Prices

March 20, 2016

Platts HRC Index: Methodology, Daily, Exchange Ready

Written by John Packard

The following article was written by SMU founder and publisher, John Packard with the assistance of Platts Content Director, Metals Americas, Joseph Innace.

Shortly after Steel Market Update (SMU) became a real company I understood the need for the flat rolled steel industry to have an pricing index which was independent and not tied as a financial instrument for the futures markets or used as a basis for contracts between customers and suppliers. Our hot rolled, cold rolled, galvanized and Galvalume indices was created so buyers and sellers have something to reference that comes from an experienced steel person utilizing my vast network of steel buyers in order to gather market intelligence which is believable.

When I was selling steel as an agent for Winner Steel (now NLMK USA Sharon Coatings) I recognized the need for a quality index to keep track of “real” selling prices. It was quite difficult to be a mill representative and have to deal with either incorrect information being leaked into the market or having to spend much of my time explaining why the market periodicals of the day were outside of the true market pricing which at the time were in a constant state of volatility. I became an early supporter of a specific index as it was the only clear choice at that point in time.

Since then other options have become available and I think buyers and sellers (as well as the financial exchanges) need to be aware of what options are out there, what their strengths and weaknesses may be and buyers and sellers need to understand there are options that may be more transparent than what you may be using now. When negotiating steel prices be aware that the index to be used as the reference point can also be negotiated.

Earlier today I asked Joe Innace of Platts if he could explain why there is a fairly wide variance in the pricing being referenced on benchmark hot rolled coil by various indices.

He told us, “I think, possibly, two main things could explain the difference:

1. Platts’ assessment is based on what we consider typical quantities purchased for today: up to 500 st. There are now many buyers ordering 50 st, 100 st, 250 st, etc. — Regardless of company size, many — small and big players —participate in our survey and deserve a voice. Large buyers alone do not reflect the market, and Platts also does no weighted averaging.

2. Repeatability. A one-off, “special relationship” deal would not be considered in Platts’ assessment. I cannot say for sure [another index name removed] accepts and includes such data, but if so, this would explain the difference.”

Here is what Joe Innace shared with Steel Market Update about their methodology and price assessments which are used to settle 19 different financial contracts around the world:

Five Core Principles of Platts Price Assessment Methodology:

1. IMPARTIAL AND INDEPENDENT

Platts has no vested interest in whether an assessment is priced high or low, which is critical to our responsibilities in establishing a market value.

2. PRICE: A FUNCTION OF TIME

We mark a price at a specified time (example: 3:30 PM, every day, for US hot-rolled coil). Having a price at a single point in time enables us to compare related steel products on an equal footing (normalization). Platts can then better provide a neutral price to market participants who are all aware of the same timing, specifications and standards.

3. REPEATABILITY

For a price to be considered in a Platts assessment, it cannot be a one-off, or specialized deal. We must be confident it reflects a market-at-large value.

4. PROCESSES ARE OPEN AND TRANSPARENT

The Platts price discovery process is built around the notion of testing a price in the market. We publish bids and offers in real-time and we also discuss what we are hearing with active market participants. The reaction to such information is critical in determining the value of our steel product assessments. We also write a market commentary underpinning the price assessment with color and insight from buyers and sellers and other market players. In cases where prices are used to settle derivatives contracts on Exchanges, Platts also publishes a daily Assessment Rationale, which discloses the data points used to form our assessment.

5. METHODOLOGY BASED ON MARKET FEEDBACK

Platts works very closely with the market on a continual basis to ensure that what we are publishing reflects the market-at-large. Platts is transparent in setting out what we are assessing and publish that publically for all to see (subscribers or not—as all methodologies are available for downloading at platts.com). We welcome feedback on market dynamics, trade shifts, changing buying/selling habits on an ongoing basis. If we think it’s time to change a methodology – any specification that may have a material impact on the value assessed — we let the market know in advance and provide an ample feedback period for comments, suggestions and other insights.

Our methodologies are all available for review at platts.com (no need to be a subscriber): http://www.platts.com/methodology-specifications/metals

Most of our benchmark prices are daily because:

1) In the case of those used to settle derivatives contracts on exchanges, daily frequency is preferred.

2) We need to be in the market each day, surveying participants, because the price can move on any given day at any given time.

