Market Data

March 21, 2018

ABI Growth a Positive Sign for Construction

Written by Sandy Williams

Billings slowed slightly at architecture firms in February, reported the American Institute of Architects. AIA’s Architecture Billings Index (ABI) registered 52.0, down from 54.7 in January. February’s reading above 50 marked the fifth consecutive month of growth for billings. Inquiries into new projects and the value of new signed design contracts both increased in February, said AIA.

Business conditions were strong across the U.S. except in the Northeast where billings fell for the third consecutive month. Firms in the West reported the strongest conditions for that region in a decade. Strongest activity was reported at firms that specialize in residential construction.

AIA noted that some Federal Reserve districts are reporting an increase in steel prices and others districts reported higher lumber prices due to increased construction demand.

- Regional averages: West (57.6), Midwest (54.5), South (54.4), Northeast (47.5)

- Sector index breakdown: multi-family residential (56.6), institutional (53.8), commercial/industrial (51.0), mixed practice (49.7)

Comments:

- “General contractors in the area are beginning to receive notices of price increases in concrete and steel, cost escalation across the board. We are also seeing labor shortages in the construction and architectural industries.” —14-person firm in the South, institutional specialization

- “Big projects are getting all the attention, while smaller, routine projects are struggling for funding and approvals.” —14-person firm in the Northeast, commercial/industrial specialization

- “Project prices are going up, since all subcontractors are busy. Trades can choose projects to work on in our market.” —eight-person firm in the Midwest, mixed specialization

- “Business conditions remain strong; new design work is consistently coming out of our public agencies, and private development does not seem to have slowed at all. The availability of skilled craftsmen is beginning to impact the construction phase of our projects negatively through delays to the overall schedule and a dip in the quality of the work.” —six-person firm in the West, institutional specialization

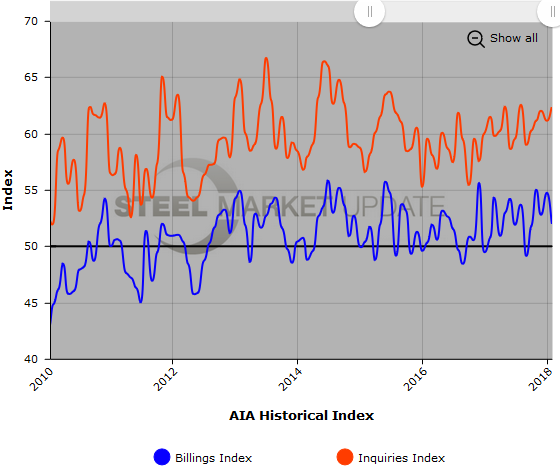

The ABI is considered a leading economic indicator of construction activity and reflects the approximate 9-12 month lead time between architecture billings and construction spending. The survey panel asks participants whether their billings increased, decreased, or stayed the same in the month that just ended. The regional and sector categories are calculated as a three-month moving average, whereas the national index, design contracts and inquiries are monthly numbers. The monthly ABI index scores are centered on the neutral mark of 50, with scores above 50 indicating growth in billings and scores below 50 indicating a decline.

Below is a graph showing the history of the AIA Billings Index and Inquiries Index. You will need to view the graph on our website to use its interactive features; you can do so by clicking here. If you need assistance logging in to or navigating the website, please contact Brett at 706-216-2140 or Brett@SteelMarketUpdate.com.