Prices

August 11, 2020

SMU Price Ranges & Indices: Market’s Mixed

Written by Brett Linton

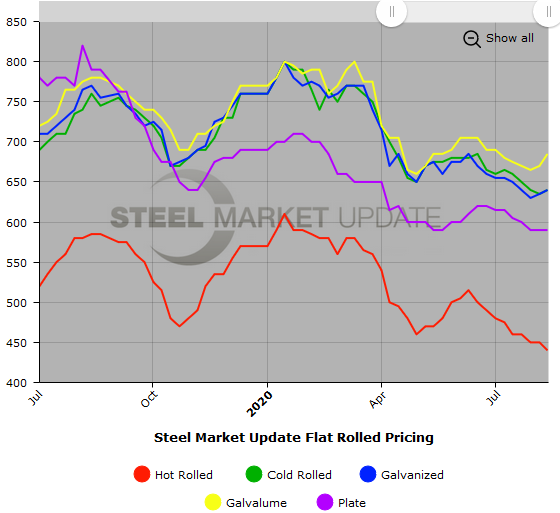

Steel Market Update’s check of the market this week shows hot rolled offers typically in the $460-$480 range. But sources tell us actual transactions are occurring anywhere from $480 down to $400, depending on volumes and other considerations. Thus, SMU puts the current benchmark price for hot rolled at $440 per ton, down $10 from last week. Other products saw prices firm a bit. The market is mixed on whether a price increase is in the wind. SMU’s Price Momentum Indicators remain at Neutral.

Here is how we see prices this week:

Hot Rolled Coil: SMU price range is $400-$480 per net ton ($20.00-$24.00/cwt) with an average of $440 per ton ($22.00/cwt) FOB mill, east of the Rockies. The lower end of our range decreased $30 per ton compared to one week ago, while the upper end increased $10 per ton. Our overall average is down $10 per ton over last week. Our price momentum on hot rolled steel is at Neutral until the market establishes a clear direction.

Hot Rolled Lead Times: 3-6 weeks

Cold Rolled Coil: SMU price range is $630-$650 per net ton ($31.50-$32.50/cwt) with an average of $640 per ton ($32.00/cwt) FOB mill, east of the Rockies. The lower end of our range increased $30 per ton compared to last week, while the upper end decreased $20 per ton. Our overall average is up $5 per ton from one week ago. Our price momentum on cold rolled steel is at Neutral until the market establishes a clear direction.

Cold Rolled Lead Times: 4-6 weeks

Galvanized Coil: SMU price range is $630-$650 per net ton ($31.50-$32.50/cwt) with an average of $640 per ton ($32.00/cwt) FOB mill, east of the Rockies. The lower end of our range increased $20 per ton compared to one week ago, while the upper end decreased $10 per ton. Our overall average is up $5 per ton over last week. Our price momentum on galvanized steel is at Neutral until the market establishes a clear direction.

Galvanized .060” G90 Benchmark: SMU price range is $699-$719 per ton with an average of $709 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 4-8 weeks

Galvalume Coil: SMU price range is $670-$700 per net ton ($33.50-$35.00/cwt) with an average of $685 per ton ($34.25/cwt) FOB mill, east of the Rockies. The lower end of our range increased $20 per ton compared to last week, and the upper end increased $10 per ton. Our overall average is up $15 per ton over one week ago. Our price momentum on Galvalume steel is at Neutral until the market establishes a clear direction.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $961-$991 per ton with an average of $976 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 6-8 weeks

Plate: SMU price range is $580-$600 per net ton ($29.00-$30.00/cwt) with an average of $590 per ton ($29.50/cwt) FOB delivered to the customer’s facility. The lower end of our range increased $10 per ton compared to one week ago, while the upper end decreased $10 per ton. Our overall average is unchanged over last week. Our price momentum on plate steel is at Neutral until the market establishes a clear direction.

Plate Lead Times: 3-5 weeks

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume and plate price history. This data is available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com.