Market Data

December 19, 2019

CRU: EU Green Deal Launch – Early Reaction for Steel

Written by Matthew Watkins

By CRU Principal Analyst Matthew Watkins, from the Steel Sheet Products Market Outlook

The European Green Deal for the EU was launched on Dec. 11 by the new European Commission. This is a strategy that aims both at achieving zero net emissions of greenhouse gases by 2050 and at managing the transition to that state for the EU’s citizens and businesses.

It presents various high-level goals and strategies to achieve them. A number of these will, if enacted, impact the steel industry on both the supply and demand side. Here we present some early reaction to the launch in those areas.

This topic area is an ongoing megatrend for commodities in general and one on which CRU continues to carry out extensive research and advisory work. Subscribers can read a range of ad hoc analytical and thought leadership pieces on our client website, and we also encourage you to get in touch to discuss your needs further in this area.

A Green Deal, Not a Done Deal – But its Aims Will Shape the Success or Otherwise of Future Business Models

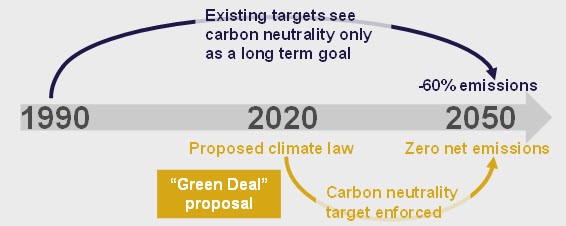

The central goal of achieving EU climate neutrality by 2050 for now remains an ambition. The EC says that by March 2020 it will propose a “climate law” that will make this ambition legally binding and that will also “ensure that all EU policies contribute to the climate neutrality objective and that all sectors play their part.” So, there is a near-term objective to ramp up the enforceability of the elements of the Green Deal, but this is not in place today. Today, not all EU member states are supportive of the 2050 net zero target and will need to be convinced to change their stance.

Other key questions are how much all this will cost, who will pay and how will they pay? There are no firm answers to these questions right now. The Green Deal states that achievement of existing 2030 climate and energy targets will already require €260 billion of additional annual investment (our emphasis) – and the aim now is to go well beyond those. So, the answer to how much this will all cost is clearly “a lot.” There are a multitude of avenues presented in the Green Deal for financing possibilities both public and private, and at EU and member state level. At this point few or none seem to be in place and will require firming up.

The EC further states that current policies will reduce greenhouse gas emissions by 60 percent by 2050 from 1990 levels. Hence in the absence of new legislation and policy there will be a large gap to the goal of the Green Deal, and there is thus considerable risk that some or all of the impacts set out below for the steel sector will be diluted to some degree. As of now they should be interpreted as indications of the direction of travel, or as general goals for the medium to longer term.

Taking Action Now is Important

We do not think this in any way invalidates the need for the steel sector to consider the impacts of the Green Deal. These are things that will shape the success or otherwise of long-term business models to serve European steel demand.

Another key thing to note is that whatever the current status of the legal and financing structures to support it, the Green Deal represents a significant acceleration of the public ambition around response to climate change. The time horizon of industry change has just been brought forward and several public actions impacting steel will now happen soon i.e. in 2020. These include presentation of an EU industrial strategy, a Circular Economy Action Plan and a proposal to support zero carbon steelmaking by 2030.

What Does the Deal Look Like?

In its initial public communication, there is the following visual representation of the Green Deal, which is helpful in identifying and separating out its various focus areas:

Below are a number of proposed action areas contained in the Green Deal that we think have relevance to the European steel sector. There is a mix of threats and opportunities, and here we try to make some early comment at a high level on those:

Steel Supply Side: Prioritizing and Promoting Low Carbon Production

Support for Decarbonization

• The EC intends to “support clean steel breakthrough technologies leading to a zero-carbon steel making process by 2030 and will explore whether part of the funding being liquidated under the European Coal and Steel Community can be used.” A legacy asset of the ECSC is the Research Fund for Coal and Steel. On its website this states that it makes around €40m available each year to fund various research projects that include, but are not exclusive to, CO2 emissions reduction. Given that the UK alone has mobilized a combined GBP350m (€415m) to support decarbonizing UK steel production and deployment of low carbon hydrogen, this funding option does not seem especially large.

• Support for the development of a commercially viable hydrogen economy and carbon capture & storage/usage (CCSU) is implicit in several areas. One is in regard to “smart infrastructure” for energy, where the EC says it will review the existing regulatory framework with the aim to “foster the deployment” of these items. The EC also lists clean hydrogen production and CCSU as priority areas in a desired set of “climate and resource frontrunners” aiming at securing commercial scale breakthrough technologies by 2030.

