Market Data

July 9, 2017

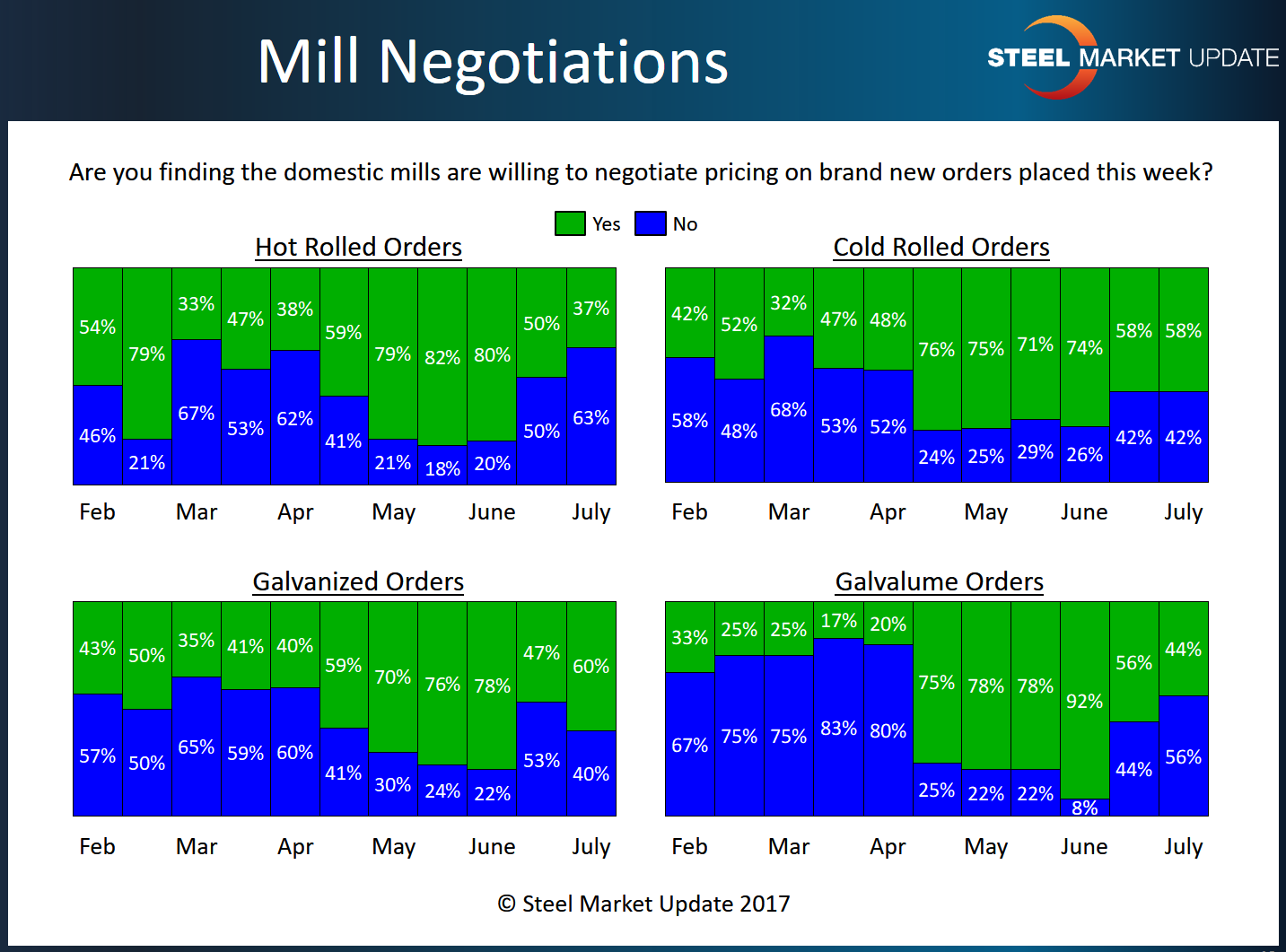

Steel Mills Divided on Negotiating Flat Rolled Prices

Written by Tim Triplett

We saw steel mill lead times as being essentially the same to slightly higher than what we measured at the time of the last price increase announcements (week of June 5th). When the announcements were made, most steel mills were actively trying to collect increases. We saw the bottom of our price range rise, and steel price averages have slowly risen with hot rolled coil now topping $600 per ton (average). Those responding to last week’s flat rolled steel market trends survey reported a weakening in the negotiation positions on hot rolled and Galvalume and strengthening of their resolve on cold rolled and galvanized.

Steel Market Update found 37 percent of hot-roll buyers, 58 percent of cold roll buyers, 60 percent of galvanized buyers and 44 percent of Galvalume buyers report that domestic mills were willing to negotiate pricing on new orders placed this past week. Those percentages are down considerably from SMU surveys dating back to May 1 (prior to June 5th price announcement) when 70-80 percent of respondents found mills willing to discuss price.

Steel Market Update sends an invitation to participate in our flat rolled steel market trends questionnaire to active flat rolled and plate steel buyers twice each month. The data we report for both lead times and negotiations comes from steel service center and manufacturing respondents. We do not include commentary from the steel mills, trading companies or toll processors.

SMU surveys active steel buyers twice each month to gauge the willingness of their steel suppliers to negotiate pricing. The results reflect current steel demand and changing spot pricing trends. SMU provides our members with a number of ways to interact with current and historical data. To see an interactive history of our Steel Mill Negotiations data, visit our website here.