Market Data

September 28, 2017

Consumer Confidence Still Encouraging

Written by Peter Wright

Consumer confidence dipped slightly in September, but continues to be encouraging for the U.S. economy, according to The Conference Board Consumer Confidence Index.

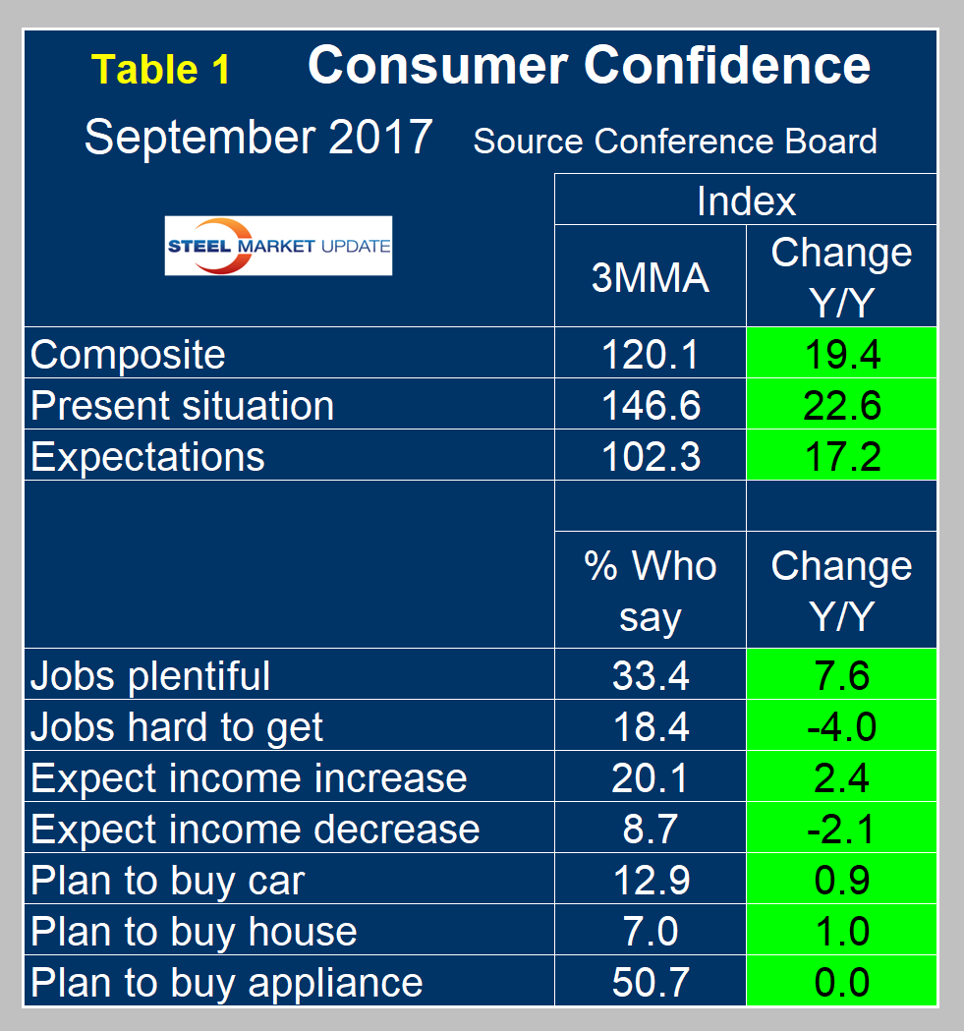

The composite value of consumer confidence in September was 119.8, down from 120.4 in August. The first estimate for August was revised down from 122.9. The last seven months have each been better than at any time since 2001. The three-month moving average (3MMA) increased from 119.2 in August to 120.1 in September, which was 19.4 points higher than in September last year. Consumers’ view of the present situation declined slightly in September. Consumer confidence is the driver of consumer spending, which is the largest component of GDP and which ultimately drives a large portion of steel consumption.

The source of this data is The Conference Board with analysis by Steel Market Update. See the end of this piece for The Conference Board’s news release and an explanation of the indicator.

