Prices

March 31, 2020

SMU Price Ranges & Indices: Prices Move Lower

Written by Brett Linton

Steel buyers are beginning to sit on their hands as they watch the damage being done to the economy by the efforts to fight the spread of the COVID-19 pandemic. The problem when buyers begin to sit back and wait is there are limited spot buys actually happening in the market, and many times there can be quite a spread from low to high. That is what we picked up today. The low end of our range was lower than we anticipated (and in some cases we actually picked up data points lower than our print below) while the upper end of our range was higher (one mill sent SMU a note to say they did book a $600 per ton hot rolled spot order today, which is higher than the high end of our range). The key for steel buyers is to understand there is a range and that spot pricing actually can vary from mill to mill.

Because of the limitations associated with the number of spot purchases actually happening this week, SMU reached out to a number of domestic steel mills to confirm what we were hearing from steel buyers. This is normal for us, but this week we increased the number of mill check points because we feel the market is at a critical point. In most cases the mills were surprised by some of the low numbers we were collecting and offered guidance as to their order books and what their sales groups were reporting back to management.

An executive with one of the steel mills told SMU today that it made no sense for their mill to lower spot numbers below their current levels. They are limited in the amount of spot business they are able to take. This may be the case with a number of mills as capacity is taken out of the market on a proactive basis. With scrap expected to drop in April, and with demand in question as to where we may be in 30 days, SMU has shifted our Price Momentum Indicators on hot rolled, cold rolled, galvanized and Galvalume to Lower to reflect what we are seeing in the markets. Our plate momentum indicator remains at neutral.

Here is how we are seeing prices this week:

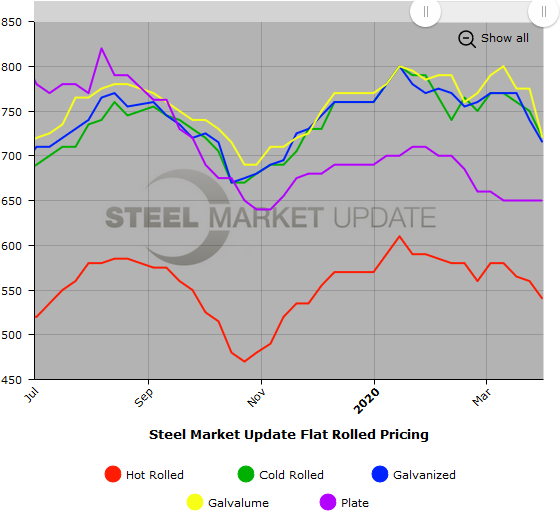

Hot Rolled Coil: SMU price range is $500-$580 per ton ($25.00-$29.00/cwt) with an average of $540 per ton ($27.00/cwt) FOB mill, east of the Rockies. The lower end of our range declined $40 per ton compared to one week ago, while the upper end remained unchanged. Our overall average is down $20 per ton over last week. Our price momentum on hot rolled steel is now Lower, meaning we expect prices to decline over the next 30 days.

Hot Rolled Lead Times: 3-8 weeks

Cold Rolled Coil: SMU price range is $680-$760 per ton ($34.00-$38.00/cwt) with an average of $720 per ton ($36.00/cwt) FOB mill, east of the Rockies. The lower end of our range decreased $60 per ton compared to last week, while the upper end remained unchanged. Our overall average is down $30 per ton over one week ago. Our price momentum on cold rolled steel is now Lower, meaning we expect prices to decline over the next 30 days.

Cold Rolled Lead Times: 4-8 weeks

Galvanized Coil: SMU base price range is $34.00-$37.50/cwt ($680-$750 per ton) with an average of $35.75/cwt ($715 per ton) FOB mill, east of the Rockies. The lower end of our range declined $20 per ton to one week ago, while the upper end declined $30. Our overall average is down $25 per ton over last week. Our price momentum on galvanized steel is now Lower, meaning we expect prices to decline over the next 30 days.

Galvanized .060” G90 Benchmark: SMU price range is $749-$819 per net ton with an average of $784 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 6-8 weeks

Galvalume Coil: SMU base price range is $34.00-$38.00/cwt ($680-$760 per ton) with an average of $36.00/cwt ($720 per ton) FOB mill, east of the Rockies. The lower end of our range decreased $80 per ton compared to last week, while the upper end declined $30. Our overall average is down $55 per ton over one week ago. Our price momentum on Galvalume steel is now Lower, meaning we expect prices to decline over the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $971-$1,051 per net ton with an average of $1,011 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 6-8 weeks

Plate: SMU price range is $620-$680 per ton ($31.00-$34.00/cwt) with an average of $650 per ton ($32.50/cwt) FOB delivered to the customer’s facility. The lower end of our range declined $20 per ton compared to one week ago, while the upper end increased $20. Our overall average is unchanged over last week. Our price momentum on plate steel is Neutral, meaning we are waiting for the market to establish a clear direction.

Plate Lead Times: 4-5 weeks

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume and plate price history. This data is available here on our website with our interactive pricing tool. Note that plate prices are not yet available on our website, but we are in the process of adding that dataset. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or 800-432-3475.