Prices

March 3, 2016

February Imports at Lowest Levels Since December 2011

Written by John Packard

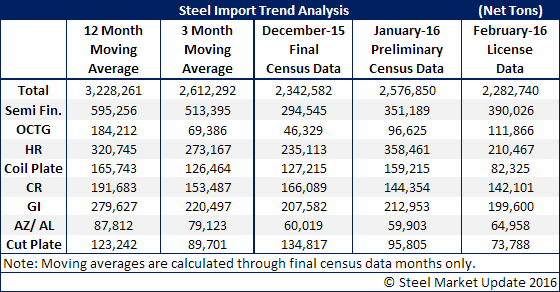

Steel Market Update had to go back into our records to dig out when foreign steel imports were reported to be less than 2.3 million net tons. The reason we were searching was based on our analysis of the U.S. Department of Commerce foreign steel import license data released earlier this week.

Based on license data collected through the 1st of March, February imports are expected to be 2.3 million net tons. The last time the United States saw imports that low (or lower) was December 2011 when 2,064,143 net tons were reported.

The February 2016 number is based on import license data and everyone needs to understand that actual receipts could be higher or lower than the import licenses (+/- 200M). What we have seen happening over the past couple of years is the actual receipts have been coming in lower than the license data for that month. Whatever the final tally, it will be at least 1.2 million net tons lower than the 3.7 million tons received during February 2015…

The trade suits against hot rolled, cold rolled and corrosion resistant steels are having an impact. Hot rolled imports are down and will continue to move lower as the preliminary determination ruling on antidumping (AD) will be announced on the 15th of March.

Cold rolled seems to have stabilized around 140-150,000 tons per month.

At 199,600 net tons, galvanized is down 150,000 tons from the peak seen during the 2nd Quarter 2015.

Galvalume tonnage is down approximately 30-40,000 tons from its peak. However, some of this is a seasonal adjustment so we will need to watch the numbers closely over the next few months.