Prices

May 18, 2017

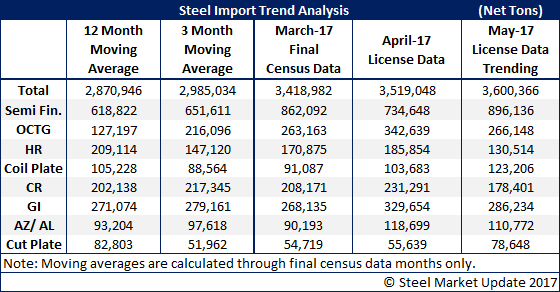

May License Trend is Indicating a Big Month for Foreign Steel Imports

Written by John Packard

The U.S. Department of Commerce (DOC) reported foreign steel import license data earlier this week. Based on the daily rate and projecting it over the course of the entire month of May we are anticipating another 3.0 million net ton month. As of the 17th of May the trend is for imports to be close to the 3.4 and 3.5 million net ton levels seen in March and April 2017.

The steel mills continue to be the largest importers of foreign steel with the data suggesting semi-finished steels (slabs/billets) will be around 800,000+ net tons. When adding some of the hot rolled and cold rolled being imported, also belonging to the domestic steel mills, the mills may actually be importing almost a third of the foreign steel coming into the country in May.

We are also seeing a surge of imports of oil country tubular goods (OCTG) and Galvalume. High imports are also expected on galvanized.

Lower imports appear to be happening on hot rolled and cold rolled.