• Implicitly there is a threat to the business model of carbon-intensive steel making. This threat includes higher emissions costs, possible loss of market access, possible loss of social license to operate, and possible loss of financing options. There is a risk to member state governments here if barriers to exit for private companies are not managed correctly. Bankrupt assets could end up in public hands, with associated large liabilities for industrial site clean-ups. This risk has an interesting current manifestation at Ilva (see a recent Insight for some of the detail on that fluid situation).

Carbon Border Adjustment

• This measure is confirmed as a real possibility but is set to be proposed in 2021, for “selected sectors” – we think likely to include iron and steel. The timescale is perhaps delayed from where domestic producer lobbying might have put it but will mean that the work to inform and shape such a measure will be a live issue throughout 2020.

Security of Supply

• There is a desire to ensure security of supply of raw materials necessary to support implementation of the Green Deal. That could be interpreted broadly. Regarding the steel sector it is likely to mean support for achieving commercial-scale domestic production of green hydrogen (as discussed above) and may mean measures to enhance steel scrap supply. In turn those could include some form of measures that encourage scrap to be consumed domestically rather than exported.

Product Standards, Passports and Public Procurement

• It seems possible that some non-tariff items may be considered in terms of products that would in the future meet EU market demands. Implicitly this presents a question of market access: either your product conforms to requirements and can access the market, or it does not and cannot. These items would equally apply to domestic and imported steel.

• The possibility of an electronic product passport is raised, which would comprise “information on a product’s origin, composition, repair and dismantling possibilities, and end of life handling.”

• Public procurement “should” be “green” and legislation to achieve and guide this is targeted for the future. This may mean an uplift in monetary costs of public procurement (if not environmental/social costs) until such time as the cost of the green option comes down.

Steel Demand Side: Steel Can Both Enable and be Threatened by the Coming Transition, Depending on Area

Stimulate Market Development for Zero Carbon Products

• This overlaps with the item above regarding product standards, etc. Regulation is one way in which a market for such products could be stimulated. It is unclear as yet what the consumer pull is for these products today. A supportive consumer mood in principal seems clear but is it backed up by a will to actually pay a premium? Maybe not. In which case, if forced the consumer will have to buy fewer units at a higher unit price. Can zero carbon be affordable for all?

• This area has an implicit flipside, which is that market development for carbon-intensive products will not be supported. Regulation or other measures could force the issue by reducing market access for products that are not zero carbon.

Support Product Re-use and Recycling

• Any increased re-use of steel-containing products would reduce the future demand growth for new such products.

• Product designs might need to be modified in order to maximize the possibility that they can be re-used or recycled. For example, durability might need to be increased. Material selection and product construction could be considered with a focus on the ease of later dismantling and recycling. As a durable, easily separable (because it is magnetic) and recyclable material, steel may incrementally benefit here.

• A target is stated that the EC will propose measures to ensure that all packaging in the EU is reusable or recyclable by 2030. That could have demand upside for packaging steel, which is highly recyclable.

• Increased use of steel scrap in the value chain would also seem to be encouraged in this area.

Renting and Sharing

• Part of the circular economy plan talks about the potential to encourage renting and sharing business models for materials, products and services. This could raise utilization and reduce demand growth for new products – if they are steel-containing products this reduces future steel demand growth.

Move Freight Transport Off the Roads and Onto Rail and Water

• The EC states that “as a matter of priority, a substantial part of the 75 percent of inland freight carried today by road should shift onto rail and inland waterways.” More freight trains, railways, boats and port infrastructure will be required to achieve this goal, all of which consume steel and could provide a one-off boost as additional capacity is built. The new model might also necessitate new warehousing capacity at new logistics hubs; also, steel-intensive. Fewer road trucks will be needed, which consume some steel, so there would be a structural shift lower in demand from that area.

Investment in Renewable Energy Generation

• Increased offshore wind power generation capacity is viewed in the Green Deal as “essential.” This sector is a major consumer of steel plate. See also a previous Insight on the potential for plate in the UK offshore wind power sector.

Investment in Electric Vehicle (EV) Sector

• Proposed support for deployment of EV charging infrastructure could cause a one-off boost to steel demand.

• The EC will examine possible legislative tools to encourage production and uptake of zero and low emission vehicles. That would be positive for EV-related steel demand but negative for internal combustion engine (ICE)-related demand – for example, anything in the mechanical powertrain or the fuel tank.

• Stringent air pollution emissions standards would be proposed for ICE vehicles and the ETS may be expanded to the road transport sector. These would play out as above in terms of EV/ICE-related steel demand.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com