Market Data

July 7, 2021

Manufacturing Indicators Show Continued Improvement through May

Written by Brett Linton

U.S. industrial production, manufacturing and durable goods orders continue to show improvement from the coronavirus pandemic downturn, indicating a strengthening manufacturing sector. The health of the manufacturing economy has a direct bearing on the health of the steel industry. Note that some of the historical data below has been adjusted by the U.S. Census Bureau and Federal Reserve, with some revisions going back as far as the mid-2000s.

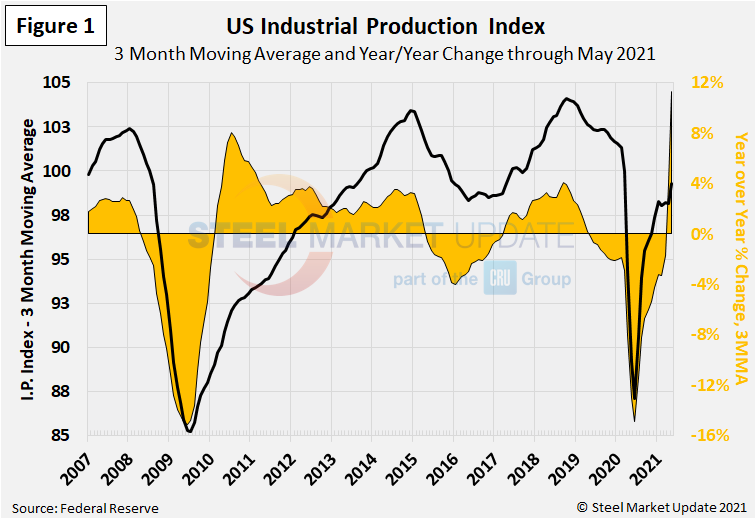

![]() The Industrial Production Index

The Industrial Production Index

The IP index is a gauge of output from factories, mines and utilities. Industrial production took a serious hit from the shutdowns of nonessential businesses and other measures mandated by the government in mid-2020 to stem the spread of the coronavirus. Figure 1 shows the three-month moving average (3MMA) of the IP index since February 2007 as the black line and the year-over-year change in orange. We use the 3MMA calculations here to smooth out some of the monthly variability. From March through June 2020, the 3MMA of the IP index dropped by 14%, from 107.7 down to 93.7. The 3MMA recovered each month through February, and has remained between 98-99 since December 2020. The May 3MMA rose to 99.3, up 11.3% over the same period last year and the highest measure since March 2020.

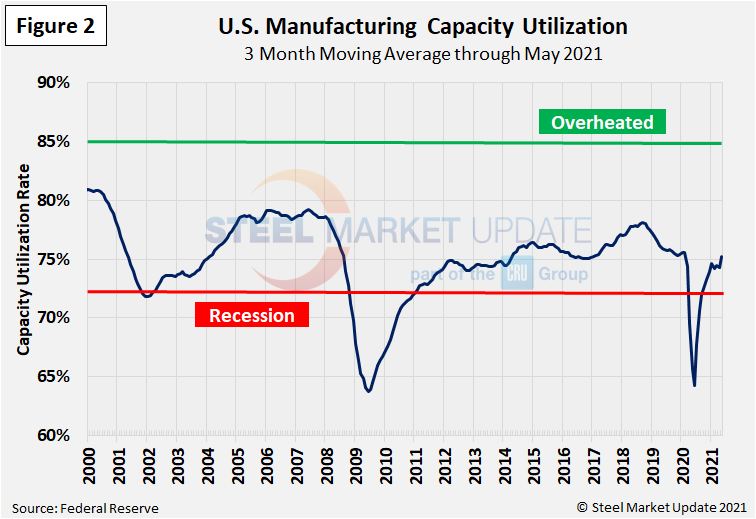

Manufacturing Capacity Utilization

Manufacturing capacity utilization through May was measured at 75.2% as a 3MMA, the seventh month in a row outside of recessionary territory and the highest 3MMA rate recorded since February 2020. The rate had hovered around 75% for most of the 2010’s, but began to decline in March 2020 and reached a low of 63% in June 2020 (Figure 2).

