Market Data

August 26, 2021

CRU on the Economy: Delta Phi Capex

Written by Jumana Saleheen

By CRU Principal Economist Alex Tuckett and CRU Chief Economist and Head of Sustainability Jumana Saleheen, from CRU’s Global Economic Outlook

The spread of the Delta variant, plus some disappointing data from the U.S., have led us to slightly revise down our forecast for 2021 GDP growth from 6.1% to 5.9%. Growth in industrial production has been revised from 8.7% to 8.5%. However, this is a case of activity postponed; we have revised up our forecasts for 2022. As well as the Delta variant, this month we also focus on stronger demand from the corporate sector through inventories and fixed investment.

Delta Variant Presents Challenge to “Zero-Covid” Approach

The “Delta” variant of Covid-19 first identified in India has now become the dominant strain in most parts of the world – with the exception of South America where the Gamma variant is most widespread. The Delta variant is thought to be around twice as transmissible as the original variant of Covid, and there is some evidence to suggest infection may carry a higher risk of hospitalization and death. The most widely used vaccines – Pfizer, Moderna and Astra-Zeneca – appear to be effective against Delta in preventing serious illness when two doses are given. However, a single dose is significantly less effective against Delta than against the original Covid variant. Furthermore, asymptomatic transmission seems to be widespread even by fully-vaccinated people.

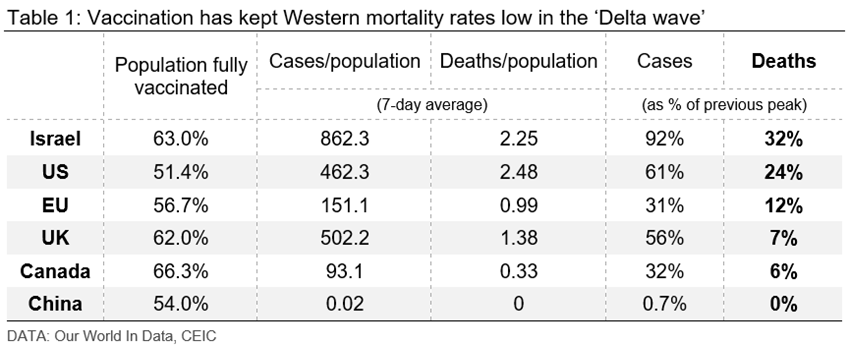

The combination of Delta and the re-opening of economies has led to another wave of cases in Europe and North America (Table 1). However, hospitalization and fatality rates have remained well below the peaks seen in previous waves. Because of this, further material restrictions are unlikely to be imposed, and the economic impact should be modest. Data from the UK and U.S. suggests that the spread of Delta will still lead to some caution amongst consumers, and this has been one of the factors behind our downgrade to U.S. growth in 2021.

However, the Delta variant does present a challenge to the “zero-Covid” approach adopted by many countries in the Asia-Pacific region (APAC), such as Singapore, Australia, New Zealand and (most importantly) China. In contrast to the approach of “living with the virus” pursued in Europe and North America, these countries have sought to suppress any outbreaks completely until widespread vaccination has achieved herd immunity. But this herd immunity may not be a realistic goal; waves of infections in countries such as Israel and the UK suggest that even vaccinating 60-70% of the population is not enough to prevent outbreaks of Delta. Add to this the questions over the efficacy of the two vaccines used in China, and the zero-Covid approach may imply periodic lockdown-style measures for the foreseeable future. This will weigh on consumer confidence and willingness to spend, particularly on contact services. Notably, Singapore has made some tentative moves away from a “Covid-Zero” policy to a “Covid-Resilience” policy that allows travel to some destinations.

The Investment Cycle Gains Momentum…

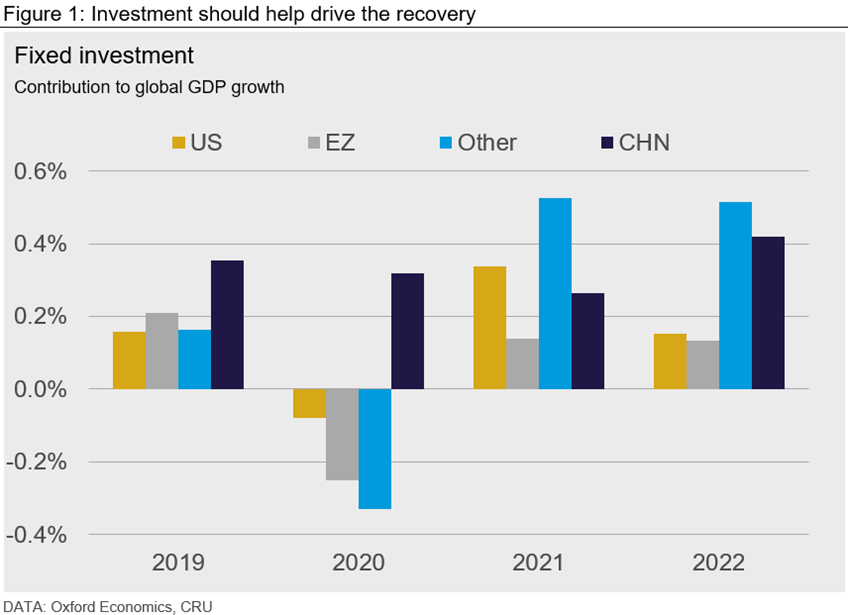

We expect fixed investment to make a strong contribution to global growth both this year and next, after falling in most major economies in 2020 – with the exception of China (Figure 1). Investment spending will be supported by public infrastructure programs in the U.S. and Europe, as well as the policy response to headwinds in China. Strong demand for housing has also supported investment. As investment spending tends to be more commodity-intensive than consumption spending by households or government, this is positive for metals.

