Prices

March 29, 2016

SMU Price Ranges & Indices: Continued Firming

Written by John Packard

Flat rolled steel prices continue to firm and many buyers are convinced there could be more price increases to come with a tightening foreign market and higher offers for foreign steel coupled with the expectation that ferrous scrap prices will increase by a minimum of $30 per gross ton for April delivery.

SMU has been learning of “holes” in some service center inventories, especially for traditional mill items (not 48″, 60″ or 72″). A number of distributors reported brisk service center sales or requests for quotes although not all service centers were willing to sell off what is becoming more valuable inventory as each week passes. Our HRC average price is now $80 per ton higher than where we were at the beginning of December. Galvanized prices have done even better improving by $137 per ton since early December.

With scrap poised to move higher in April, supply constrained, inventories down at service centers and foreign prices rising we have our Price Momentum Indicator set at Higher as we expect prices to continue to rise over the next 30 days.

At this moment here is how we see spot flat rolled prices this week (all prices shown are in net tons which are equal to 2,000 pounds):

Hot Rolled Coil: SMU Range is $420-$460 per ton ($21.00/cwt- $23.00/cwt) with an average of $440 per ton ($22.00/cwt) FOB mill, east of the Rockies. Both the lower and upper ends of our range remained unchanged compared to one week ago. Our overall average is the same as it was last week. SMU price momentum for hot rolled steel has prices rising over the next 30 days.

Hot Rolled Lead Times: 4-7 weeks.

Cold Rolled Coil: SMU Range is $600-$630 per ton ($30.00/cwt- $31.50/cwt) with an average of $615 per ton ($30.75/cwt) FOB mill, east of the Rockies. The lower end of our range remained the same compared to last week while the upper end increased $10 per ton. Our overall average increased $5 per ton over one week ago. SMU price momentum for cold rolled steel is for prices to increase over the next 30 days.

Cold Rolled Lead Times: 5-8 weeks.

Galvanized Coil: SMU Base Price Range is $30.00/cwt-$32.00/cwt ($600-$640 per ton) with an average of $31.00/cwt ($620 per ton) FOB mill, east of the Rockies. The lower end of our range increased $5 per ton compared to one week ago while the upper end increased $10 per ton. Our overall average is up $7.50 per ton over last week. Our price momentum on galvanized steel is for prices to move higher over the next 30 days.

Galvanized .060” G90 Benchmark: SMU Range is $660-$700 per net ton with an average of $680 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 6-10 weeks.

Galvalume Coil: SMU Base Price Range is $30.50/cwt-$32.00/cwt ($610-$640 per ton) with an average base of $31.25/cwt ($625 per ton) FOB mill, east of the Rockies. Both the lower and upper ends of our range are the same compared to last week. Our overall average is unchanged over one week ago. Our price momentum for Galvalume steel is currently pointing towards an increase in prices over the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU Range is $901-$931 per net ton with an average of $916 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 5-9 weeks.

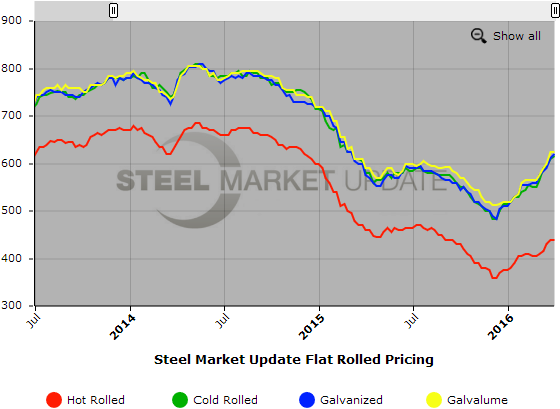

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, and Galvalume price history. To use the graphs interactive capabilities, you must view it on our website here. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or by calling 800-432-3475.