CRU

October 1, 2021

CRU: Price Declines Outside of the USA Accelerate

Written by Ryan McKinley

By CRU Senior Editor Ryan McKinley, from CRU’s Steel Sheet Products Monitor

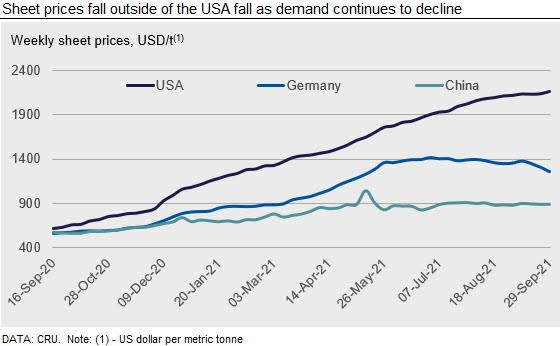

Sheet prices outside of the USA fell markedly this week as demand declines and inventories build. The largest of these declines occurred in Europe, as lower-priced imports forced Italian domestic prices to fall below the €1,000 /t mark for the first time since May. German domestic prices were also down notably w/w. Expectations that prices will fall further in southeast Asia, amid yet more competitive offers from Russian producers, caused domestic prices to fall despite a spike in coking coal prices. U.S. sheet prices rose w/w, although the spread between transactions is widening and buyers are beginning to decline spot offers as their inventories find balance. In China, prices were stable w/w due to low trading activity ahead of national holidays.

USA

In the USA, HR coil prices rose this week, increasing by $24 /s.ton, but CR coil and HDG coil prices fell. While there were enough high-priced transactions to raise HR coil prices this week, we also saw purchases at lower numbers, which may indicate we have reached a peak in pricing. Spot buy volumes continued to decline as buyers were either content with contract tons or had already purchased import material due in Q4 2021 or Q1 2022. Several buyers reported that they had been offered spot tonnage but passed on the opportunity because their inventories are in balance with demand, and they believe that prices will be more attractive soon. Many companies expressed an inability to pass along higher prices to their customers and noted that they are beginning to see more competition for orders from other distributors. New import opportunities were less attractive when compared to contract pricing, futures pricing, and new domestic spot offers.

Steel prices on the U.S. West Coast remained stable this week as buyers wait for December pricing to be announced. Buyers expect new mill prices to be flat or increase a small amount as limited regional mill competition, lack of offers from other domestic mills, and increasing freight costs keep pricing firm. New import offers reportedly have more restrictions on size, grade and minimum order quantity than previous offers.

Europe

European sheet prices have fallen significantly this week, especially in Germany where falls of €30-€40 /t w/w can be seen across all sheet products. European mills are experiencing increased price pressure from less expensive import options from India and Russia. Russia reportedly is offering HR coil into Southern Europe at below €800 /t excluding the antidumping duty imposed on Severstal. Italian HR coil has dropped below the €1,000 /t mark to €996 /t for the first time since the second week of May earlier this year.

The Turkish market seems to be restricting any HDG offers into Europe recently, which is unusual as importers like Spain have concluded many deals with the Turks for this material in prior months. According to some market participants, Turkey is changing their product program to now offer more CR coil at attractive prices, especially as there is an ongoing investigation into the antidumping of Turkish HDG material into Europe.

China

Chinese domestic sheet prices stay stable as business slows down ahead of the national holidays. Transactions were scarce but expectations over tighter production controls remain strong and supported prices despite weakening underlying sheet demand. Supply restrictions have further intensified with power supply becoming problematic in some provinces. A shortage of coal has triggered provinces, including Jiangsu, Jiangxi, Guangdong, and Anhui, to control power consumption. Local producers, especially EAFs, were therefore ordered to cut production. However, we do not believe this will have a significant impact for sheet given that the majority of sheet production is BF/BOF based, and existing supply restriction have already capped sheet production before the power consumption limits were put in place. Going forward, we continue to believe a seasonal demand recovery in October will bring some upside to sheet prices, though potential policy changes may put this view at risk. However, lower production costs in our forecast suggest a price decline for finished steel even as profitability stays the same after October’s seasonal uptrend.

Asia

Prices of imported sheet products decreased this week due to limited buying interest.

Rerolling mills in Vietnam have been relying on exports and, according to market sources, now have orders booked through November. However, sales may slow from December onwards and, as a result, mills are being very cautious with raw material procurement. Meanwhile, Indian mills have been aggressive, and some mills lowered their offers to $870 /t CFR Vietnam after seeing Russian material sold to Vietnam at $850-855 /t CFR Vietnam for December shipment.

There have been plans to ease some Covid-19 restrictions in Southeast Asian countries such as Vietnam and Indonesia and some expect this to result in increased demand. For now, though, things remain uncertain.

CRU assessed HR coil prices at $870 /t CFR Far East Asia, a $25 /t fall w/w. CR coil prices were assessed at $1,120 /t CFR Far East Asia, while HDG prices were assessed at $1,140 /t CFR Far East Asia (both down by $20 /t w/w).

India

Spot sheet prices in India have declined by another INR700-1200 ($9-16) /t w/w because of weak market sentiment due to low offtake from key manufacturing end users. Buyers are holding off their purchases, expecting further price declines in the coming month as availability and mill stocks continue to rise and put downward pressure on prices.

Meanwhile, steelmakers are planning to push through a price increase of INR1000-1500 ($13-20) /t across sheet products for October deliveries, attributing it to a rise in input costs, particularly that of coking coal. Given the prevailing market sentiment, CRU doesn’t believe any price increase will be absorbed by the market. Furthermore, Indian HR coil export prices have fallen by $15-20 /t w/w to $830-840 /t FOB, which is at a discount of $20-30 /t over the latest domestic HR coil price. Therefore, external factors also do not support a price increase. Nevertheless, fresh demand from Europe in early October, as Q4 import quotas open up, may provide some price support.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com