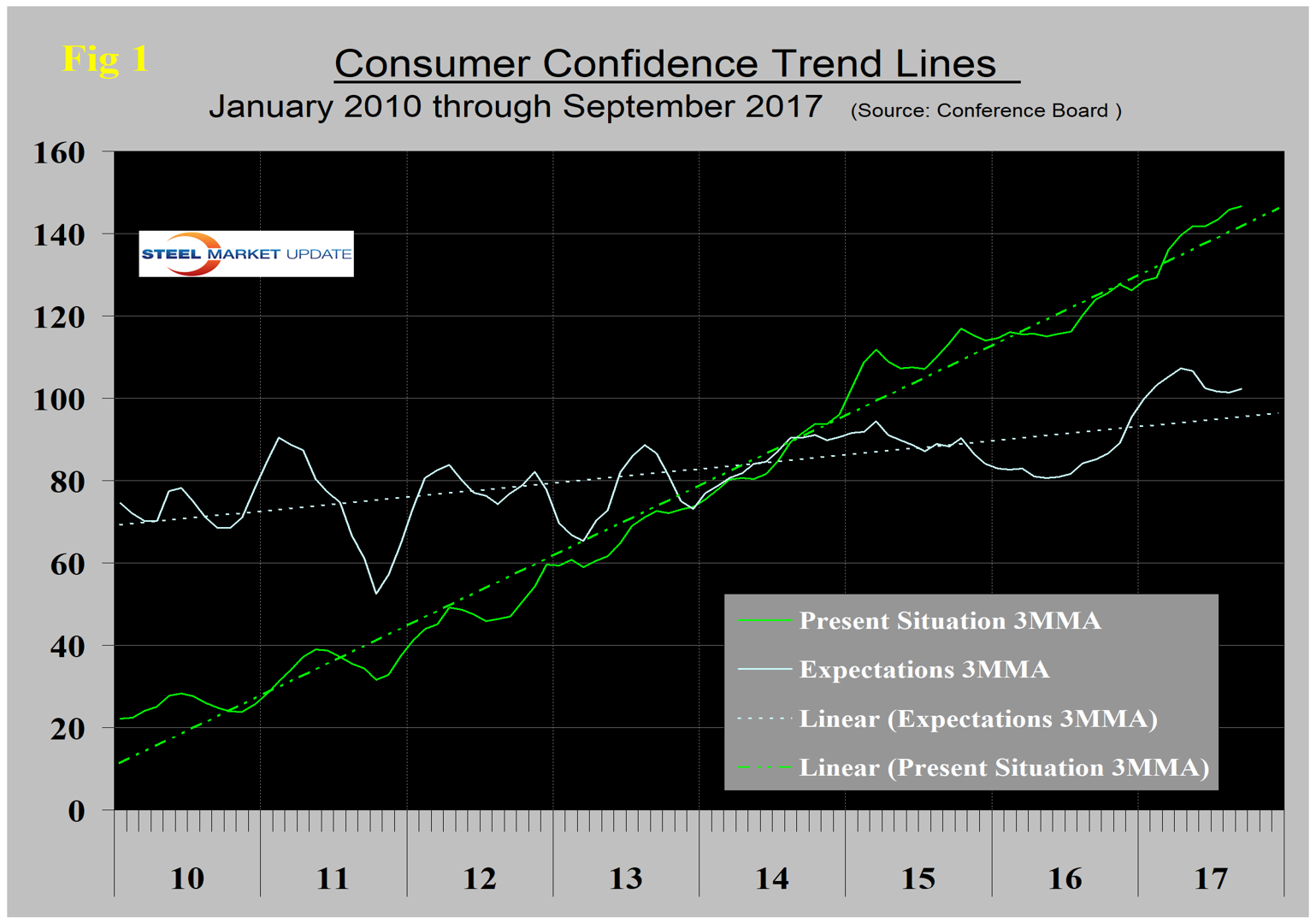

In September, the 3MMA of the composite increased by 0.83 to 120.1 points. We prefer to smooth the data with a moving average because of monthly volatility, which in the case of consumer confidence has been quite extreme since the beginning of last year. The composite index is made up of two sub-indexes. These are the consumer’s view of the present situation and his/her expectations for the future. Both are now above their eight-year trend line (Figure 1).