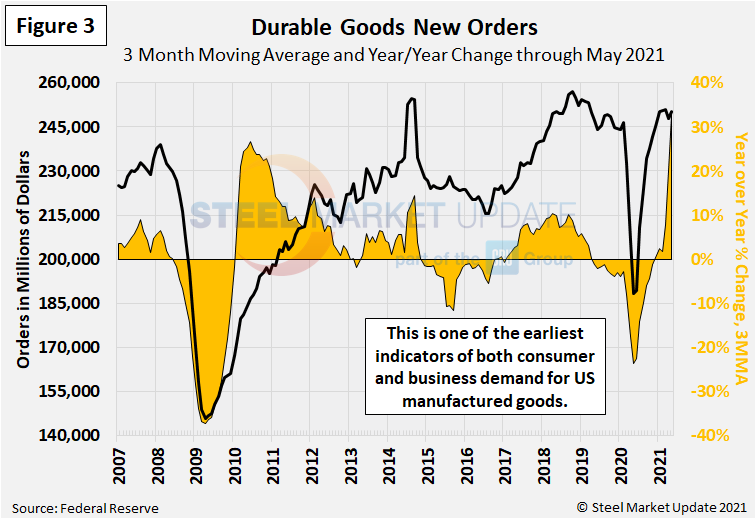

New Orders for Durable Goods

New orders for durable goods, an early indicator of consumer and business demand for U.S. manufactured goods, continues to recover from the virus shock last year and is approaching record levels (Figure 3). New orders increased to $250.1 billion as a 3MMA through May 2021 and has remained around $250 billion for most of 2021. The May figure is the fourth highest reading seen in the last two years. The 3MMA had dropped by 24% from February through May 2020, from a peak of $246.4 billion to a low of $188.4 billion.

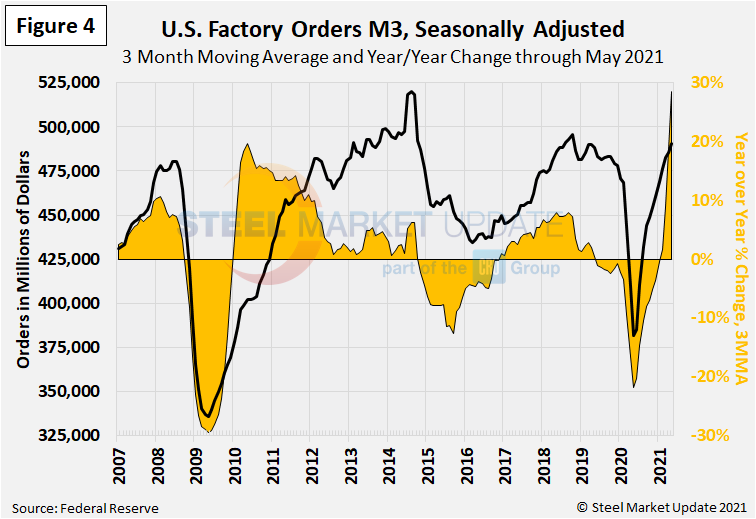

New Orders for Manufactured Products

The growth rate of new orders for manufactured products as reported by the Census Bureau was slightly negative for most of 2019, then declined sharply in March through June 2020 (Figure 4). On a 3MMA basis, factory orders have increased each month over the past year, reaching $490 billion in May 2021. This is up 28.5% compared to one year prior, the highest annual rate of change seen in nearly three decades, surpassing the previous high of 19.7% in May 2010.

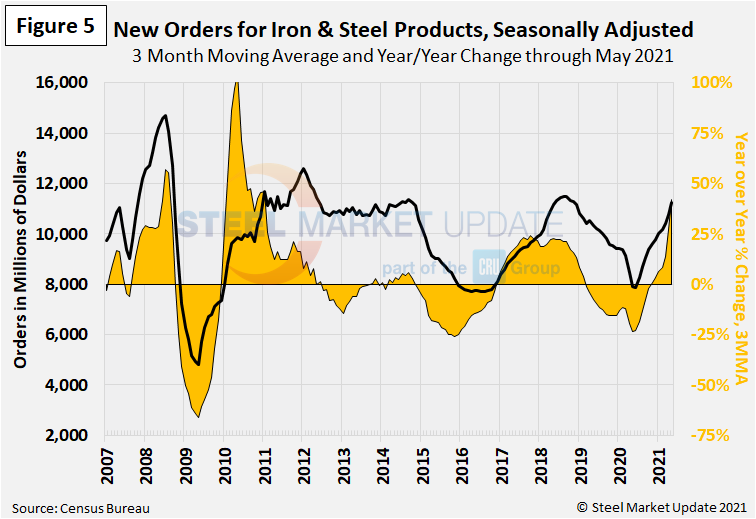

New Orders for Products Manufactured from Iron and Steel

Within the Census Bureau M3 manufacturing survey is a subsection for iron and steel products. Figure 5 shows the history of new orders for iron and steel products since 2007 as a 3MMA. The 3MMA year-over-year growth rate, which reached negative 20.0% last May, rebounded to positive 42.3% this May at $11.3 billion. This is the highest annual rate of change seen since February 2011.

