor, which, guess what?, are cheaper to produce and deliver here now than just about anywhere else in the World, and so Petrochemical plants here are booming, and expanding. And let’s not forget the $650-$1500/family per year savings on all the low cost energy effect from the gas pump, electric bill and heat bill. We are not an Island, but it doesn’t mean that the World’s issues translate dollar for dollar here. As a free market based economy (until Bernie or Trump or elected anyway) that has already had its difficult culling and trimming and $ printing from the financial crisis period, we may well have some legs left! I’ll be the contrarian, again! And say I think business in 2016 surprises our industry.

Steel (HRC)

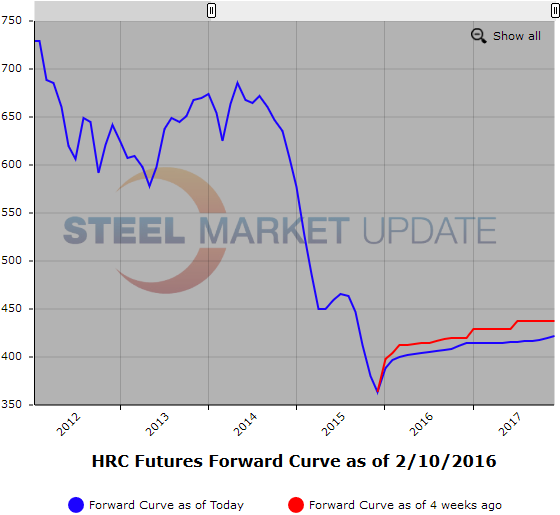

This was an active week in hot rolled (HRC) futures as sellers continued to compress the forward curve by selling the back end of the forward curve. 36,000 short ton (1,800 contracts) traded Tuesday ahead of Wednesday’s index release which was reported up $8 from the previous week to $399 ST. Toward the back end of the forward curve Jan/Sep’17 traded on Tuesday @$415 ST[$20.75cwt] followed today @ $412 ST[$20.60cwt] which is $9 below Monday’s settlement value.

The middle of the forward curve also traded lower as Apr’16/Feb’17 traded @ $410 ST[$20.50cwt] which was slightly below Monday’s settlement value, however on the follow Apr/Dec’16 traded @ $405 ST [$20.25cwt] which was $4 below Monday’s settlement value. Today Q4’16/Q1’17 traded @ $409 ST[$20.45cwt] pushing values lower yet again.

We are not sure what is driving the selling. Market sentiment seems to have shifted this week even as the HR index rose close to $20cwt. HR forward market appears to reflect contagion concerns related to distressed global equity markets and weak oil prices.

HR interests:

Apr/May’16 $400 bid on 1,000 ST/month

Oct’16/Mar’17 $408 bid on 500 ST/month

Open Interest 24,716 contracts or 494,320 short tons (2,000# is one short ton).

February 2016 month to date HRC futures trading activity 4,167 contracts or 83,340 short tons traded.

Busheling Scrap (BUS)

Lukewarm sentiment continues to plague U.S. scrap markets as weak global growth, declining oil prices and US dollar strength continue to disrupt domestic scrap market pricing. In Midwest busheling scrap (BUS) futures we have not seen any bids of late. The BUS index settled yesterday @ $180.58 basically sideways to last month which appears to be due to the abundant supply of prime scrap from the strong auto manufacturing sector and measured mill purchasing.

We are currently offering:

Mar/Jun’16 @ $190 GT on 240 GT/month

2H’16 @ $215 GT on 500 GT/month

Below is a graphic of the HRC Futures Forward Curve. The interactive capabilities of the graph can only be used in Steel Market Update website here. If you have any issues logging in or navigating the website please contact us at info@steelmarketupdate.com or (800) 432 3475.