CRU

August 13, 2021

CRU: Falling Demand Weighs on Global Metallics Prices

Written by Ryan McKinley

By CRU Senior Editor Ryan McKinley, from CRU’s Steelmaking Raw Materials Monitor

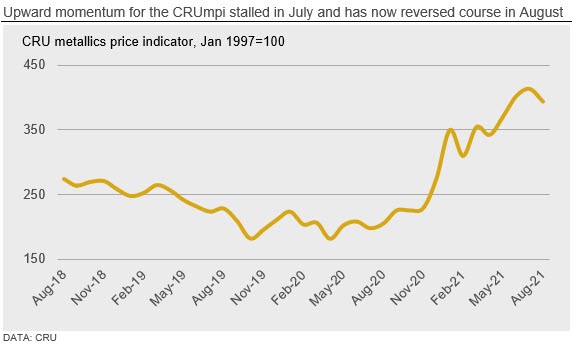

The CRU metallics price indicator (CRUmpi) fell by 4.8% in August to 393.8, making it the first reading below the 400 level since May. Price falls for scrap and HBI were similar in scale, but pig iron prices have moved notably lower. Demand was weaker than expected in nearly all regions, and steady supply inflows tipped global markets into a surplus, resulting in price declines.

Metallics prices across the globe came under pressure in August amid weakening demand and seasonally strong supply availability. Obsolete scrap pricing in the USA fell for the first time since April 2021, while prime grade prices fell in some regions for the first time since August 2020. Meanwhile, prices in Europe and Russia fell on seasonally slower demand and falling Turkish import scrap prices. Policy-led steel output cuts caused Chinese scrap demand, and consequently prices, to also decline, while fresh Covid-19 outbreaks in other areas of Asia limited scrap buys as well. Ore-based metallics pricing faced the most intense downward pressure with European and Chinese buyers out of the market after Russian exporters liquidated stocks ahead of a new export tariff.

U.S. scrap demand was weak compared to supply availability during August trade, resulting in the first drop in obsolete prices in multiple months. While stable in some markets, prime grade prices fell in some regions, and dealers reported having some trouble placing all of their material. This supply/demand imbalance, and subsequent price drops, occurred even as U.S. finished steel prices continue to break all-time records, and domestic HR coil prices now command a premium of over $1,600 /t to shredded scrap prices.

Scrap prices also fell across the board in Europe amid seasonally weak demand and ample supply. Steel mills there were well stocked heading into August, and weakness in the Turkish scrap import market kept more material on the continent. In Turkey, scrap prices have declined as steel long product exporters struggle to find buyers amid high freight rates and demand weakness in Asia. At the same time, well-supplied Baltic and U.S. suppliers allowed Turkish scrap importers to secure discounts.

A fresh round of Covid-19 outbreaks in Asia sent scrap prices lower m/m. New pandemic control measures hampered steel production and by extension scrap demand, and in markets like Vietnam, this was compounded by high steel inventories at mills. Lower demand from Vietnam, South Korea, and Bangladesh meant that exports prices from Japan were lowered m/m, although domestic price directions were mixed.

Scrap demand in China was hampered by regional power outages, steel production cuts and pandemic control measures. Combined, these factors caused total scrap demand to fall by 20-40% m/m in late July, and mills lowered their bids as a result. However, pandemic control measures also resulted in a sharp decrease in scrap collection, and mills were forced to raise bids again to attract material. These factors mostly offset one another, resulting in a relatively small m/m price decrease.

Ore-based metallics underwent the strongest downward price pressure m/m. Following a flurry of offers from Russian exporters looking to get rid of material ahead of a new export tariff, sellers found that only U.S. buyers were still in the market. Using this leverage and against the background of plummeting iron ore prices, U.S. buyers were able to secure material at substantial discounts. Meanwhile, HBI prices declined on falling obsolete scrap prices in Europe.

Outlook: Downside Risks are Mounting

Market sentiment is bearish in most regions we cover given high levels of scrap supply availability and lower steel output rates. In addition, other steelmaking raw material prices are falling—notably iron ore, which recently fell by 27% from its peak just weeks earlier—and will likely allow pig iron producers to drop their prices further. With ore-based and obsolete prices falling, markets like the USA, where pig iron and prime grade scrap prices have inverted this month, will likely see more pressure on the latter come September.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com