3) Even in the case of less-active markets, there is still a price value every day. There is a level at which a buyer would or could buy at, and a level at which a seller would or could sell at. Consider this: Your house may be up for sale at $500k. Three other, similar houses on the block are also for sale, in a range from $480k-$520k. Those houses may not sell tomorrow, and might not even see any offers tomorrow. No one might attend the open houses. But we know they have a price, in this case somewhere around $500k—and we know a person could transact at that price.

Usage in Financial (derivatives) Contracts

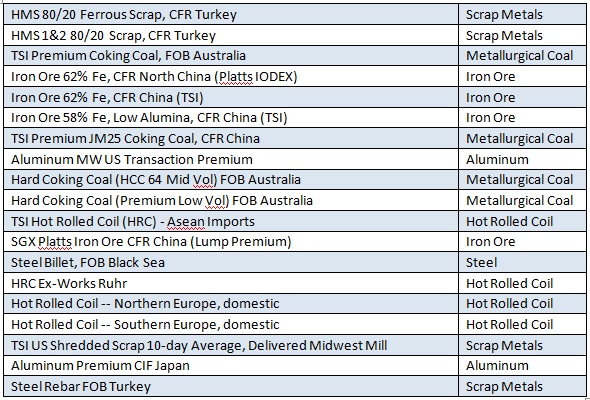

Below is a listing of all Platts Metals benchmarks (19 and growing) that are used to settle/clear contracts on several major exchanges—including the Singapore Exchange, CME Group, and the London Metals Exchange (LME).

As for transparency, for all of the above (Platts’ prices used to settle exchange contracts), a daily assessment rationale is published, explaining how we determined the spot price.

For example, here is the assessment rationale for our Platts IODEX (iron ore) price for March 8. This is published real-time (Platts Metals Alert) and also in Platts Steel Markets Daily—as are several other ferrous scrap, met coal and finished steel assessment rationales:

IODEX 62% Fe Assessment rationale March 8, 2016

Platts assessed the 62% Fe Iron Ore Index at $62/dry mt CFR North China, down $2.20/dmt on Monday.

Australian miner Rio Tinto was heard to have offered 61% Fe Pilbara Blend fines at $63.40/dmt CFR Qingdao on COREX. The 170,000 mt parcel will load March 29-April 7.

Taking into account the iron content, impurity adjustments, timing and 15 cents/dmt premium that PB fines currently command over other brands, the PB fines offer normalized to $64.61/dmt against IODEX specifications.

The counterbid stood at $61/dmt CFR Qingdao on COREX, which normalized to $62.17/dmt against IODEX specifications.

Another parcel of 62% Fe Pilbara Blend fines was offered at $61/dmt CFR Qingdao on globalORE. The 170,000 mt parcel will arrive China in April.

The offer normalized to $61.48/dmt CFR Qingdao against IODEX specifications, and counterbid stood at $57/dmt CFR Qingdao on the platform.

Early in the day, a parcel of 62% Fe Pilbara Blend fines was traded at $64/dmt CFR Qingdao on globalORE. The 170,000 mt shipment will arrive China in April.

No market data was excluded from the March 8 assessment process.

Such assessment rationales are published to comply with IOSCO Price Reporting Agency Principles. IOSCO stands for International Organization of Securities Commissions.

Platts’ aim is to build awareness among various stakeholders of its role in the commodity markets, its price assessment processes and how they protect against distortion of its price assessments. Here you will find facts about Platts as well as Platts’ responses to several regulatory consultations and media reports: http://www.platts.com/regulatory-engagement

Ernst & Young also conduct an annual independent audit of all Metals benchmarks. Two EY assurance reviews now have found Platts aligned with IOSCO principles. The audit report is also accessible at the link above.

One final point: As noted previously, Platts’ prices are used by many exchanges. You asked specifically about The CME Group, which settles and clears more than 720 contracts based on spot market price assessments published by Platts (across all commodities).

Not among those 720, however, is CME Group’s US Midwest Domestic Hot-Rolled Coil Steel futures contract that uses CRU pricing as the basis for settlement. The Platts US hot-rolled coil daily price assessment, as well as Platts-owned TSI’s US hot-rolled coil price, are also widely referenced in physical market contracts. The Platts and TSI prices are robust, subjected to compliance rigor, and always regulatory-ready.

If you have a question you would like to ask Platts about their methodologies, an example of the transparency of their hot rolled or other price index or anything else he can be reached at: joseph_innace@Platts.com