Prices

April 6, 2021

SMU Price Ranges & Indices: Still Some Headroom

Written by Brett Linton

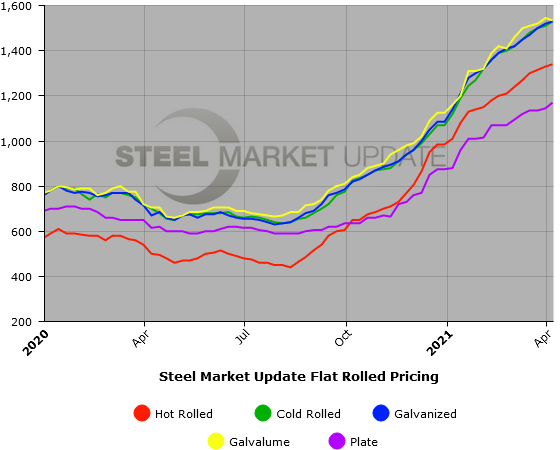

Steel prices cannot rise indefinitely without hitting a ceiling at which they begin to erode demand. But respondents to Steel Market Update’s questionnaire this week report no signs of weakening demand so far. It appears there’s still some headroom for price increases, as most flat rolled and plate tags moved up another $10-25 per ton. SMU’s benchmark price for hot rolled coil, which has been setting new records week after week since mid-January, is now at $1,340 per ton ($67/cwt), surpassing the prior high seen in 2008 by 25%. Sources tell SMU that at least one mill has offered hot rolled at $1,400 per ton ($70/cwt) this week, though we have not yet heard of any takers. With supplies critically tight and few spot tons available, buyers desperate for material may have to pay up. SMU’s Price Momentum Indicators continue to point toward higher steel prices over the next 30 days.

Here is how we see prices this week:

Hot Rolled Coil: SMU price range is $1,320-$1,360 per net ton ($66.00-$68.00/cwt) with an average of $1,340 per ton ($67.00/cwt) FOB mill, east of the Rockies. The lower end of our range increased $20 per ton compared to one week ago, while the upper end remained unchanged. Our overall average is up $10 from last week. Our price momentum on hot rolled steel is Higher, meaning prices are expected to rise in the next 30 days.

Hot Rolled Lead Times: 6-12 weeks

Cold Rolled Coil: SMU price range is $1,500-$1,560 per net ton ($75.00-$78.00/cwt) with an average of $1,530 per ton ($76.50/cwt) FOB mill, east of the Rockies. The lower end of our range increased $40 per ton compared to last week, while the upper end remained unchanged. Our overall average is up $20 per ton from one week ago. Our price momentum on cold rolled steel is Higher, meaning prices are expected to rise in the next 30 days.

Cold Rolled Lead Times: 8-12 weeks

Galvanized Coil: SMU price range is $1,500-$1,560 per net ton ($75.00-$78.00/cwt) with an average of $1,530 per ton ($76.50/cwt) FOB mill, east of the Rockies. The lower end of our range increased $20 per ton compared to one week ago, while the upper end remained unchanged. Our overall average is up $10 from last week. Our price momentum on galvanized steel is Higher, meaning prices are expected to rise in the next 30 days.

Galvanized .060” G90 Benchmark: SMU price range is $1,569-$1,629 per ton with an average of $1,599 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 9-12 weeks

Galvalume Coil: SMU price range is $1,510-$1,560 per net ton ($75.50-$78.00/cwt) with an average of $1,535 per ton ($76.75/cwt) FOB mill, east of the Rockies. The lower end of our range decreased $20 per ton compared to last week, while the upper end remained unchanged. Our overall average is down $10 per ton from one week ago. Our price momentum on Galvalume steel is Higher, meaning prices are expected to rise in the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1,801-$1,851 per ton with an average of $1,826 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 8-13 weeks

Plate: SMU price range is $1,140-$1,200 per net ton ($57.00-$60.00/cwt) with an average of $1,170 per ton ($58.50/cwt) FOB mill. The lower end of our range increased $45 compared to one week ago, while the upper end increased $5. Our overall average is up $25 per ton from one week ago. Our price momentum on plate steel is Higher, meaning prices are expected to rise in the next 30 days.

Plate Lead Times: 6-8 weeks

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume and plate price history. This data is available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com.