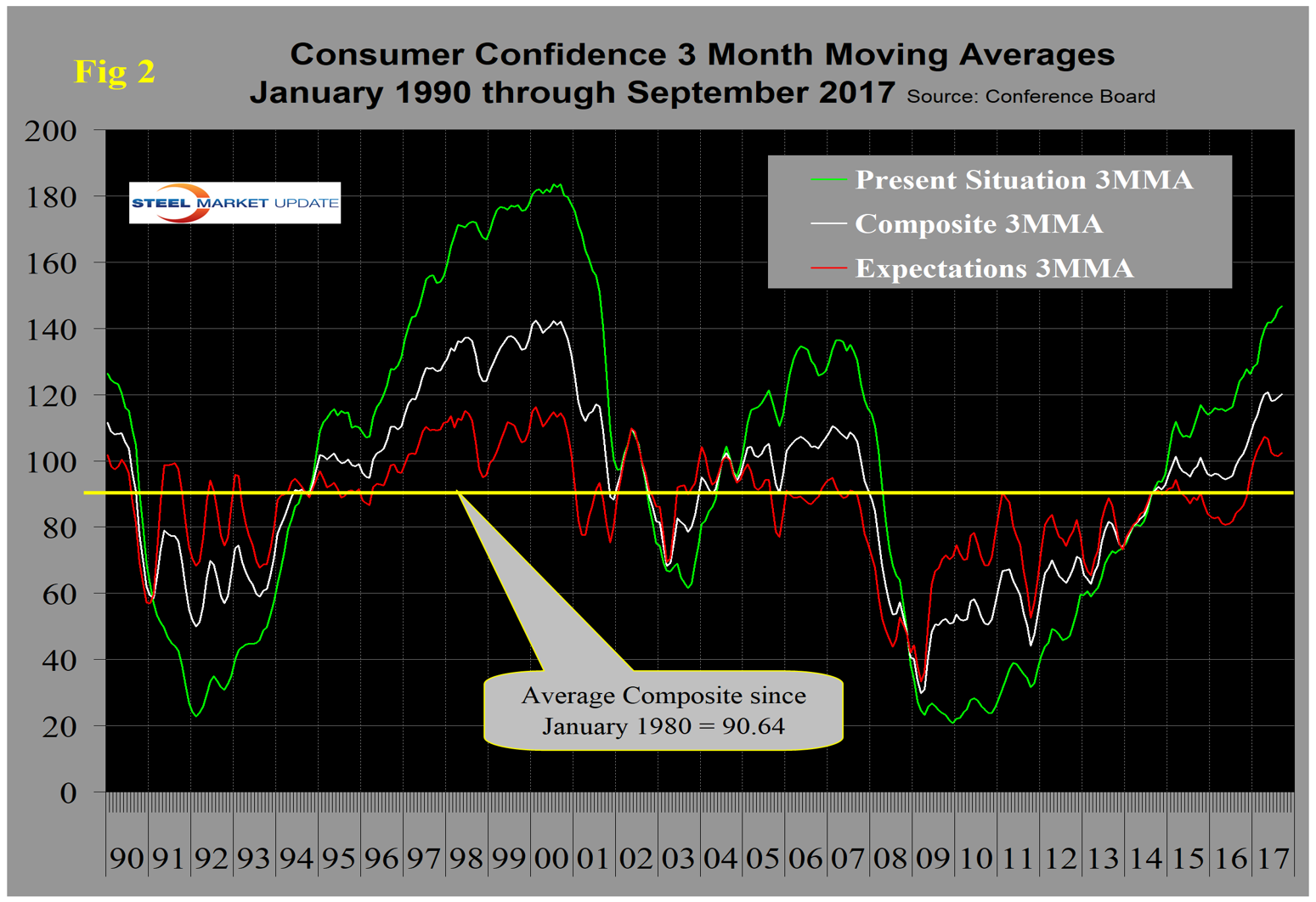

The historical pattern of the 3MMA of the composite, the view of the present situation and expectations are shown in Figure 2. All three measures are now higher than they were at the pre-recession peak of 2007.