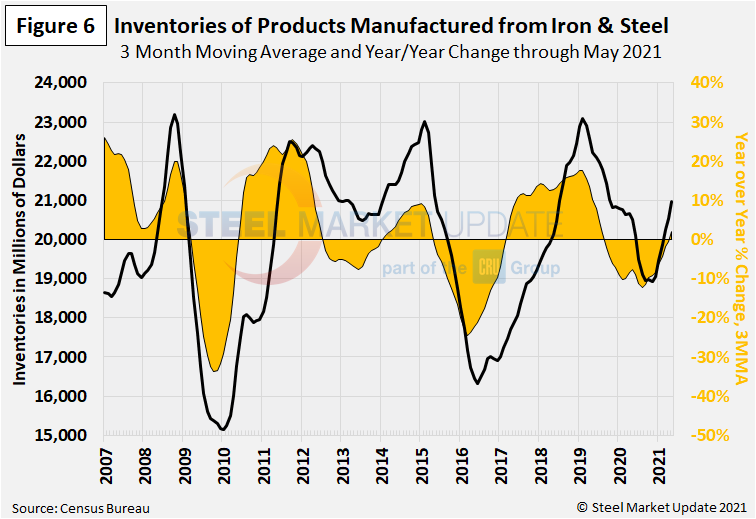

Inventories of Products Manufactured from Iron and Steel

Inventories of iron and steel products broke their multi-month decline streak in December 2020, and have risen each month since. The latest iron and steel inventory levels totaled $21.0 billion on a 3MMA basis in May, up 2.2% compared to the same period the year prior (Figure 6).

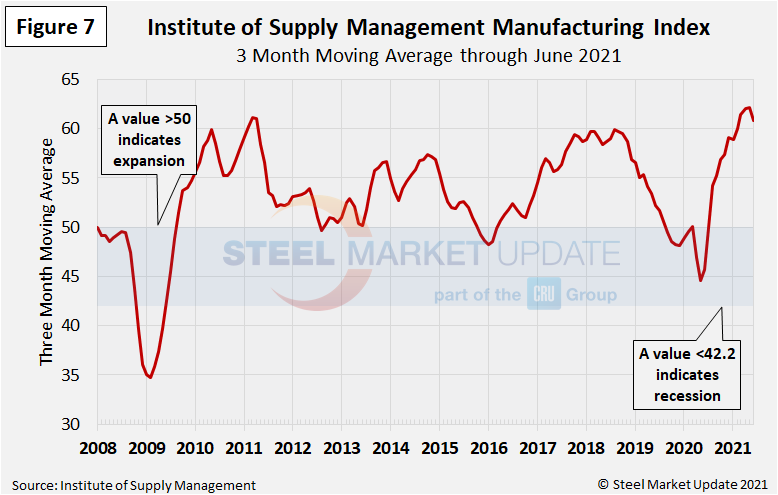

The ISM Manufacturing Index

The Institute for Supply Management’s Manufacturing Index is a diffusion index. An index value above 50 indicates that the manufacturing economy is expanding. As Figure 7 shows, the index on a 3MMA basis was in contraction territory from September 2019 through June 2020, but has recovered each month since then. The ISM index as a 3MMA now stands at 60.8 through June, down from levels three months prior but still strong.

“Manufacturing performed well for the 13th straight month, with demand, consumption and inputs registering growth compared to May. Panelists’ companies and their supply chains continue to struggle to respond to strong demand due to the difficulty in hiring and retaining direct labor. Continued high backlog levels, too low customers’ inventories and record raw-materials lead times are being reported. Labor challenges across the entire value chain continue to be the major obstacles to increasing growth,” said ISM Business Survey Committee Chairman Timothy Fiore.

By Brett Linton, Brett@SteelMarketUpdate.com