Prices

June 25, 2020

Ferrous Scrap Prices Likely Lower in July

Written by Tim Triplett

Ferrous scrap prices most likely will move lower in July as scrap supplies are increasing at a greater pace than steel demand. Finished steel prices have shown some weakness lately as the market struggles to get back on track and are unlikely to get any help from scrap next month.

Ferrous scrap prices rose $30-40 in May as coronavirus shutdowns disrupted scrap generation and collection and supplies tightened considerably. Scrap prices traded mostly sideways in June, as prime scrap rose by $10 and shredded scrap declined by $10 per ton. Supplies will loosen further next month as more obsolete and prime scrap enters the market, say the experts.

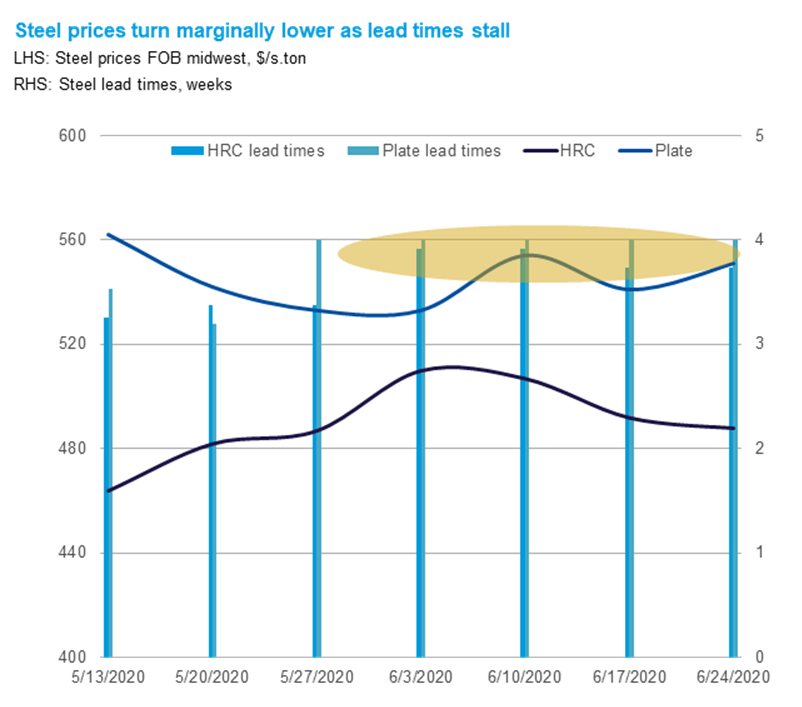

CRU Senior Analyst Ryan McKinley noted that capacity utilization rates at the mills are still quite low and lead times have stalled at around four weeks. “There hasn’t been much upward pressure for finished steel prices, which means there isn’t a lot of incentive to increase scrap prices from mills,” he said. As CRU’s chart below shows, lead times are stalling and prices are lower for hot rolled coil.

“Scrap demand is sputtering as mill capacity still sits at just over 50 percent. Combined with strong scrap collection rates in May/June, scrap prices face downward pressure moving into July,” said a dealer in the Northeast. “As finished steel prices teeter, mills have the added pressure to drop scrap prices to maintain margins. These pressures will be offset somewhat by a stable export market and better demand in some regions of the country such as the Ohio Valley. I see scrap prices range bound through the summer with the delta between prime grades and shred diminishing.”

Another Steel Market Update source points to four factors currently at play: First, mill demand for scrap is better than it was in May, but not as good as expected approaching July. Supply of obsolete grades into scrap yards, while still 30-40 percent below 2019 levels, is nonetheless outpacing mill demand.

Second, there may be additional mills buying scrap in July than there were in June, a mix of integrated and EAFs. Buying by more mills will help buttress the July market.

Third, the prime-shredded spread widened in May and June due to significant supply constraints from manufacturing shutdowns. That spread will likely contract in July as prime scrap prices decline more than those for obsolete grades.

Fourth, export dock inventories are not very deep, but demand from overseas has peaked for the time being after a lot of scrap was sold into Turkey from the U.S. and other regions for June and July deliveries (more than 1 million tons per month to Turkey from all regions).

“Scrap is not moving higher in July, but the degree of the downside, especially for obsolete grades, remains uncertain,” said the scrap executive.