The 3MMA of both components of the composite surged from mid-2016 until June this year when expectations declined. Expectations in May were 106.7 and fell to 102.3 through September. Comparing September 2017 with September 2016, the 3MMA of the composite was up by 19.4, the present situation was up by 22.6 and expectations were up by 17.2 (Table 1). Except for July, all sub-indices in Table 1 have been green every month since March. Plans to buy an appliance broke the string and were negative year over year in July. The consumer confidence report includes encouraging data on job availability and wage expectations. It reports on the proportion of people who find that jobs are hard to get and those who believe jobs are plentiful and it measures those who expect a wage increase or a decrease. Since September 2011 both the employment components have steadily improved. The difference between those finding jobs plentiful and hard to get has been in positive double digits every month since February. Expectations for wage increases have not been as consistent but the differential between those expecting an increase and those expecting a decrease has been in positive double digits since January this year. Plans to buy an automobile have been positive year over year for each of the last 14 months. Plans to buy a house have been positive for each of the last six months and plans to buy an appliance have been positive for each of the last 13 months.

Economy.com summarized as follows: “Recent hurricanes create some uncertainty to our near-term forecast, though we are not making any changes, yet. The incoming data will help us assess the hurricane’s impact on both the regional and U.S. economy. Turning to the data, job growth in August came in slightly below our expectation and wage growth was weak. However, technical issues caused a host of problems in August, therefore we are not reading too much into it. Retail sales fell in August, but there wasn’t any clear evidence of an impact from the storms, which is somewhat concerning. There was concern that higher gasoline prices following Hurricane Harvey would affect spending. The storm and floods have interrupted 20 to 40 percent of U.S. refining capacity. Damage to refineries is a serious risk and could cause gasoline inventories to fall more quickly. The one advantage now is that there is more of a cushion in inventories than when Katrina hit. Still, wholesale gasoline prices have risen, foreshadowing further increases in prices at the pump.”

SMU Comment: Based on three-month moving averages, this was another good report. The employment sub-indexes are good, which will drive personal consumption, the largest component of GDP. This in turn will have a positive effect on steel consumption. Our analysis is more upbeat than either Economy.com or the official release below because they both consider month-on-month variations.

Conference Board’s Consumer Confidence Index Declines Slightly in September

The Conference Board Consumer Confidence Index, which had improved marginally in August, declined slightly in September, the group reported in its September press release. The Index now stands at 119.8 (1985=100), down from 120.4 in August. The Present Situation Index decreased from 148.4 to 146.1, while the Expectations Index rose marginally from 101.7 last month to 102.2. The cutoff date for the preliminary results was Sept. 18.

“Consumer confidence decreased slightly in September after a marginal improvement in August,” said Lynn Franco, Director of Economic Indicators at The Conference Board. “Confidence in Texas and Florida, however, decreased considerably, as these two states were the most severely impacted by Hurricanes Harvey and Irma. Despite the slight downtick in confidence, consumers’ assessment of current conditions remains quite favorable and their expectations for the short-term suggest the economy will continue expanding at its current pace.”

Consumers’ assessment of current conditions moderated in September. Those saying business conditions are “good” decreased slightly from 34.5 percent to 33.9 percent, while those saying business conditions are “bad” increased from 13.2 percent to 13.8 percent. Consumers’ appraisal of the labor market was also somewhat less upbeat. Those stating jobs are “plentiful” declined from 34.4 percent to 32.6 percent. However, those claiming jobs are “hard to get” decreased marginally from 18.4 percent to 18.1 percent.

Consumers’ optimism about the short-term outlook was somewhat better in September. The percentage of consumers expecting business conditions to improve over the next six months rose slightly from 19.8 percent to 20.2 percent, but those expecting business conditions to worsen increased from 8.0 percent to 9.9 percent.

Consumers’ outlook for the labor market was more favorable than in August. The proportion expecting more jobs in the months ahead increased from 16.8 percent to 19.5 percent, while those anticipating fewer jobs rose marginally from 13.2 percent to 13.5 percent. Regarding their short-term income prospects, the percentage of consumers expecting an improvement increased moderately from 19.9 percent to 20.5 percent, while the proportion expecting a decline was virtually unchanged at 8.3 percent, The Conference Board reported.