Investment spending by the corporate sector should also play its part in the recovery. Conditions are good for business investment; GDP is recovering in most major economies, and funding costs are low. The pandemic has re-shaped the structure of economies – perhaps permanently – requiring many firms to invest in new processes such as digitization. Finally, the green transition will require huge investment by the corporate sector globally.

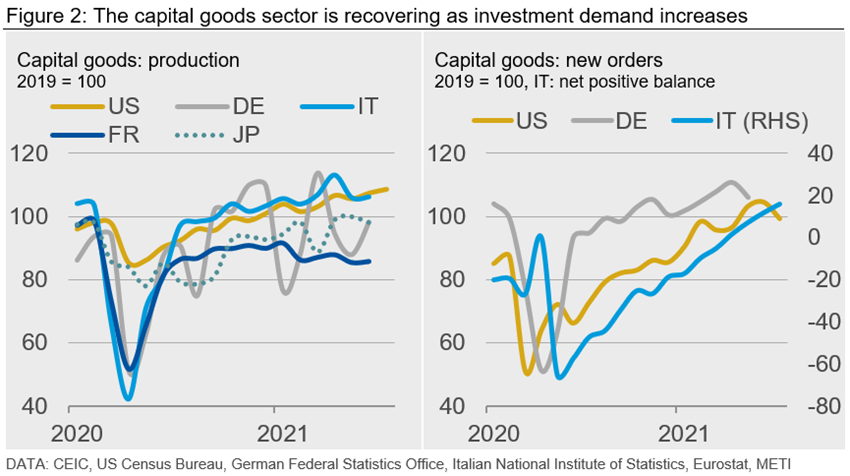

Production of capital goods has increased from the deep trough in early 2020 (Figure 2, left-hand panel). The recovery has been bumpy – particularly in Germany and Japan, and global supply-chain constraints have caused problems. However, the strong increase in new orders for capital goods (Figure 2, right-hand panel) suggests that investment spending should increase further as supply shortages ease. Other indicators also point to strong growth in investment. The balance for capital spending over the next six months from the U.S. Business Roundtable survey is at the highest level since mid-2018, and investment intentions reported to surveys by the New York Fed and National Federation of Independent Business have recovered significantly. Shipments of Japanese industrial robots in 2021 H1 were at their highest ever level, up two-thirds from 2020 Q2. Stronger business investment should complement infrastructure and housing investment in supporting demand for commodities.

…While Supply Chain Problems Hold Back Inventories

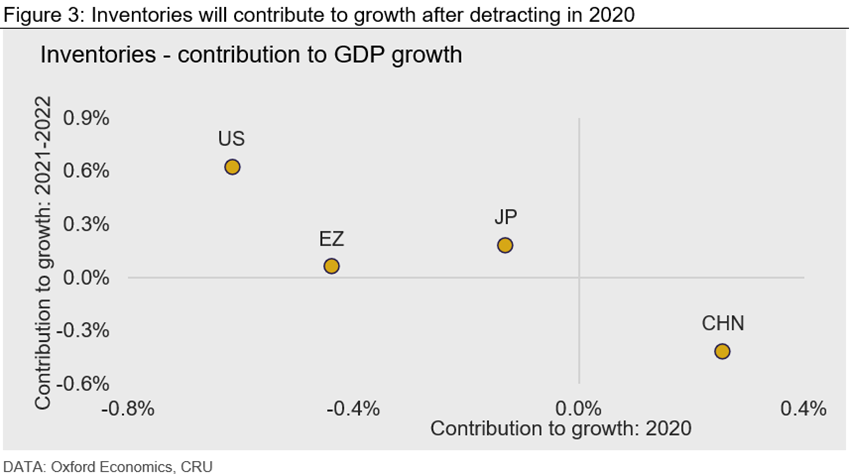

Spending on inventories in advanced economies fell sharply in 2020. Companies reacted to the speed of the downturn by cancelling orders and running down stock levels to preserve cash. Although far less important than the collapse in consumer spending, this deepened the recession in 2020 (Figure 3).

We expect inventories to be rebuilt, contributing to growth in 2021 and 2022 (Figure 3). The boost to growth should be greatest in the U.S., where inventories fell the furthest in 2020, according to national accounts data. The exception to this is China, where spending on inventories continued in 2020, albeit at a level lower than recent years.

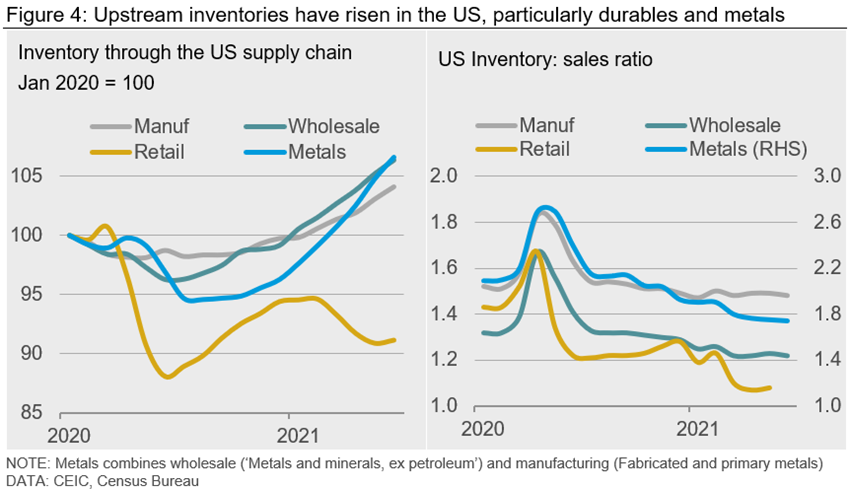

National accounts data on inventories is available only with a lag. Higher frequency data for the U.S. show a mixed picture since the start of 2021. Inventories held at retailers have fallen as consumer demand has surged. But wholesalers and manufacturers – which account for around two-thirds of the total value of stock – have increased their inventories and are now above the level of January 2020 (Figure 4, left-hand side). Stocks of durable goods and metals products in particular have surged. Upstream metals inventories have risen 13% so far this year, and are almost 8% higher than their December 2019 level.

This inventory build is a response to strong demand, as consumers spend heavily on goods – particularly durables. Stock-sales ratios are at pre-pandemic levels for manufacturers and below pre-pandemic levels for wholesalers (Figure 4, right-hand side). However, if demand for durables eases back as the economy re-opens and consumers rotate towards spending on services, those inventory levels could turn out to be too high. In addition, global supply-chain disruptions may be leading firms to over-order as a precaution. Once supply-chain disruptions ease, the industrial sector could be left with a surplus of inventory. If that materializes, new orders could slow sharply.

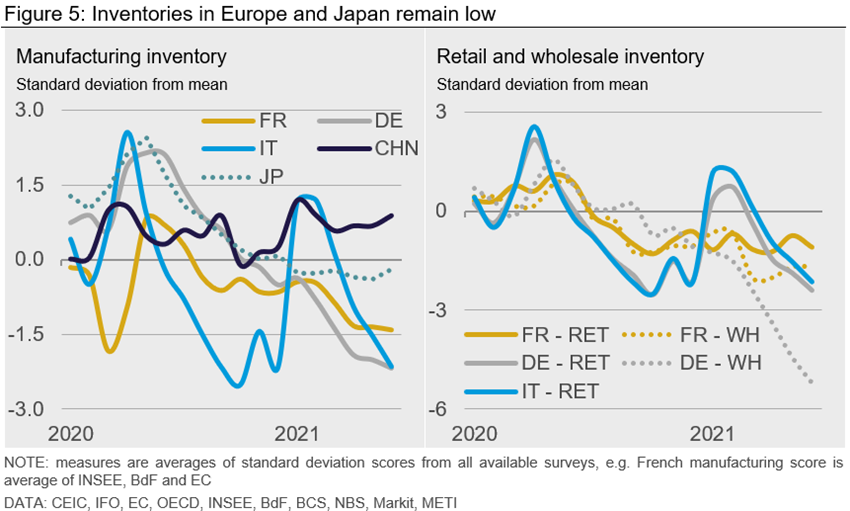

The U.S. is ahead of other regions in the inventory cycle. Total industrial inventories have been increasing in China as well, and are 13.5% above pre-Covid levels. However, inventory indicators in Europe and Japan have yet to recover their pre-Covid levels (Figure 5). Supply constraints are biting hard in Europe, and demand has not recovered as quickly. As the recovery strengthens in Europe, inventory levels are likely to be re-built.

Recovery Remains Healthy Despite Delta Threat

In previous months, we have discussed consumer demand and public investment programs in the U.S. and Europe, and how these could affect metals demand. In this overview we have turned to demand from the corporate sector. Broadly, this is a positive story. The fundamentals for corporate investment spending look good, and this will support demand for commodities.

However, Covid-19 continues to pose a threat to the world economy. The spread of the Delta variant in western advanced economies will probably not result in further lockdowns, but it may act as a limiting factor on the consumer recovery. More seriously, Delta presents a challenge to the “zero-Covid” strategy pursued by China and other APAC economies. The aggressive response by the Chinese authorities has added to supply disruptions in the short-term, and repeated outbreaks could depress consumer demand. Although this will be negative for GDP in China and its trade partners, perversely there could be an upside for commodities if the policy response to slower growth involves re-opening the infrastructure spending taps.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com